Download

1 / 31

320 likes | 714 Views

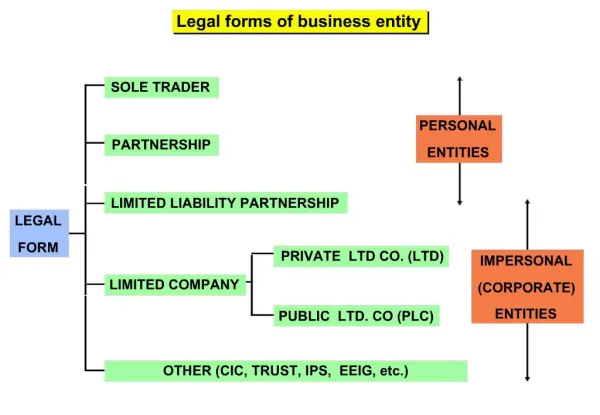

Choice of Business Entity. Jack Cohen, CPA Asset Protection IncSmart.biz Inc. Types of Entities. C CORPORATION. S CORPORATION. LLC. PARTNERSHIP. SOLE PROPRIETOR. Identifying the Objectives Items To consider What’s at Risk?. Tax Savings Asset Protection Management

E N D

Choice ofBusiness Entity Jack Cohen, CPA Asset Protection IncSmart.biz Inc

Types of Entities C CORPORATION S CORPORATION LLC PARTNERSHIP SOLE PROPRIETOR

Identifying the Objectives Items To consider What’s at Risk? • Tax Savings • Asset Protection • Management • Capitalization • Exit Strategies

Chances of IRS AuditF.Y. 06 • Form 1040 Sch. ‘C’ > $100,000 = 3.90% • 1120 < 10 Mill. Assets = .80% • 1120-S = .38% • 1065 = .36%

Tax Savings • Income Tax • Payroll Taxes • Self Employment • Gift and Estate Taxes

Asset Protection From: • Business Activities Risk • Management Actions • Employee Actions

Management • Will management be expanded? • How will management disputes be resolved? • How will they be compensated? • Equity participation • Compensation • Additional fringe benefits

Capitalization – What Form Should it Take? Initial Capitalization Debt • Bank loans • Home equity loans • Family and friends Equity • Corporation- stock • Partnership- partner interest • Limited liability company- member interest Debt Pros • Interest tax deductible • No ownership dilution • Flexible rates and terms • Increases return on equity • Establishes credit rating Cons • Personal guarantees • Monthly periodic payments Equity Pros • Minimum cash outflows • Ease of transfer • Large source of capital Con • Ownership dilution

Tax Tip • On corporations capitalize for the least amount possible. • Have company “borrow money” from you. • Example • $1,000 Stock • $99,000 Loan • $100,000 Total Capital

Exit Strategies • Company Stock redemptions • Competitor Merger Acquisition Asset sale Stock sale • Family members Gifting Death transfers Acquisition • Management Management buy-out (MBO) Management buy-in (MBI)

Proprietorships – Non Tax Considerations • Simplicity of form • Unlimited personal liability • Continuity of existence and transferability of ownership • Limited ownership

Proprietorships – Tax Considerations Tax Advantages • Wages paid to children • At-risk rules • Fringe benefit via spouse employment • No double taxation Tax Disadvantages • Self-employment tax • All income taxed at individual level • Lack of fringe benefits • Hobby loss rule

Proprietorships – Taxation • Tax rate depends on filing status • No withholding requirements • 15.3% self-employment tax • Total net income determines income tax & Social Security liabilities • File Schedule C with 1040: Business profit & loss

Taxation of LLC • Single Member LLC: Disregarded Entity • Rev Ruling 99-5; 99-6 • SMLLC – Husband or • Husband & Spouse • Reported on Form 1040 • Can not have any other unrelated owner • “Check the Box” Rules • Partnership taxation is default (minimum two members) • May choose to be taxed as a corporation • S Corp or C Corp

Real Estate Tip • For Maximum Asset Protection Separate SMLLC for each property. • Put Real Estate in SMLLC.

Partnership – Formation Issues • Partnership agreement or operating agreement • Buy/Sell agreement • Contributions of Assets • Limited Life • Liability Issues • LLP vs. General Partnership

Partnership – Tax Considerations Tax Advantages • Tax basis from debt • Basis adjustment when partnership interest acquired • Tax-free contributions and distributions of property • Ability to make special elections • No entity level of tax Tax Disadvantages • Inability to reduce payroll taxes • Unfavorable tax treatment of fringe benefits • Lack of flexibility to select a tax year end • Technical Termination

Partnership Taxation – Summary • IRS Form 1065 • Generates K-1 • No “double taxation” • Self-employment tax • Informational tax return: entity does not pay tax • Taxed at partner level • Income is taxable for FICA

S Corporation – Tax Considerations Tax Advantages • No double taxation • Pass-through to shareholders • No excessive compensation • Ability to reduce payroll taxes • Ability to use cash method • Tax-free withdrawals of equity • Possible ordinary loss treatment for stock losses Tax Disadvantages • Fringe benefits • Tax year-end • Built-in gains tax • Excess passive income • Basis is reduced even if no tax benefit

‘S’ CorporationWho Can Be Shareholder? • U.S. citizen • Estates • Single Member LLC • 501 (c) (3) Charities • Qualified Pension plans • Qualified Profit Sharing plans

‘S’ CorporationWho Can not Be shareholder? • Corporations • Partnerships • LLC’s (not SMLLC) • IRA’S & Roth’s • Sep IRA’s & SIMPLE IRA’s • Non-Resident Aliens

S Corporation Taxation – Summary • Must make election: Form 2553 • Files Form 1120-S • Generates K-1 • Informational return • Taxed at shareholder level • Income tax only on proportionate share of income: No FICA • No corporate tax on sale of assets or liquidation

Partnership vs. S Corp– Treatment • Social Security • General partners pay FICA on K-1 income • Shareholders S Corp K-1 income: no FICA

Social SecurityHow Much Does Sub ‘S’ Owner Pay? • In 2000 78.9% of ‘S’ - more than 50% owned by single shareholder. • Compensation To be Reasonable • 36,00 taxpayers > $100,000 profits = 0 compensation. • 2001 – Owner salaries 41.5% of operating profits. • 2000 – ‘S’ corporations paid 5.7 billion less than if sole proprietors

Partnership vs. S Corp – Treatment Distributions • Partnership: disproportionate distributions allowed • S Corp: no disproportionate distributions Ownership Interest • S Corp: ownership restricted • No more than 100 shareholders • Individuals, estates, certain types of trusts • No foreign shareholders • Only one class of stock allowed • Partnership: no restrictions

C Corporations – Non Tax Considerations • Limited liability • Administrative burden • Management and control • Continuity of existence and transferability of ownership

C Corporations – Tax Considerations Tax Advantages • Lower tax rates at many income levels • Net income not subject to Social Security • Takes maximum advantage of fringe benefit deductions Tax Disadvantages • Double taxation of corporate earnings • Excessive compensation • Personal service corporate limitations • Personal holding company accumulated earnings tax- penalty taxes • Limitations caused by corporate ownership changes

C Corporation – Employee Benefits • Salaries • Reasonable salaries • Garnishment limitations • Medical benefits • Medical reimbursement plans • Health savings accounts • Retirement benefits • Educational benefits • Other benefits

C Corporations – Taxation • Separate entity – separate taxpayer • Files IRS Form 1120 • Calendar or fiscal year • Dividends not deductible: double tax on profits • Isolates state operations for nexus • Payroll • Sales • Property

THANK YOU For more information, visithttp://incsmart.biz