Download

1 / 20

210 likes | 367 Views

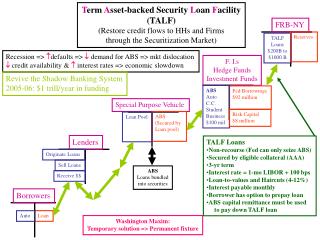

T erm A sset-backed Security L oan F acility (TALF) (Restore credit flows to HHs and Firms through the Securitization Market). FRB-NY. Reserves. TALF Loans $200B to $1000 B. Recession => defaults => demand for ABS => mkt dislocation

E N D

Term Asset-backed Security Loan Facility (TALF) (Restore credit flows to HHs and Firms through the Securitization Market) FRB-NY Reserves TALF Loans $200B to $1000 B Recession => defaults => demand for ABS => mkt dislocation credit availability & interest rates => economic slowdown F. I.s Hedge Funds Investment Funds Revive the Shadow Banking System 2005-06: $1 trill/year in funding ABS Auto C.C. Student Business $100 mil Fed Borrowings $92 million Special Purpose Vehicle Risk Capital $8 million ABS (Secured by Loan pool) Loan Pool Lenders TALF Loans • Non-recourse (Fed can only seize ABS) • Secured by eligible collateral (AAA) • 3-yr term • Interest rate = 1-mo LIBOR + 100 bps • Loan-to-values and Haircuts (4-12%) • Interest payable monthly • Borrower has option to prepay loan • ABS capital remittance must be used to pay down TALF loan Originate Loans Sell Loans ABS Loans bundled into securities Receive $$ Borrowers Loan Auto Washington Maxim: Temporary solution => Permanent fixture

Chapter 10Principles of Bank Management 1. Liquidity Management 2. Asset Management • Manage credit risk - get borrowers with low default risk, paying high interest rates • Buy securities with high return, low risk • Diversify • Manage interest-rate risk 3. Liability Management • Important since 1960s • Banks no longer primarily depend on deposits • When see loan opportunities, borrow or issue CDs to acquire funds • Manage interest-rate risk 4. Capital Adequacy Management

ASSET-LIABLITY MANAGEMENT The Process of planning, directing and controlling the balance sheet flows, levels, mix, and yields & cost of funds. To Achieve Financial Goals: • Capital (Net Worth) • Income (ROA) • Member value • Flexibility • Growth (PCA!) • Loan-to-share ratios To Control Financial Risks: • Credit risk (default) • Liquidity risk • Interest rate risk

Valve/Control: • Interest rates • Loan underwriting standards Loan originations per year Inflow/Production Valve/Control: • Contract term • Interest rates • Economy Equilibrium Condition Inflow = Outflow Loan balance • Amortization / sales • Prepayments • Chargeoffs per year

Asset-Liability Management Interest Rate Risk Interest rate risk is the potential impact of interest rate movements on an institution’s net interest income and capital level. It focuses on the repricing speed of the institution’s assets relative to liabilities Credit Risk Credit risk is the oldest of all financial risks. It is the danger that a borrower will simply fail to meet interest payments or repay a debt Liquidity Risk Liquidity risk is concerned with maintaining an adequate availability of funds for loan demand, deposit outflows, and expense payments in changing interest rate environments

UWCU Balance Sheet Assets Liabilities + NW Cash (7.5%)Deposits (88%) Checking Deposits (15%) Investments (6%) Regular Savings (15%) MMA (29%) Loans (82%) CDs (25%) Consumer (20%) IRAs (4%) Mortgage (46%) Student (16%) Borrowings (2.5%) Building (4.5%)Net Worth (9.5%) 2007-08 Liquidity Crisis Securitization market freeze up 1. Write down security to market value 4. Lenders refuse to rollover loans 5. Sell off assets to pay off loans 3. probability of insolvency 2. net worth YOA - COF = NIM + Fee/Other Income - Operating Expense - PLL = Net Income *Required ROA = Asset Growth Rate x Capital Ratio (dependent variable) (choice variable) (current) 6. asset prices Downward spiral to widespread insolvency

Accounting Review Basic Accounting Equation Assets = Liabilities + Equity (A = L + E) Extended Accounting Equation Assets + Expenses = Liabilities + Equity + Income (A + Exp. = L + E + Inc.) Both sides of these equations must be equal (balance). Double Entry Bookkeeping System: Every debit transaction must have a corresponding credit transaction and vice versa. Debits and credits are the 2 aspects of every transaction. Debits and credits form 2 opposite aspects/sides of every financial transactions. Debit (Dr) is the left side of a ledger account. From latin, debere (to owe). Credit (Cr) is the right side of a ledger account. From latin, credere (to entrust). Assets Liabilities Debits Dr Credits CR Debits Dr Credits Cr

Example1: Person deposits cash into bank checking account Bank Assets Liabilities + E Person Assets Liabilities + E Debits Credits Debits Credits Debits Credits Reserves +100 Deposits +100 Cash -100 Deposits +100 For every transaction, total debits must be equal to the total credits and therefore balance. Value of Debits = Value of Credits. Example 2: Investment Company buys a $500,000 condo. Investment Co. Assets Liabilities + E Bank Assets Liabilities + E Debits Credits Debits Credits Debits Credits Debt +500,000 Cash -500,000 Land +500,000 Loans +500,000 To balance the accounting equation ( A = L + E ) the corresponding liability account is credited.

Journal Form Totals show net effect on accounting equation and double-entry principle where transactions are balanced. Credit transactions are indented in the “Account” column. Extended Accounting Equation A + Exp = L + E + Inc Transaction 1: $500,000 (dr) $500,000 (cr) Transaction 2: -$3,000 (cr) $3,000 (dr) Transaction 3: $1,000 (dr) $1,000 (cr)

Repurchase Agreements (Repo) (Sale and repurchase of securities agreement) Repo = Cash Transaction + Forward Contract (Loan origination) (Loan repayment) (Spot price) (Forward price) (Near leg) (Far leg) (Settlement date) Fed MMMFs Buyer/Lender Bank T-Bill Collateral: T-Bills/Bonds $ Fed T-Bill • Repo: • Fed adds reserves Repo: Seller/Borrower Reverse Repo: Buyer/Lender $ • Reverse Repo: • Fed initially drains reserves • Adds reserves back later • Used to target iff • Repos began in 1917 by Fed to lend to banks • $5 Trillion Repo market today • Secured cash loan • Legal transfer of security to lender • Repurchase price > Original price (gap = interest) • 1-7 day term typically, up to 2 years • Typically over collateralized to mitigate credit risk • Fed describes transaction from the counterparty’s viewpoint, rather than from their own.

Assume Required Reserve Ratio (RRR) = 20% Calculate maximum deposit outflow Balance Sheet Reserve Outflow -20,000 -4,000 -800 -160 -32 -7 Sum = 25,000 Deposit Outflow -20,000 -4,000 -800 -160 -32 -7 Sum = 25,000 Chk Dep = 100,000 RR = 20,000 ER = 20,000 Chk Dep = 80,000 RR = 16,000 ER = 4,000 RR = 15,200 ER = 800 Chk Dep = 76,000 RR = 15,040 ER = 160 Chk Dep = 75,200 RR = 15,008 ER = 32 Chk Dep = 75,040 RR = 15,001 ER = 7 Chk Dep = 75,008 RR = 15,000 ER = 0 Chk Dep = 75,000 Maximum deposit outflow = 20,000 [1 + 0.2 + 0.22 + 0.23 + …..] = ER [1 + x + x2 + x3 + …..], where x = RRR = 0.2 = ER [1/(1-x)] = 20,000 * 1.25 = 25,000

Assume Required Reserve Ratio (r) = 20% Calculate maximum deposit outflow, X Balance Sheet RR = $20,000 ER = $20,000 Chk Dep = $100,000 What we know: R1 = RR1 + ER1 R = V.C. + F.D. DR = DD = X RR = rD R after deposit outflow X: R2 = 40,000 – X RR after deposit outflow X: RR2 = 0.20 * (100,000 – X) ER after deposit outflow X: ER2 = 0 R2 = RR2 + ER2 40,000 – X = 0.20 * (100,000 – X) + 0 200,000 – 5X = 100,000 – X 25,000 = X DR = DRR + DER 25,000 = 5,000 + 20,000

Assume a new checkable deposit, DD, leads to: • Vault cash, VC, increases $2 million (DVC = 2) • Excess reserves, ER, increase $9 million (DER = 9) • Required Reserve Ratio, r = 10% Calculate the increase in Fed Deposits, DFD What we know: RR = rD R = RR + ER R = VC + FD DR = DD RR = rD Balance Sheet R = RR + ER R = VC + FD D DR = DD • R = RR + ER • DR = DRR + DER (convert to changes) • DD = r DD + DER (equation substitution) • DD = 0.10 DD + 9 (r = 0.10 and DER = 9) • DD = 10 • R = VC + FD • DR = DVC + DFD (convert to changes) • DD = DVC + DFD (equation substitution) • = 2 + DFD (DD = 10 and DVC = 2) • 8 = DFD Balance Sheet DR = 10 D RR = 1 D ER = 9 D VC = 2 D FD = 8 DD = 10 Regulatory Allocation Location Allocation

A situation where 1 party has more info than the other party Asymmetric Information 2 types Adverse Selection Moral Hazard potential bad credit risks are the ones who most actively seek out loans the lender runs the risk that the borrower will engage in risky activities that make it less likely that the loan will be paid back Screening process Monitoring process Loan applicants “The business of banking is the business of collecting information” Good C.R. Performing Approve Deny Non-performing Loan signing date Bad C.R. Stopping “bad credit risks” from becoming borrowers Stopping borrowers from becoming “bad credit risks” Loan department Collections department

Income Ratios (Financial Capabilities) 3-Dimensional Mortgage Loan Underwriting Marginal borrower is being denied 65% Total Debt Expense Gross Income 3 Cs of Lending • Collateral • Capacity • Character Inflated Non-verified Income 36% Loan Approval Zone 2005 False Premise: Home prices always rise So default risk is low 35% Housing Expense Gross Income 28% Loan-to-Value Ratios (Physical Security) Loan Approval Zone 2007 80% 100% Inflated Appraisals 670 620 580 Mortgage Crisis: • Lending to high-risk borrowers • large amounts of money • that they could not afford 500 Credit Scores (Credit Characteristics)

Return on Equity Decomposition ROE = Asset Growth Speed Limit (given constant Capital-to-Asset ratio) Return on Equity Leverage Return on Assets R = Return (net income) E = Equity (reserves + undivided earnings) A = Assets GR = Gross Revenues (interest revenue + noninterest revenue) Profit Margin Asset Utilization

Econ 330 Chapter 10 Homework Due Friday, March 7 in Discussion Chapter 10 Questions & Applied Problems 7, 8, 11, 16, 19, 21, 23, 24, 25