Comparing Retirement Plans

20 likes | 59 Views

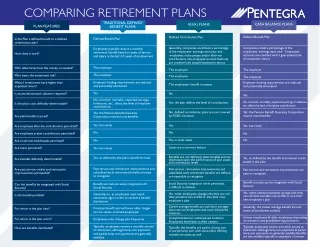

Are you considering starting a retirement plan for your business? You should review plan features to help determine which type of retirement plan will work best for your business and employees.

Comparing Retirement Plans

E N D

Presentation Transcript

COMPARING RETIREMENT PLANS TRADITIONAL DEFINED BENEFIT PLANS CASH BALANCE PLANS 401(K) PLANS PLAN FEATURES Defined Benefit Plan Defined Contribution Plan Defined Benefit Plan Is the Plan a defined benefit or a defined contribution plan? Companies credit a percentage of the employees’ earnings each year Employees’ accounts are credited with a guaranteed rate of investment return Generally, companies contribute a percentage of the employees’ earnings each year and employees make pretax and/or after-tax contributions; the employee account balances are credited with actual investment returns Employees typically receive a monthly retirement benefit based on years of service and salary in the last 3-5 years of employment How does it work? The employer Who determines how the money is invested? The employer The employee The employer Who bears the investment risk? The employee The employer Employer funding requirements are reduced and potentially eliminated Employer funding requirements are reduced and potentially eliminated What if investments have higher than expected return? The employees’ benefit increases Yes No, turnover, mortality, expected earnings, forfeitures, etc , affect the level of employer contributions Is an annual actuarial valuation required? No Yes Is the plan’s cost definitely determinable? No, turnover, mortality, expected earnings, forfeitures, etc, affect the level of employe contributions Yes, the plan defines the level of contributions No, defined contribution plans are not covered by PGBC insurance Yes, the Pension Benefit Guaranty Corporation insures most benefits Yes, the Pension Benefit Guaranty Corporation insures most benefits Are plan benefits insured? Yes, but rarely Yes Yes, but rarely Are employee after-tax contributions permitted? Yes No Are employee pretax contributions permitted? No No Yes, in most cases Loans are a common feature No Are in-service withdrawals permitted? Are loans permitted? Yes, but rarely Benefits are not definitely determinable and are dependant upon the performance of plan assets and contribution levels Yes, as defined by the plan’s benefit formula Yes, as defined by the benefit and interest credit stated in the plan Are benefits definitely determinable? Past service and retroactive improvements and subsidized early retirement benefits are easy to recognize Past service, retroactive improvements and subsidized early retirement benefits are difficult or impossible to recognize Are past service credits and retroactive improvements permissible? Past service and retroactive improvements are easy to recognize Benefit accruals can be integrated with Social Security Social Security integration while permitted, is difficult to achieve Benefit accruals are easily integrated with Social Security Can the benefits be integrated with Social Security? Yes, when vested employees change jobs they can roll their benefits into an IRA or into their new employer’s plan Yes, when employees change jobs they can roll their pensions into an IRA or into their new employer’s plan Generally no, as employees must reach retirement age in order to receive a benefit distribution Is the benefit portable? Career average benefit accruals favor younger, short-service employees and savvy disciplined investors Unsophisticated or undisciplined investors Employees hired later in their careers Generally, the career average benefit accrual treats all employees similarly Final pay benefit accrual favors older, longer service career-oriented employees For whom is the plan best? Career employees & older employees depending on transition and grandfathering provisions For whom is the plan worst? Employees who change jobs frequently Typically, employees receive a monthly annuity at retirement, although lump sum payments and partial lump sum payments are generally available Typically, employees receive a monthly annuity at retirement, although lump sum payments & partial lump sum payments are generally available Benefits are also available typically at separation of service Typically, the benefits are paid in a lump sum or partial lump sum with some plans offering monthly annuities as well How are benefits distributed?