Download

1 / 28

280 likes | 624 Views

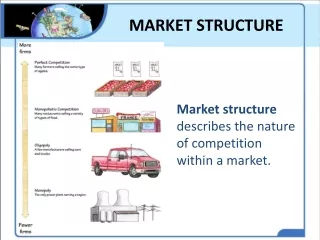

Market Structure. The four market structures perfect competition monopoly monopolistic competition oligopoly Classifying markets number of firms freedom of entry to industry nature of product nature of demand curve. The Degree of Competition. Market Structures. Assumptions

E N D

The four market structures perfect competition monopoly monopolistic competition oligopoly Classifying markets number of firms freedom of entry to industry nature of product nature of demand curve The Degree ofCompetition

Assumptions firms are price takers freedom of entry identical products perfect knowledge Perfect Competition

Total revenue (TR) How much does the firm receive for the sale of the total output? TR = P × Q Average revenue (AR) How much does the firm receive for the sale of one typical unit of output? AR = TR/Q Marginal revenue (MR) How much does the firm receive for the sale of one additional unit of output? MR = ΔTR/ΔQ The Revenue ofCompetitive Firm

Includes all the opportunity costs of making its output of goods and services. Explicit costs: input costs that require a direct outlay of money by the firm (e.g. opportunity cost of $100 electricity fee) Implicit costs: input costs that do not require an outlay of money by the firm (e.g. opportunity cost of renting out building) Cost of Production

The firm will want to produce the quantity that maximizes the difference between total revenue and total cost. Occurs at the quantity where marginal revenue equals marginal cost (MR=MC). Why don’t the firm just produce the maximum quantity? Profit Maximization

Short-run equilibrium of industry and firm under perfect competition £ MC AC S D = AR Pe AR = MR AC D O Q (thousands) (b) Firm Firm is a price taker. Price is given by the market. P O Qe Q (millions) (a) Industry

When MR > MC, increase Q When MR < MC, decrease Q When MR = MC, profit is maximized Profit Maximization

S1 Se LRAC P1 AR1 D1 PL ARL DL D Long-run equilibrium Profits return to normal New firms enter P £ Supernormal profits O O QL Q (thousands) Q (millions) (a) Industry (b) Firm

Shut down (short-run decision) Exit (long-run decision) Which costs are relevant? If the firm shuts down, it only incurs fixed cost, which is sunk and cannot be recovered. Relevant cost in the short run is variable cost. Produce or shut down – the short-run

The firm shuts down if the revenue it gets from producing is less than the variable cost of production. Shut down if TR < VC Shut down if TR/Q < VC/Q Shut down if P < AVC As long as P ≥ AVC (or TR ≥ TVC), the firm should operate even if it is losing money (loss-minimizing) Produce or shut down- the short-run

In the long run, the firm exits if the revenue it would get from producing is less than its total cost. Exit if TR < TC Exit if TR/Q < TC/Q Exit if P < ATC A firm will enter the industry if such an action would be profitable. Enter or exit– the long run

A firm that is the sole seller of a product for which no close substitutes exist. The firm is protected from competitors by barriers that prevent entry from other firms Monopoly

Monopoly resources Government-created monopolies Natural monopolies (economies of scale) Product differentiation and brand loyalty Aggressive tactics Lower costs for an established firm Barriers to entry

Profit maximising under monopoly Total profit AC AR AC AR £ MC Profit maximised at output of Qm (where MC = MR) MR Qm O Q

MR = MC (true for all firms!) In a competitive firm, P = MR Profit maximization leads to P = MC → P = MC = MR For a monopoly, P > MR Profit maximization leads to P > MC Why? Profit Maximizationunder Monopoly

Equilibrium under PC &Monopoly – the same MC curve P2 £ MC ( = supply under perfect competition) Comparison with Perfect competition P1 AR = D MR Q1 Q2 O Q

A situation where there are a lot of firms competing with their own market segment Each firm has some discretion as to what price to charge for its products Monopolistic Competition

Assumptions Independence Freedom of entry Product differentiation Monopolistic Competition

Monopolistic Competition – Short run equilibrium MC AC AR =D MR £ Ps ACs O Qs Q

Monopolistic Competition – Long run equilibrium LRMC LRAC ARL=DL MRL £ New firms entering the industry reduce demand for each individual firm. Price falls to PL PL O QL Q

A few firms share a large proportion of the market Key features of oligopoly barriers to entry interdependence of firms Competition versus collusion Collusive oligopoly: cartels Oligopoly

Profit-maximising cartel Industry MC £ Industry profit maximised at Q1 and P1. P1 Members must agree to restrict total output to Q1. Industry D = AR Industry MR Q1 O Q

Few firms Open with each other Similar production methods and average costs Similar products Dominant firm Significant entry barriers Stable market No government measures to curb collusion Factors favoring collusion