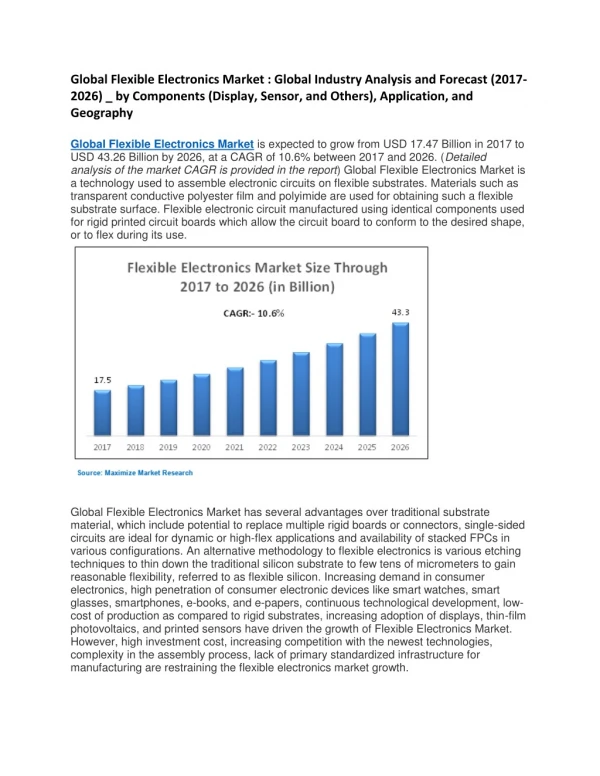

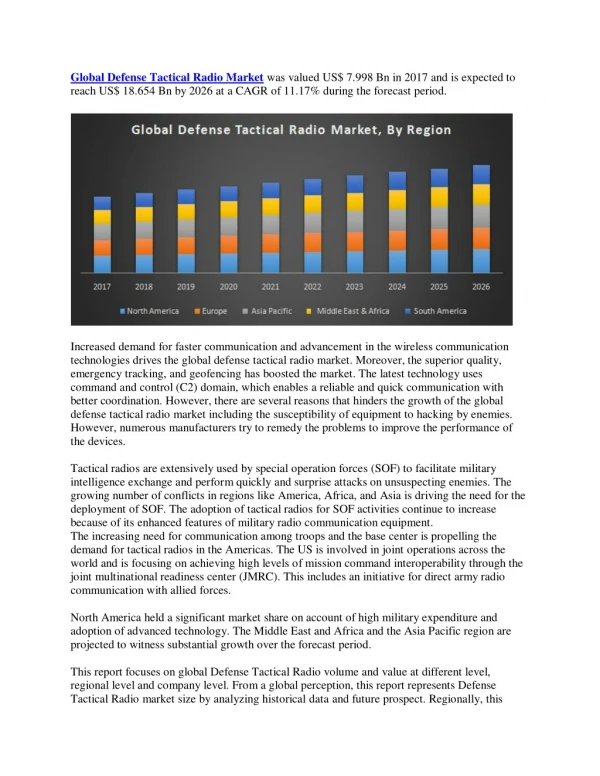

Download

1 / 3

0 likes | 2 Views

The global defense electronics obsolescence market was valued at USD 2,530.1 million in 2024 and is projected to grow from USD 2,736.3 million in 2025 to USD 5,005.7 million by 2032, exhibiting a CAGR of 9.0% during the forecast period. North America dominated the market in 2024, accounting for 45.6% of global revenue, driven by robust military modernization programs and upgrades to legacy systems.

E N D

The global defense electronics obsolescence market was valued at USD 2,530.1 million in 2024 and is projected to grow from USD 2,736.3 million in 2025 to USD 5,005.7 million by 2032, exhibiting a CAGR of 9.0% during the forecast period. North America dominated the market in 2024, accounting for 45.6% of global revenue, driven by robust military modernization programs and upgrades to legacy systems. As defense forces increasingly depend on advanced electronic systems, managing obsolescence has become a critical priority. Governments and defense contractors are focusing on operational readiness and lifecycle management to maintain performance and ensure mission success. Understanding Defense Electronics Obsolescence Defense electronics obsolescence refers to the declining availability and support for electronic components used in military systems. Rapid technological advancements often render key components—such as microprocessors, radar systems, and communication modules—obsolete, leading to operational inefficiencies and heightened security risks. The market addresses these challenges through a range of solutions, including component redesign, reverse engineering, strategic obsolescence forecasting, and integrated lifecycle planning. These strategies are essential across various defense platforms—airborne, naval, and land-based systems—to ensure legacy hardware remains compatible with modern technologies and continues to perform reliably in mission-critical environments. Information Source: https://www.fortunebusinessinsights.com/defense-electronics-obsolescence-market-112861 Key Market Players: Defense Electronics Obsolescence Companies Raytheon Technologies Corporation (U.S.) BAE Systems (U.K.) L3 Harris Technologies Inc. (U.S.) Thales Group (France) Elbit Systems Ltd. (Israel) Lockheed Martin Corporation (U.S.) Northrop Grumman Corporation (U.S.) General Dynamics Corporation (U.S.) Bharat Electronics Ltd. (India) Leonardo S.p.A. (Italy) Market Segmentation: Defense Electronics Obsolescence Landscape The defense electronics obsolescence market is segmented by system type, platform, type of obsolescence, and region. By system, the market includes communication systems, navigation systems, flight control systems, electronic warfare systems, and others. Based on platform, it is categorized into land, naval, and air domains. By type of obsolescence, the market is divided into supply chain obsolescence, functional obsolescence, and technical obsolescence. Regionally, the market covers North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Market Dynamics Driving Factors: Operational Readiness & Lifecycle Management Fuel Market Growth With rising geopolitical tensions and the need for high readiness levels, the demand for efficient obsolescence management has intensified. Lifecycle management now plays a central role in mitigating component obsolescence, reducing maintenance downtime, and enhancing force effectiveness. Defense modernization programs, particularly in the U.S., India, and European Union countries, are prioritizing modular upgrades, digital twins, and long-term support strategies for existing systems. The emphasis on interoperability and supply chain resilience is also encouraging strategic collaborations between defense OEMs and technology providers. Restraints: Complex Supply Chains & High Costs Present Challenges Despite the growth outlook, the market faces significant hurdles. Managing obsolescence requires detailed component tracking, multi-vendor coordination, and expensive redesign or replacement solutions, which may be financially unviable for some defense programs. In addition, the global supply chain disruptions and chip shortages observed post- pandemic continue to impact project timelines and component availability. Industry Developments: Recent developments illustrate the strategic focus on addressing obsolescence challenges: December 2024– A defense contract worth USD 1.2 billion was awarded for the procurement of six Next-Generation Missile Vessels (NGMVs), which integrate

upgraded electronics with stealth and enhanced combat capabilities. This signals a growing emphasis on modernizing aging naval systems with future-ready technology.