Download

1 / 26

290 likes | 483 Views

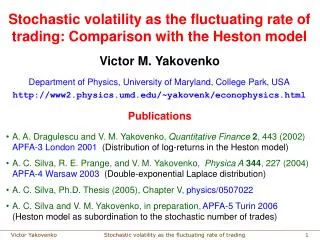

Stochastic volatility as the fluctuating rate of trading: Comparison with the Heston model. Victor M. Yakovenko. Department of Physics, University of Maryland, College Park, USA http://www2.physics.umd.edu/~yakovenk/econophysics.html. Publications.

E N D

Stochastic volatility as the fluctuating rate of trading: Comparison with the Heston model Victor M. Yakovenko Department of Physics, University of Maryland, College Park, USA http://www2.physics.umd.edu/~yakovenk/econophysics.html Publications • A. A. Dragulescu and V. M. Yakovenko, Quantitative Finance2, 443 (2002) • APFA-3 London 2001 (Distribution of log-returns in the Heston model) • A. C. Silva, R. E. Prange, and V. M. Yakovenko, Physica A344, 227 (2004) • APFA-4 Warsaw 2003 (Double-exponential Laplace distribution) • A. C. Silva, Ph.D. Thesis (2005), Chapter V, physics/0507022 • A. C. Silva and V. M. Yakovenko, in preparation, APFA-5 Turin 2006 • (Heston model as subordination to the stochastic number of trades)

Double-exponential (Laplace) distribution of log-returns: An overlooked stylized fact • Detrended log-return is defined as xt = ln(S2/S1)-t, • where S2 and S1are the stock prices at times t2and t1, • t = t2t1 is the time lag (horizon), and is the mean growth rate. • We study the probability distribution Pt(x) of log-returns x after the time lag t. • A simple multiplicative Brownian motion gives the Gaussian distribution • Pt(x) exp(-x2/2vt), which does not agree with the data. • There are two aspects of discrepancy between the data and the Gaussian: • The tails of the distribution (about 1% of probability) follow a power law: • Pt(x) 1/|x|a for large |x| - the Pareto law. • 2. The central part of the distribution (about 99% of probability) follows a double-exponential(Laplace) law: Pt(x) exp(-|x|/ct). The double-exponential law is a ubiquitous, but largely ignored stylized fact, because most studies focus on the tails and make plots in the log-log scale. The Laplace law becomes obvious in the log-linear scale.

German DAX t = 1 day t = 1 hour Poland t = 1 day Indian stocks Double-exponential distribution around the world Poland:D. Makowiec, Physica A344, 36 (2004) Germany:R. Remer and R. Mahnke, Physica A 344, 236 (2004) India:K. Matia, M. Pol, H. Salunkay, and H. E. Stanley, Europhys. Lett. 66, 909 (2004)

Double-exponential distribution around the world t = 4 hours t = 0.5 hour t = 1 hour Japanese Yen Deutsche Mark US bonds J. L. McCauley and G. H. Gunaratne, Physica A 329, 178 (2003) t = 1 day Japanese Nikkei 225 index 1990 – 2002 Taisei Kaizoji, Physica A 343, 662 (2004)

Laplace distribution for short time lags For x>0, we plot and 1-CDF for x<0. Pt(x)rescales when plotted vs. the normalized log-return x/t, where t2 = xt2 Pt(x)exp(-|x|/t): tent-shape, double-exponential, Laplace distribution

Mean-square variation of log-return as a function of time lag 1863: Jules Regnault in “Calcul des Chances et Philosophie de la Bourse”observed t2 = xt2 t for the French stock market. See Murad Taqqu http://math.bu.edu/people/murad/articles.html 134 “Bachelier and his times”.

Time evolution of Pt(x) Dow Jones data for time lags from 1 day to 1 year. Microsoft (MSFT) data for time lags from 5 min to 20 days. The data points show evolution of Pt(x) from the double-exponential shape exp(-|x|) for shortt to the Gaussian shape exp(-x2) for longt. The solid lines show a fit to the Heston model (to be discussed later).

Short-time and long-time scaling Exponential Gaussian

Science284, 87 (1999) Turbulent pipe flow J.E. Guilkey, A.R. Kerstein, P.A. McMurtry, J.C. Klewicki, Phys. Rev. E56, 1753 (1997)

Hydrodynamic turbulence Turbulent jet S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, Y. Dodge, Nature381, 767 (1996) R. Friedrich and J. Peinke, Phys. Rev. Lett.78, 863 (1997) There is amazing similarity between Pt(x) for financial markets and for hydrodynamic turbulence.

Stock price St is not a simple Markov process A Markov process satisfies the Chapman-Kolmogorov equation: This is true for the Gaussian distribution: Normal * Normal = Normal But not true for the Laplace distribution: Exp * Exp Exp It is useful to introduce the characteristic function (the Fourier transform) The Chapman-Kolmogorov equation demands We find that the stock-market data do not satisfy this condition. It is important to describe the whole family of distributionsPt(x) for a range of t, not just for one t, such as 1 day.

Models with stochastic volatility Suppose the variance vt=t2 of a random walk x depends on time. Let us introduce the integrated variance Vt, which acts as the effective time: For stochastic variance, we use subordination (Feller’s book; P.K.Clark 1973): where Kt(V) is the probability density of V for the time lag t. The Fourier and Laplace transforms of Pt(x) and Kt(V) are simply related: Markov processes xt can be written in the subordinated form, but stochastic volatility models can also describe non-Markovian Pt(x)

Heston model with stochastic volatility Steve Heston inReview of Financial Studies6, 327 (1993) proposed amodel where the stochastic variancevt follows the mean-reverting Feller or Cox-Ingersoll-Ross (CIR) process: where Wt is a Wiener process. The model has 3 parameters: - the average variance:t2 = xt2 = t. - relaxation rate of variance, 1/ is relaxation time - volatility of variance, use dimensionless parameter = 2/2 Solving the corresponding Fokker-Planck equation, we obtain where kV is the Laplace variable conjugate to V, vi is the initial variance, and (vi) is the stationary probability distribution of vi.

Notice that is non-Markovian. We set . For long times t » 1: Gaussian distribution It scales as For short times t « 1: Laplace distribution For =1, it also scales Solution of the Heston model Solution of the Heston model qualitatively agrees with the empirical data on time evolution of Pt(x).

Number of trades as stochastic variance Mandelbrot & Taylor (1967) suggested that the integrated variance Vt may be associated with the random number of trades Nt during the time lag t: Vt = Nt . This scenario is related to the continuous-time random walk (CTRW) proposed by Montroll and Weiss (1965). Trades happen at random times ti, so we expect • After a fixed number of trades N (as opposed to a fixed time t), does the probability of returns x follow the Gaussian PN(x) exp(-x2/2N)? • What is the probability density Kt(N) to have N trades during the time t? These questions can be answered using tick-by-tick data. There is some evidence in favor of (1) – Stanley et al., Phys. Rev. E62, R3023 (2000), Ané & Geman, J. Finance55, 2259 (2000). It was disputed by Farmer et al., physics/0510007. However, they focused on the relatively small N and on the power-law tails of PN(x). We study large N and focus on the central part of the distribution.

Three ranges for time horizon • Microscopic (atomic) range – up to ~30 minutes. It is dominated by discrete transitions. • Mesoscopic (diffusive) range – from ~30 minutes to days and weeks. Here continuous stochastic description makes sense. • Macroscopic (hydrodynamic) range – months-years-decades. It is dominated by macroeconomics: expansion vs. recession. The Heston model is applicable only in the mesoscopic range and is compatible with CTRW and subordination formalisms. • Some other recent studies of CTRW in finance: • Enrico Scalas et al. (2000-2006) • Peter Richmond et al. (2002-2004) • Jaume Masoliver et al. (2003-2006) • I.M. Dremin and A.V. Leonidov (2005)

Discrete price changes for short time horizon Discrete price changemN = (SnSn-N)/h, where h=1$/64 is the quantum, vs. continuous returnxN = lnSnlnSn-N (SnSn-N)/Sn = mNh/Sn smeared by Sn. Derivative dPN(m) / dm PN(m) in log-linear scale PN(m) linear scale N=1 (1.5 sec) N=4000 (99 min)

Discrete price changes for short time horizon Blue line: price change mN=S/h Black line: return xN=S/S

Discrete price changes for short time horizon J.D. Farmer et al., Quant. Finance4, 383 (2004) CDFt(x) for t = 5 min For short time horizons (less than ~30 min), price changes and returns are dominated by discrete structure. Continuous (diffusive) models are not applicable at this microscopic scale.

Let us verify for mesoscopic time horizons. We find: Variance of returns and the number of trades

Gaussian distribution for PN(x) Verifying formula PN(x) exp(-x2/2N) The Gaussian distribution works for, at least, 85% of probability (1.5 standard deviation). PN(x) is certainly more Gaussian than Pt(x).

Comparing Kt(N) with the Heston model PDF Kt(N) for the number of trades N during the time t is obtained for Heston model by inverse Laplace transform of

for the Heston model. Verifying Comparing Pt(x) with the Heston model

Conclusions • Probability distribution of log-returns x for mescoscopic time lags t is subordinated to the number of trades N: Pt(x) = dN exp(x2/2N) Kt(N). PN(x) is Gaussian, and Kt(N) is given by the Heston model with stochastic volatility. The stochastic process xt is a continuous-time random walk (CTRW). • The data and the Heston model exhibit the double-exponential (Laplace) distribution Pt(x)exp(|x|2/t) for short time lags and the Gaussian distribution Pt(x)exp(x2/2t2) for long time lags.For all times, t2 = xt2 = t. • The double-exponential distribution, found for many markets, should be treated as a stylized fact, besides the power laws, clustered volatility, etc. • Probability distributions for hydrodynamics turbulence look amazingly similar to those for financial markets – universality?

Brazilian stock market index IBOVESPA R. Vicente, C. M. de Toledo, V. B. P. Leite, and N. Caticha, Physica A361, 272 (2006) Fits to the Heston model