Download

1 / 17

180 likes | 368 Views

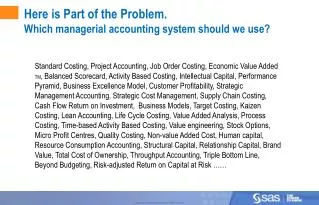

Here is Part of the Problem. Which managerial accounting system should we use?.

E N D

Here is Part of the Problem. Which managerial accounting system should we use? Standard Costing, Project Accounting, Job Order Costing, Economic Value Added TM, Balanced Scorecard, Activity Based Costing, Intellectual Capital, Performance Pyramid, Business Excellence Model, Customer Profitability, Strategic Management Accounting, Strategic Cost Management, Supply Chain Costing, Cash Flow Return on Investment, Business Models, Target Costing, Kaizen Costing, Lean Accounting, Life Cycle Costing, Value Added Analysis, Process Costing, Time-based Activity Based Costing, Value engineering, Stock Options, Micro Profit Centres, Quality Costing, Non-value Added Cost, Human capital, Resource Consumption Accounting, Structural Capital, Relationship Capital, Brand Value, Total Cost of Ownership, Throughput Accounting, Triple Bottom Line, Beyond Budgeting, Risk-adjusted Return on Capital at Risk ……

Here is Part of the Problem. Which managerial accounting system should we use? Standard Costing, Project Accounting, Job Order Costing, Economic Value Added TM, Balanced Scorecard, Activity Based Costing, Intellectual Capital, Performance Pyramid, Business Excellence Model, Customer Profitability, Strategic Management Accounting, Strategic Cost Management, Supply Chain Costing, Cash Flow Return on Investment, Business Models, Target Costing, Kaizen Costing, Lean Accounting, Life Cycle Costing, Value Added Analysis, Process Costing, Time-based Activity Based Costing, Value engineering, Stock Options, Micro Profit Centres, Quality Costing, Non-value Added Cost, Human capital, Resource Consumption Accounting, Structural Capital, Relationship Capital, Brand Value, Total Cost of Ownership, Throughput Accounting, Triple Bottom Line, Beyond Budgeting, Risk-adjusted Return on Capital at Risk …… Even most cost accountants do not understand what the differences are !

Accounting Taxonomy ACCOUNTING Managerial Accounting Financial and Tax Accounting (external reporting) Cost Uses (decision support) Cost Measurement Assigning expense data into costs Collecting cost data Control (feedback) Reporting & analysis Planning (predictive) Concepts, assumptions & issues Methods, Attributes Financial Operational, Quality Segmented profit analysis Variance analysis Budgeting Accountability Managing capacity Managing demand Economic Financial Operational financial operational QUOTATIONS (PRICING), WHAT-IF ANALYSIS SCORECARDS, PERFORMANCE MEASURES

Management Accounting Framework ACCOUNTING Managerial Accounting Financial and Tax Accounting (external reporting) Cost Measurement Cost Uses (decision support) Collecting cost data Assigning cost data Control (feedback) C Reporting & analysis Planning (predictive) Concepts, assumptions & issues B Methods, Attributes E Financial Operational, Quality Segmented profit analysis Variance analysis Budgeting Responsibility & Accountability Financial Operational Managing capacity Managing demand Economic financial operational A QUOTATIONS (PRICING), WHAT-IF ANALYSIS, BUDGETS PERFORMANCEMEASUREMENT D

Cost Measurement / Collecting Cost Data Cost Measurement Collecting Cost Data Assigning Costs Economic measurements financial operational Resource drivers (timesheets, storyboarding) activity dictionary activity drivers activity driver rates (actual vs. standard) output quantities Direct costs: labor routings Direct costs: bill of materials Payroll / wages general ledger purchase price Cost of capital Capital preservation allowance Long-term sustainable vs. specific period expenditures A

Cost Measurement / Assigning Costs Cost measurement Collecting cost data Assigning costs Assignment methods Concepts, assumptions, & issues Period costing Non-period costing Fixed vs. Variable (“viscosity”) sunk costs / depreciation variability / linearity planning horizon update frequency level of aggregation causality (and effect) full absorption costing machine vs. labor intensity precision vs. accuracy vs. ……..relevancy GAAP (regul.) vs. ABC/M historical vs. replacement Project accounting job order costing process accounting throughput accounting kaizan accounting standard costing activity based costing activity based management supply chain costing constraint based costing; total available profit (TAP) feature based costing parametric cost modeling Life cycle costing target costing product phase-in & out/ attributes B

Cost Uses / Control (feedback) Cost Uses Control (feedback) Assessment (insights & learning) Planning (predictive) Financial (spending) operational Developing Budgets (planning) Variance analysis (actual vs. plan ) Productivity analysis capital investment realized benefits tracking unused capacity identification unitized cost-of-outputs trends cost of quality (TQM) six sigma & SPC & ISO9000) Benchmarking Traditional activity-based budgeting Budget -responsibility center accounting Standard cost of: ---direct materials ---direct labor C

Cost Uses / Assessment Cost Uses Control (feedback) Planning (predictive) Assessment (insights & learning) Segmented & Multi-dimensional ...Profit Contribution Analysis Responsibility & Accountability Financial Operational Products / service lines direct product profitability (DPP) shared services / joint service agreements total cost of ownership (TCO) dealer profitability channel profitability customer profitability break-even analysis Benchmarking best practices / lean cost driver analysis throughput $ velocity attributes analysis / value-added analysis cost of quality (COQ) environmental costing Risk management Economic value added (EVA) shareholder value added (SVA) cash flow RONA ROI inventory valuation WEIGHTED SCORECARD (performance measures) D

Cost Uses / Planning (Predictive) Cost Uses Assessment (insights & learning) Planning (predictive) Control (feedback) Managing Capacity (Supply resources) Managing Demand (Outputs & Cost Receivers) Budgeting (see control) Unused capacity management make vs. buy (outsourcing) activity based budgeting (ABB) capital budgeting (allocation) target costing (design for manuf.) business process reengineering supply chain management efficient consumer response (ECR) discrete-event simulation Theory of Constraints (TOC) manpower levels Influencing demand Rationalizing & repositioning Pricing strategies transfer pricing quoted delivery lead times customer order rules bundled services Strategic planning Sourcing mix product offerings service offering channel strategy customer mix QUOTING CUSTOMER ORDERS COST FORECASTING (what-if analysis) E

Source data capture (transactions / bookkeeping) ACCOUNTING Tax Accounting Financial Accounting Managerial Accounting Non-financial data capture Cost Accounting Financial Reporting regulatory compliance Cost Measurement • [e.g., GAAP, IFRS] • Costs of goods sold • Inventory valuation Cost Reporting & Analysis (feedback on performance) Decision Support/ Cost Planning • Fully absorbed & incremental pricing • Driver-based budgeting & rolling financial forecasts • What-if analysis • Product, channel & customer rationalization • Outsourcing & make vs. buy analysis • Spending vs. budget variance analysis • Profitability reporting • Process analysis (e.g., lean, benchmarking, COQ) • Performance measures • Learning; corrective actions The Domain of Costing History Future Low value-add Modest value-add High value-add Source: “A Costing Levels Continuum Maturity Model” by Gary Cokins published by the International Federation of Accountants, 2010

International Federation of Accountants Report Evaluating the Costing Journey: A Costing Levels Continuum Maturity Model By Gary Cokins, SAS Most organizations are typically at lower levels of maturity in adopting progressive managerial accounting practices, methods and systems.

Costing Continuum / Levels of Maturity (most companies are Level 4D and 1P) (1) Descriptive Continuum EXPENSE TRACKING, COST REPORTING and CONSUMPTION RATES (2) Predictive Continuum DEMAND DRIVEN PLANNINGwith CAPACITY SENSITIVITY Unused Capacity Aware Customer Demand Sensitive 8D Improved Treatment of Indirect Costs 7D Unused capacity costs (estimated) 6D Level # Improved Output Information/ Approximate Accuracy Level 6D with Channel and customer profitability Reporting; Cost-to-serve Push Activity- Based costing (ABC); Product costs Output Visibility Process Visibility 5D 4D Blind 3D 2D 1D Standard costing to individual outputs; Project acct; Job order costing Direct costs without (3) and with (4) support costs to output groups process and Lean accounting bookkeeping Source: “A Costing Levels Continuum Maturity Model” by Gary Cokins published by the International Federation of Accountants, 2012

Costing Continuum / Levels of Maturity (most companies are Level 4D and 1P) (1) Descriptive Continuum EXPENSE TRACKING, COST REPORTING and CONSUMPTION RATES (2) Predictive Continuum DEMAND DRIVEN PLANNINGwith CAPACITY SENSITIVITY Simulation Resource Consumption Accounting 5P Level # Time-driven ABC Pull Activity- based Resource Planning 4P Ultimate in consumption rates; 3P (RCA); Level 2P with proportional costing at direct and support depts. % G/L acct. Incremental 2P (TDABC); Forecast driver quantities X time consumption rates; Direct cost focus; Repetitive work conditions 1P (ABRP); Forecast driver quantities X unit consumption rates; Driver based budgeting Source: “A Costing Levels Continuum Maturity Model” by Gary Cokins published by the International Federation of Accountants, 2012

Costing Continuum / Levels of Maturity (most companies are Level 4D and 1P) (1) Descriptive Continuum EXPENSE TRACKING, COST REPORTING and CONSUMPTION RATES (2) Predictive Continuum DEMAND DRIVEN PLANNINGwith CAPACITY SENSITIVITY Unused Capacity Aware Customer Demand Sensitive 8D Improved Treatment of Indirect Costs Simulation 7D Resource Consumption Accounting 5P Unused capacity costs (estimated) 6D Level # Improved Output Information/ Approximate Accuracy Time-driven ABC Pull Activity- based Resource Planning 4P Level 6D with Channel and customer profitability Reporting; Cost-to-serve Ultimate in consumption rates; 3P Push Activity- Based costing (ABC); Product costs Output Visibility (RCA); Level 2P with proportional costing at direct and support depts. % G/L acct. Incremental Process Visibility 5D 2P 4D Blind (TDABC); Forecast driver quantities X time consumption rates; Direct cost focus; Repetitive work conditions 3D 2D 1P 1D Standard costing to individual outputs; Project acct; Job order costing (ABRP); Forecast driver quantities X unit consumption rates; Driver based budgeting Direct costs without (3) and with (4) support costs to output groups process and Lean accounting bookkeeping Source: “A Costing Levels Continuum Maturity Model” by Gary Cokins published by the International Federation of Accountants, 2012

Hierarchical Objectives High Profitability Low Costs High Sales High Customer Service Low Unit Costs Quality Product High Throughput Low Inventory High Utilization Fast Response Many products Less Variability Short Cycle Times Low Utilization High Inventory More Variability Source: Dr. Nico Vandaele; Katholieke Universeit Leuven

Financial and Operational Flows Source: Dr. Nico Vandaele; Katholieke Universeit Leuven