Download

1 / 27

270 likes | 290 Views

Evaluate the present value of a consultancy contract with payments spread over 5 years and calculate the cost of capital for a company. Explore market efficiency and lessons learned. Available in English.

E N D

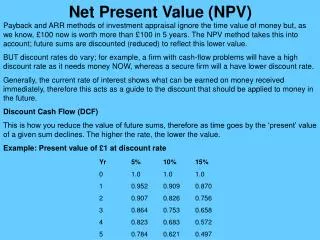

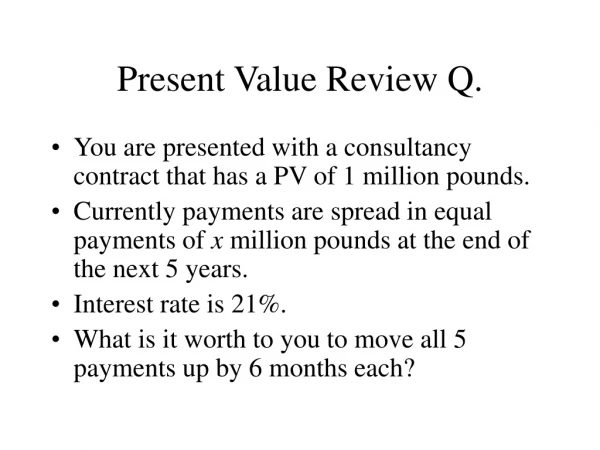

Present Value Review Q. • You are presented with a consultancy contract that has a PV of 1 million pounds. • Currently payments are spread in equal payments of x million pounds at the end of the next 5 years. • Interest rate is 21%. • What is it worth to you to move all 5 payments up by 6 months each?

Cost of Capital Cost of Capital - The return the firm’s investors could expect to earn if they invested in securities with comparable degrees of risk. Capital Structure - The firm’s mix of long term financing and equity financing.

Cost of Capital Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital?

Cost of Capital Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital?

Cost of Capital Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital? Interest is tax deductible. Given a 35% tax rate, debt only costs us 5.2% (i.e. 8 % x .65).

WACC Weighted Average Cost of Capital (WACC) - The expected rate of return on a portfolio of all the firm’s securities. Company cost of capital = Weighted average of debt and equity returns.

WACC • Taxes are an important consideration in the company cost of capital because interest payments are deducted from income before tax is calculated.

WACC Weighted -average cost of capital=

Required Rates of Return Dividend Discount Model Cost of Equity Perpetuity Growth Model = solve for re

WACC Issues in Using WACC Debt has two costs. 1)return on debt and 2)increased cost of equity demanded due to the increase in risk (lower percent of assets in equity) • Betas may change with capital structure • Corporate taxes complicate the analysis and may change our decision

Question: Why doesn’t it cost you to borrow at the rate on debt? • Answer from the previous slide. • The rate it costs you is not the rate it costs to borrow!! • It is both the interest AND the increased risk of equity.

Topics Covered • Investment Decision vs. Financing Decision • Market Efficiency • Weak form efficiency • Semi-strong form efficiency • Strong form efficiency • Lessons of Market Efficiency

Investment vs. Financing • Investment decision are made based on the risk of the project, with total disregard for how the project will be financed (flotation costs being the exception). • Financing decisions are made based on the conditions in the capital markets, with little consideration for the investment being made.

Market Efficiency Market Efficiency Theory Capital markets reflect all relevant information. You cannot consistently earn excess profits. Efficient Capital Markets - Financial markets in which security prices rapidly reflect all relevant information about asset values. Random Walk - Security prices change randomly, with no predictable trends or patterns.

Random Walk Theory • The movement of stock prices from day to day DO NOT reflect any pattern. • Statistically speaking, the movement of stock prices is random (skewed positive over the long term).

Random Walk Theory Coin Toss Game Heads $106.09 Heads $103.00 $100.43 Tails $100.00 Heads $100.43 $97.50 Tails $95.06 Tails

Market Efficiency Technical Analysts - Investors who attempt to identify over- or undervalued stocks by searching for patterns in past prices. Fundamental Analysts - Analysts who attempt to fund under- or overvalued securities by analyzing fundamental information, such as earnings, asset values, and business prospects. Once a profit making opportunity is discovered, it will be competed away.

Market Efficiency Weak Form Efficiency - Market prices rapidly reflect all information contained in the history of past prices. Semi-Strong Form Efficiency - Market prices reflect all publicly available information. Strong Form Efficiency - Market prices reflect all information that could in principle be used to determine true value.

Todd’s trip to work • Two paths to work, the Exe-bridges or Exwick. • There is construction on the Exe-bridge path starting on Friday. • Weak form of travel efficiency, after a day or so paths will take the same time. • Semi-Strong form, if announced beforehand, that day paths will take the same time. • Strong form, as long as one of the city planners know, that day paths will take the same time.

Lessons of Market Efficiency • Markets have no memory • Trust market prices • There are no financial illusions • Do it yourself diversification (worry about transaction costs).

Behavioral Finance • We live in an imperfect world with imperfect people. • What are the problems people face in dealing with problems?

Mental Accounting • Where the money comes from matters: mental accounting. • Have a $200 ticket to the superbowl and lost it. Do you buy another one? How about you are just about to buy a ticket to the superbowl and discover that you are missing $200. Do you still buy it? • Do you go across town when you find that you can pay £985 instead of £999 on a computer? How about if you can pay £14 instead of £28 on a lamp? How about free instead of £14?

Loss Aversion • Imagine that you have just been given £1000. Option A you gain £500. Option B you flip a coin and gain £1000 if it is heads nothing if it is tails. • Imagine that you have just been given £2000. Option A you lose £500. Option B you flip a coin and lose £1000 if it is tails nothing if it is heads. • One may hold onto assets longer to avoid a loss. • Sunk cost does matter!

Status Quo Bias • People invest in something they already invested in or already have. • Your brother sends you tickets to the World Series. You can sell them to a stranger how much would you be willing to part with them for. • Your brother gives you some money. How much would you be willing to spend on World Series tickets.

Understanding Bayes-Rule • Monty Hall problem: • You have three doors. Only one has a prize. Choose one. • Monty opens one of the other two doors to reveal nothing. • He then offers you to switch to the other door. Do you switch?

Implications • Does this mean we don’t have efficient markets?