AP Macroeconomics

150 likes | 356 Views

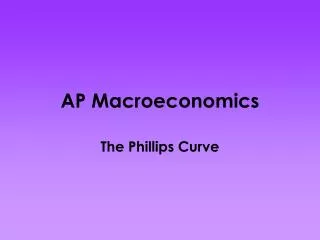

AP Macroeconomics. The Phillips Curve. The Phillips Curve (hypothetical example). π%. . 4%. . 2%. PC. 5%. 7%. u%. Note: Inflation Expectations are held constant. Trouble for the Phillips Curve DO NOT WRITE DOWN.

AP Macroeconomics

E N D

Presentation Transcript

AP Macroeconomics The Phillips Curve

The Phillips Curve(hypothetical example) π% . 4% . 2% PC 5% 7% u% Note: Inflation Expectations are held constant

Trouble for the Phillips CurveDO NOT WRITE DOWN • In the 1970’s the United States experienced concurrent high u% & π%, a condition known as stagflation. 1976 American Nobel Prize economist Milton Friedman saw stagflation as disproof of the stable Phillips Curve. Instead of a trade-off between u% & π%, Friedman and 2006 Nobel Prize recipient Edmund Phelps believed that the natural rate of unemployment u% was independent of the π%. This independent relationship is now referred to as the Long-Run Phillips Curve.

The Long-Run Phillips Curve (LRPC) • Because the Long-Run Phillips Curve exists at the natural rate of unemployment (un), structural changes in the economy that affect un will also cause the LRPC to shift. • Increases in un will shift LRPC • Decreases in un will shift LRPC • The key to understanding shifts in the Phillips curve is inverse relationships

The Long-Run Phillips Curve π% LRPC un% u% Note: Natural rate of unemployment is held constant

The Short-Run Phillips Curve (SRPC) • Today many economists reject the concept of a stable Phillips curve, but accept that there may be a short-term trade-off between u% & π% given stable inflation expectations. Most believe that in the long-run u% & π% are independent at the natural rate of unemployment. Modern analysis shows that the SRPC may shift left or right.

Increase in AD = Up/left movement along SRPC π% PL LRAS . . SRAS SRPC . . P1 π1 P π AD1 AD un u u% Y YF GDPR C↑, IG↑, G↑ and/or XN↑ .: AD .: GDPR↑ & PL↑ .: u%↓ & π%↑ .: up/left along SRPC

Decrease in AD = Down/right along SRPC LRAS PL π% . SRAS SRPC . . . P π P1 π1 AD AD1 YF Y GDPR u un u% C↓, IG↓, G↓ and/or XN↓ .: AD .: GDPR↓ & PL↓ .: u%↑ & π%↓ .: down/right along SRPC

SRAS = SRPC SRAS SRPC PL π% LRPC LRAS . . SRAS1 SRPC1 . . π P π1 P1 AD un u u% Y YF GDPR Inflationary Expectations↓, Input Prices↓, Productivity↑, Business Taxes↓, and/or Deregulation .: SRAS .: GDPR↑ & PL↓ .: u%↓ & π%↓ .: SRPC (Disinflation)

SRAS = SRPC SRAS1 SRPC1 π% PL LRAS LRPC SRAS SRPC . . . . P1 π1 P π AD Y1 YF GDPR un u1 u% Inflationary Expectations↑, Input Prices↑, Productivity↓, Business Taxes↑, and/or Increased Regulation .: SRAS .: GDPR↓ & PL↑ .: u%↑ & π%↑ .: SRPC (Stagflation)

Reconciling the LRPC and SRPC In the long-run, the inflation rate at B (π1%) becomes the new expected inflation rate (π1^%), and the economy returns to the natural rate of unemployment (point C). π% LRPC C B π1% A π % SRPC (π1^ %) SRPC (π^ %) u% Assume that either the government or the central bank enacts an expansionary policy to reduce the unemployment rate below its natural rate at point A. In the short-run, assuming the policy is successful, inflation occurs and unemployment decreases as the economy moves from A to B. u% uN%

Reconciling the LRPC and SRPC In the long-run, the inflation rate at B (π1%) becomes the new expected inflation rate (π1^%), and the economy, once again, returns to the natural rate of unemployment (point C). π% Now assume that either the government or the central bank enacts a contractionary policy to reduce inflation from it’s current rate at point A LRPC A π % C π1% B SRPC (π1^ %) In the short-run, assuming the policy is successful, disinflation occurs and unemployment increases as the economy moves from A to B. SRPC (π^ %) u% u% uN%

Relating Phillips Curve to AS/AD • Changes in the AS/AD model can also be seen in the Phillips Curves • An easy way to understand how changes in the AS/AD model affect the Phillips Curve is to think of the two sets of graphs as mirror images.

Summary • There is a short-run trade off between u% & π%. This is referred to as a short-run Phillips Curve (SRPC) • In the long-run, no trade-off exists between u% & π%. This is referred to as the long-run Phillips Curve (LRPC) • The LRPC exists at the natural rate of unemployment (un). • un ↑ .: LRPC • un ↓ .: LRPC

ΔC, ΔIG, ΔG, and/or ΔXN = Δ AD = Δ along SRPC • AD .: GDPR↑ & PL↑ .: u%↓ & π%↑ .: up/left along SRPC • AD .: GDPR↓ & PL↓ .: u%↑ & π%↓ .: down/right along SRPC • Δ Input Prices, Δ Productivity, Δ Business Taxes and/or Δ Regulation = Δ SRAS = Δ SRPC • SRAS .: GDPR↑ & PL↓ .: u%↓ & π%↓ .: SRPC • SRAS .: GDPR↓ & PL ↑ .: u%↑ & π%↑.: SRPC