Download

1 / 13

130 likes | 272 Views

The Impact of Merger Announcements on Stock P rices: The Application of Event-Study Analysis to a Historical Issue. Discussion held on 26 th April 2003 Economics and Business Historical Society Conference Gerhard Kling Department of Economics University of Tuebingen. I. T. R.

E N D

The Impact of Merger Announcements on Stock Prices:The Application of Event-Study Analysis to a Historical Issue Discussion held on 26th April 2003 Economics and Business Historical Society Conference Gerhard Kling Department of Economics University of Tuebingen

I T R C Overview Introduction Theoretical Background Empirical Results Concluding Remarks Merger Paradox Event Study CMR model Abnormal returns Cumulated Effects Cross-sectional model Pros and cons Further research Gerhard Kling

I T R C Introduction Empirical finding that acquiring firms loose from mergers What is the Merger Paradox? Can we detect the merger paradox in the first phase of globalization? Event Study method + draw a sample (year 1908) Gerhard Kling

I T R C Theoretical background • Basic concept of event-studies • normal returns - up to six models • definition of the estimation period • construction of the event period Caution! • deriving the test statistics - two approaches! • Why do we choose the CMR model? • lacking market index • simple model - modifications easily embedded • similar results (see Warner and Brown 1980, 1985) Gerhard Kling

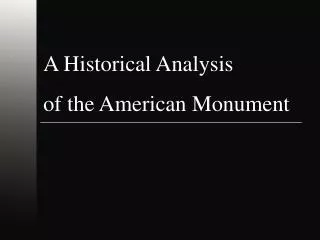

I T R C Illustration of CMR and AR • ARit +error term eit return Rit return of stock i at t upper and lower bound estimation period event period time t Gerhard Kling event day

I T R C AR and CAR Measurement • normal range of returns • returns outside range - abnormal returns AR • accumulation of AR over firms and over time • whole effect should be captured • which group wins? • division into subgroups (target; acquiring firm) Gerhard Kling

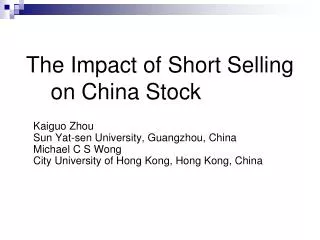

I T R C Target and acquiring firms Gerhard Kling

I T R C Results - What can we learn? • Both groups gain from mergers • Merger paradox rejected • Reasons unknown - further research • Adaptation takes only a few days • Market is highly informationally efficient • Pre-merger gains - insiders? • Not enough insights - cross-sectional model Gerhard Kling

I T R C Cross-sectional model • Objective: What influences success of mergers? • Explanatory variables: • age of the firm (experience) • market capitalization (firm size) • growth rate of dividend payment (profitability) • dummies: target, cash payment, change of management, success (approval), lines of business (banking and mining industry) Gerhard Kling

I T R C Gerhard Kling

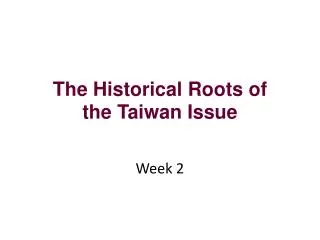

I T R C What do I mean with causality? Success of Merger CAR direct indirect Estimated Normal Return Firm Size Gerhard Kling

I T R C Gerhard Kling

I T R C Concluding remarks • Merger paradox rejected • Additional insights using simultaneous equation model • banking industry exhibits larger gains • targets and acquiring firms do not differ significantly • Insiders versus outsiders • Different ways of disclosure • Does regulation protect outsiders? Gerhard Kling