Download

1 / 8

80 likes | 183 Views

Explore historical viewpoints on money lending, alongside modern regulatory measures to combat reckless credit and over-indebtedness. Learn about the National Credit Act in South Africa and key aspects promoting fairness in the credit market.

E N D

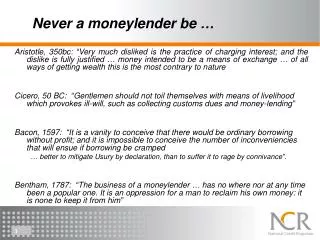

Never a moneylender be … Aristotle, 350bc: “Very much disliked is the practice of charging interest; and the dislike is fully justified … money intended to be a means of exchange … of all ways of getting wealth this is the most contrary to nature Cicero, 50 BC: “Gentlemen should not toil themselves with means of livelihood which provokes ill-will, such as collecting customs dues and money-lending” Bacon, 1597: “It is a vanity to conceive that there would be ordinary borrowing without profit; and it is impossible to conceive the number of inconveniencies that will ensue if borrowing be cramped … better to mitigate Usury by declaration, than to suffer it to rage by connivance”. Bentham, 1787: “The business of a moneylender … has no where nor at any time been a popular one. It is an oppression for a man to reclaim his own money: it is none to keep it from him”

National Credit RegulatorSouth Africa Regulatory measures to prevent reckless credit, deal with over-indebtedness ... & improve transparency & fairness Gabriel Davel 21 February 2008

The National Credit ActMeasures to combat reckless lending & over-indebtedness • Affordability assessments • reasonable steps to assess ability to meet obligations under agreement, based consumer’s existing financial means, prospects and obligations per information available to lender at the time of approving the loan • If reckless, • Court may suspend enforcement; credit provider must indicate to court that credit was not granted recklessly; Court can refer a consumer to a debt counselor • but: consumers must disclose details of all debts • Debt counselling • Develop debt repayment plan, either consented by providers or approved by courts + provide on-going support to consumer • In duplum rule’ • limit interest & fees after default to 100% of outstanding amount at point of default … limit ‘debt farming’

Key aspects that deal with fairness in credit market … • Negative option marketing & automatic increases in credit limits prohibited • Compulsory, standard 1-page pre-agreement quote on all agreements • “Penalty interest” prohibited; “In Duplum” rule introduced; Single premium credit life insurance prohibited • Changed structure of disclosure, away from “APR”, to separate disclosure & regulation of interest, initiation fees & monthly service fees • Prohibited arrangements that give one credit provider a preference over others, particularly in payment system or through payroll deduction • Prohibit specific contractual clauses that are considered unfair (not “unconscionable contract approach) • Create Register of Credit Agreements & regulate credit bureaus … to provide complete & accurate picture of payment profile & indebtedness Fairness, predictability, consistency …

Why is the market for low value credit dysfunctional ? Question 1: Are there any legal or systemic failures that allow a credit provider to lend beyond a consumer’s ability to repay, yet still recover loan repayments? That allow the reckless lender to pass the write-off on to another party? Question 2: Are there any legal, regulatory or institutional reasons why main stream commercial providers are not willing or able to provide micro-finance … Why is credit market for low value transactions operating inefficiently / uncompetitively ?

Thank You ! www.ncr.org.za

Overview of Act Interest & fees Reckless lending Marketing practices & disclosure National Credit Act Enforcement & debt collection Agreements & quotes Unlawful agreements, provisions Debt counsellors Credit Bureaus National Credit Register

Regulatory reform Uniform treatment & disclosure across all types of agreement Standardisation, comparability Access to redress Enforcement Improve information sharing between credit providers Regulatory issues