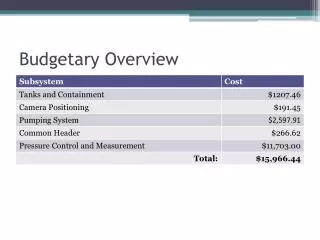

Chapter 18: Budgetary control

Chapter 18: Budgetary control. On completion of this topic you should be able to Describe the main stages in budgetary control Differentiate between fixed and flexible budgets Explain the purpose of budgetary control and the requirements for an effective system

Chapter 18: Budgetary control

E N D

Presentation Transcript

Chapter 18: Budgetary control • On completion of this topic you should be able to • Describe the main stages in budgetary control • Differentiate between fixed and flexible budgets • Explain the purpose of budgetary control and the requirements for an effective system • Describe the advantages and disadvantages of budgetary control • Independent study • Study Chapter 18 • Progress test and practice questions(s) as set Business Accounting

The story so far … • Unlike financial accounting, there are no statutory regulations governing the preparation of management accounting information, as it is intended for internal users • One advantage is that information can be produced about future financial periods • We have already seen that cost accounting techniques can use actual (past) costs or budgeted (future) costs • This is very important as planning and control are essential if a business is to make a profit Business Accounting

Budgetary control • Budgetary controlis ‘the process by which financial control is exercised by managers preparing budgets for revenue and expenditure for each function of the organization in advance of an accounting period. It involves the continuous comparison of actual performance against the budget to ensure the plan is achieved or to provide a basis for its revision’ (Collis and Hussey, 2007, p. 309) Business Accounting

Budgets and budget centres • A budget is ‘a quantitative or financial statement, that contains the detailed plans and policies to be pursued during a future accounting period’ (Collis and Hussey, 2007, p. 310) • A budget centre is ‘a designated part of an entity for which budgets are prepared and controlled by a manager’ (Collis and Hussey, 2007, p. 310) Business Accounting

Variances • Once the budget period begins, each manager compares the actual performance of his/her budget centre against the budget and takes action to remedy any controllable adverse variances • A variance is ‘the difference between the predetermined cost and the actual cost, or the difference between the predetermine revenue and the actual revenue’ (Collis and Hussey, 2007, p. 311) • An adverse variance is anunfavourable difference Business Accounting

Main requirements for an effective system of budgetary control • A sound and clearly defined organization with managers’ responsibilities clearly defined • Effective accounting records and procedures that are clearly understood and applied • Support and commitment of top management for the system of budgetary control • Education/training of managers in the development, interpretation and use of budgets • Revision of budgets where amendments are needed to make them appropriate and useful (continued) Business Accounting

Main requirements for an effective system of budgetary control (continued) • Recognition that budgetary control is a management activity and not an accounting exercise • Participation of managers in the budgetary control system • An information system that provides data for managers so they can make realistic predictions • Correct integration of budgets and their effective communication to managers • Setting of budgets that are reasonable and achievable Business Accounting

Main stages in budgetary control Business Accounting

Exercise 1Role of assumptions in business planning • In order to set realistic financial plans, there needs to be a consultation process, so that management can set out their assumptions about what is going to happen to the firm’s markets and the business environment • Required • Using knowledge you have gained from other modules, jot down the key factors that managers should consider before setting their financial plans for the forthcoming period Business Accounting

Solution 1Role of assumptions in business planning Key factors include assumptions about • Changes in the size of the market and their market share • Competitors’ strategies • Changes in interest rates and sources of funding • Increases in the cost and availability of energy, materials and labour • Changes in legal, social or environmental factors that will affect the demand for the organisation’s products/services • Effects of the activities of other related organisations (eg major customers or suppliers) Business Accounting

Objectives, strategies and plans • The overall purpose of budgetary control is to help managers plan and control the use of resources in a systematic and logical manner to ensure that they achieve their financial objectives • Profit satisficing (making a satisfactory level of profit) • Profit maximisation (making the maximum profit) • Having made their assumptions about the forthcoming period, the next stage is to set out their financial strategies in detail by preparing financial and non-financial budgets that cover every aspect of the firm’s activities Business Accounting

ExampleNon-financial and financial budgets Business Accounting

Methods for setting budgets • In incremental budgeting managers add a percentage to the previous period’s budget to take account of expected changes in price levels • But this is unlikely to create a budget that is relevant to the particular conditions expected and non-recurring revenue and/or non-recurring expenditure will be included • In zero-base budgeting managers start from zero, building each figure into the budget where it can be justified from the expected conditions and policies • This makes the budget more relevant than incremental budgeting Business Accounting

Interrelationship of budgets • Functional budgets are drawn up for each department or function in the business by the specific functional manager • Non-functional budgets are also needed (eg capital expenditure budget; cash flow budget; budgeted profit and loss account; budgeted balance sheet) and these require contributions from various managers and the accountant • The master budget incorporates all the budgets and is the final coordinated budget for the period Business Accounting

Types of budget • A fixed budget is one that is not changed if the activity level differs from the planned level • Disadvantage is that if the actual activity level is higher than planned, an adverse cost variance may be due simply to the increase in variable costs at this level, so the budget becomes irrelevant • A flexible budget is designed to change with the level of activity to reflect the different behaviour of fixed and variable costs • Advantage is that any cost variance can only be due to an increase or decrease in fixed costs Business Accounting

Exercise 2Variance analysis • Variance analysis is the investigation of the factors that have caused the differences between the actual and budgeted figures • A favourable variance is where actual performance is better than planned • An adverse variance is where actual performance is worse than planned (eg costs are higher or revenue is lower) • Required • Complete the June budget report for Jersey Flowers Ltd, indicating whether the variances are favourable or adverse Business Accounting

Pro forma Jersey Flowers Ltd Budget report for June Business Accounting

Solution 2 Jersey Flowers Ltd Budget report for June Business Accounting

Advantages of budgetary control • Co-ordination of all functions and activities • Responsibility accounting - information is provided to managers responsible for revenue and expenditure • Utilisation of resources - capital and effort are used to achieve the financial objectives • Motivation of managers through the use of clearly defined objectives and monitoring of achievement • Planning ahead gives time to take corrective action • Establishes a system of control if plans are reviewed regularly against actual • Transfer of authority to individual managers for decisions Business Accounting

Disadvantages of budgetary control • Set in stone - managers may be constrained by the original budget (eg make no attempt to spend less than maximum or exceed target income) • Time consuming process may deflect managers from their prime responsibilities of running the business • Unrealistic if fixed budgets are set and actual activity level is not as planned • Disillusioning for managers if fixed budgets are set and not achieved merely due to changes in activity • Demotivating for managers if budgets are imposed by top management with no consultation Business Accounting

Conclusions • An effective system of budgetary control helps managers plan and control the use of resources in a systematic and logical manner • Planning helps co-ordinate the activities of the business • Control is achieved through the frequent monitoring of progress against the plan by managers of budget centres, and taking corrective action where necessary • It is a communication system • Financial objectives and constraints are communicated to managers of budget centres and regular monitoring keeps management informed of progress towards objectives Business Accounting