Download

1 / 56

560 likes | 731 Views

British Banking Structure and Stability over the Long Run. John D. Turner Queen’s University Belfast. Introduction. Why look at the long run? Banking crises are low frequency events Therefore to understand crises we need to develop a long-run perspective Dangers Nostalgia Cherry pick.

E N D

British Banking Structure and Stability over the Long Run John D. Turner Queen’s University Belfast

Introduction • Why look at the long run? • Banking crises are low frequency events • Therefore to understand crises we need to develop a long-run perspective • Dangers • Nostalgia • Cherry pick

Introduction • Britain has only had two severe systemic banking crises over the past two centuries (1825/6 and 2007/8), and these two crises are correlated with inadequately capitalised banking institutions.

Introduction • Stability in the interim period • Up until c.1940 – extended or contingent liability • After 1940 – contingent capital disappears and low capital ratios, but there are constraints on bank risk taking • Basic argument: adequate capital prevents residual claimants opportunistically increasing asset risk, a phenomenon known as risk shifting.

Introduction Related literature • Bank capital and risk shifting • Berger et al. (1995) • Contingent capital and risk shifting in U.S. • Macey and Miller (1992); Esty (1998); Grossman (2001). • Contingent capital and early joint-stock banking systems • Hickson and Turner (2004)

Introduction • Proposals for reform which mimic contingent liability • Flannery (2009) – ‘contingent capital certificates’ • Admati and Pfleiderer (2010) – ‘equity liability carriers’ • Conti-Brown (2011) – unlimited liability for systematically important financial institutions

Outline • British banking crises, 1800-2008 • Risk shifting and capital • Banking capital, 1800-2008 • Partnership banks • Extended shareholder liability • Constrained banking in the era of low capital • Liberalisation and capital adequacy regulation • Speculation and discussion

British banking crises, 1800-2008 • Defining banking crises • Narrative vs quantitative approaches • Grossman (2010) and Reinhart and Rogoff (2009) • Crisis = failure (or bailout) of one or more commercial or investment banks • Problems with this definition • Bank failure ≠ banking instability • Bank failure can enhance banking stability (Calomiris and Kahn 1991) • English banks learned to be become more prudent as a result of observing bank failures (Collins, 1990; Baker and Collins, 1999) • Investment banks included – not directly linked to money supply or engaged in credit intermediation

British banking crises, 1800-2008 • Focus on systemic stability of commercial banking system • 10% or more of commercial banking system fails (or is bailed out) in terms of number of institutions or bank assets

British banking crises, 1800-2008 • 1836-37 • Agricultural & Commercial Bank of Ireland; Northern & Central Bank of England • 1857 • Western Bank of Scotland – 4.8% of British banking capital • Depositors lost nothing, but 1,280 shareholders had to pay out £851 on average. • 1866 • Birmingham Banking Company - 0.7% of British banking capital • 1878 • City of Glasgow Bank – 1.9% of British banking capital • Depositors paid in full, but 86% of its 1,819 shareholders bankrupted.

British banking crises, 1800-2008 • 1890 • Privately-organised bailout of Barings • 1914 • 5-day Bank Holiday at start of August due to liquidity pressures faced by BoE. • Special issue of Treasury notes was created rather than suspending gold convertibility. • National Penny Bank failed.

British banking crises, 1800-2008 • 1974 • Secondary banking crisis. • Secondary banks raised money on wholesale money markets and used funds to make property and consumer finance loans. • Lifeboat operation, where £1,300m was advanced by commercial banks. • Only a few secondary banks failed. • 1984, 1991 & 1995 • Johnson Matthey Bankers • BCCI • Barings

British banking crises, 1800-2008 • 2007-8 • Northern Rock nationalised • Alliance and Leicester acquired by Santander • Bradford & Bingley nationalised • Lloyds-TSB took over HBOS • Lloyds-TSB and RBS required substantial capital injections • Six of the nine largest UK commercial banks were effectively insolvent • 46.7% (in terms of assets) of the British banking system required a government bailout • An unprecedented collapse!

Outline • British banking crises, 1800-2008 • Risk shifting and capital • Banking capital, 1800-2008 • Partnership banks • Extended shareholder liability • Constrained banking in the era of low capital • Liberalisation and capital adequacy regulation • Speculation and discussion

Risk shifting and capital • Risk shifting, by its very nature, cannot be observed and is typically exposed whenever the banking system is hit by a shock. • If risk shifting has occurred on a large enough scale and equity capital resources are insufficient, then banks will be unable to withstand the shock, resulting in a banking crisis.

Risk shifting and capital Ameliorating risk shifting • Depositor monitoring • Vigilant financial press (Hayek, 1990) • Sequential service rule (Calomiris and Kahn, 1991) • Brand-name capital (Klein, 1974) • Last period problem or high discount rate • Capital • Need large amounts of idle funds • Severe agency problems • Contingent capital • Regulation

Outline • British banking crises, 1800-2008 • Risk shifting and capital • Banking capital, 1800-2008 • Partnership banks • Extended shareholder liability • Constrained banking in the era of low capital • Liberalisation and capital adequacy regulation • Speculation and discussion

Partnership banks • Prior to 1826 • Banks constrained to partnership form • Six-partner rule in all bar Scotland • Problems with six-partner rule • Inhibits diversification of assets and liabilities • Reduces size of equity cushion and inhibits ownership diversification • English law partnerships • Was six-partner rule binding? • No separate legal personality → hold-up problems → results in small number of homogeneous partners

Partnership banks • Stability of Scottish banking at the time • Absence of six-partner rule (Kerr, 1884; Cameron, 1967; Munn, 1981; White, 1995) • Scottish partnership law (AHT, 2011) • Scottish partnership law • Contracting and governance decisions limited to a managerial hierarchy. • Enabled large partnerships to emerge having heterogeneous members. • Banks had large equity cushions and diversified ownership.

Outline • British banking crises, 1800-2008 • Risk shifting and capital • Banking capital, 1800-2008 • Partnership banks • Extended shareholder liability • Constrained banking in the era of low capital • Liberalisation and capital adequacy regulation • Speculation and discussion

Extended shareholder liability • Banking Copartnership Act (1826) • Banks could incorporate, but shareholders had unlimited liability. • Banks had large equity cushions and diversified ownership. • Unlimited liability underpinned the stability of the banking system. • Objections

Extended shareholder liability • Objection 1 - Banks shares owned by low-wealth individuals (Bagehot) • Directors vetted candidate owners for suitability • Shares couldn’t be transferred without director approbation • Wealthiest shareholders had incentives to be directors as they had most to lose. • Evidence (Hickson and Turner 2003; Turner 2009)

Extended shareholder liability • Objection 2 – Shares could be dumped at onset of financial distress • Agricultural & Commercial shares • Post-sale extended liability clauses • Objection 3 – Share trading is moribund • Woodward (1985); Carr and Mathewson (1988); Winton (1993) • Top 20 largest companies on London market in 1870 contained five banks with unlimited liability • Changes in shareholder liability had no effect - AHT (2010)

Extended shareholder liability • Objection 4 – City of Glasgow Bank crash • the CGB failure highlighted the extent to which shares in the large unlimited liability banks had been diffused to individuals of modest means. • the CGB failure resulted in wealthy shareholders of other banks dumping their stock, with the consequence that bank shares ended up in the hands of low-wealth individuals.

Extended shareholder liabilityA digression on the CGB • By 1878, it had 3rd largest branch network in Britain and was Glasgow’s premier bank. • Bank was closed on 1st October 1878 with a £5,190,983, 11s. 3d. shortfall between assets and liabilities. • 4% of Scotland’s GDP at the time. • £1/2 bn in today’s money! • There wasn’t a widespread run on other banks.

Extended shareholder liabilityA digression on the CGB • Impact on CGB shareholders • 1st call - £613 per share in December 1878 • 2nd call - £2,250 per share in April 1879 • The average shareholder had to pay in excess of £12,000 (approx. £1m in today’s money) • Only 254 shareholders out of 1,819 were still solvent at the end of the process

Extended shareholder liabilityA digression on the CGB “In hundreds and thousands of cases homes have been broken up, health and life destroyed, dismay and ruin spread over towns and parishes, sons and daughters left penniless – by the wickedness and folly which perverted a public trust in so infamous a manner.” The Economist (1879)

Extended shareholder liabilityA digression on the CGB • Acheson and Turner (2008) • CGB shareholders were wealthy • No evidence of shares being dumped at other banks • No evidence of wealthy shareholders at other banks trying to exit

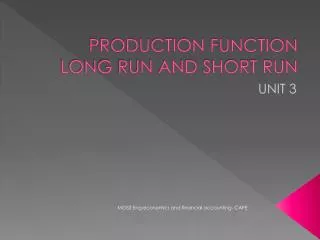

Average returns (%) on bank shares in months after CGB failure Forced sale of shares – e.g. 107 CGB shareholders owned shares in the Clydesdale Bank

Extended shareholder liability • Limited liability introduced – 1857/8 • But established banks did not convert • New limited banks • The median limited bank in 1874 had uncalled capital to cover 50.6% of deposits and paid-up capital to cover 25.2% of deposits • “practically as safe as an unlimited bank” (Dun, 1876)

Extended shareholder liability • 1879 Companies Act – reserve liability • Enabled banks to “set aside and hypothecate a certain portion of its registered capital, as an inalienable fund for the protection of its depositors” (Rae, 1885, p.258). • In 1884 • 83 out of 139 banks had reserve liability • Nine had unlimited liability • The rest had uncalled capital • Average liability carried by bank shareholders - £3.10 for every £1 they had invested in a bank. • Such high levels of shareholder liability would have potentially acted as a substantial check on bank risk shifting.

Extended shareholder liability • Could bank shares could end up in the hands of individuals who have inadequate wealth to cover their extra liability? • Bank directors had the power to exclude those with inadequate wealth to meet calls from acquiring shares (Rae, 1885; Withers and Palgrave, 1910). • Also, under the 1862 Companies Act, ex-shareholders of banks were liable for all unpaid capital for up to one year after they ceased to be a shareholder.

Outline • British banking crises, 1800-2008 • Risk shifting and capital • Banking capital, 1800-2008 • Partnership banks • Extended shareholder liability • Constrained banking in the era of low capital • Liberalisation and capital adequacy regulation • Speculation and discussion

Constrained banking in an era of low capital • How was move to low capital and no extended liability possible? • Why did the banking system remain stable despite such low levels of capital? • During the 1940s and 50s, various discussions were held between the banks and the Bank of England about raising bank capital so that capital / deposit ratios would be strengthened. • But the Bank of England was always reluctant for this to happen • divert capital away from productive industry. • “banks were not suffering in prestige from low capital/deposit ratios”, as bank capital had “long ceased to bear any serious relation either to their liabilities or functions”

Constrained banking in an era of low capital • Bank of England and the commercial banks had a symbiotic relationship whereby • the banks were allowed to operate a cartel • and the Bank issued (on behalf of the government) informal directives • This informal relationship was created during Norman’s governorship. • The directives were, in general, not supervisory in nature and were not usually concerned with the security of the banking system (Fforde, 1992, p.21). • Rather they concerned government attempts to influence the economy via credit and monetary policy.

Constrained banking in an era of low capital • Qualitative directives • Lending to specific sectors • Quantitative directives • Reserve ratio = 8% • Liquidity ratio = c.30% • Large holdings of government debt

Constrained banking in an era of low capital • These constraints would have severely limited bank’s ability to risk shift. • They may explain why the Bank was uninterested in low capital / deposit ratios, and why the banking system was stable despite low capital ratios.

Constrained banking in an era of low capital • Why did this informal system work? • Stick • Bank would not maintain an account for a non-compliant bank and would not allowing such a bank to use its discount window (Wadsworth, 1973; Hirsch, 1977). • Although the Bank was given statutory powers under the 1946 Bank of England Act to enforce compliance with its directives, it did not resort to using that power. • Carrot • Banks were allowed to operate a cartel as a quid pro quo for their compliance with directives and for their willingness to hold government debt (Griffiths, 1973; Cottrell, 2003).

Outline • British banking crises, 1800-2008 • Risk shifting and capital • Banking capital, 1800-2008 • Partnership banks • Extended shareholder liability • Constrained banking in the era of low capital • Liberalisation and capital adequacy regulation • Speculation and discussion

Liberalisation and capital adequacy regulation • Increase in competition • New institutions had no incentive to comply with Bank of England directives or requests and the mushrooming of institutions made informal control more complex (Forde, 1992). • Commercial banks abandoned their interest rate cartel in 1971.

Liberalisation and capital adequacy regulation • Supervisory reform after secondary banking crisis • banks had to make detailed statistical returns (annually for clearing banks and quarterly for other banks) and then be interviewed by the Bank. • Discretion rather than rules • This supervisory approach was codified in the 1979 and 1987 Banking Acts. • As prudential regulation was enacted, Bank directives in terms of lending and liquidity gradually disappeared, potentially giving banks a lot more latitude in terms of risk shifting.