Download

1 / 2

20 likes | 41 Views

Increasing lifetime expectancies and raising dwelling fees imply that a lot of Australians obtain them selves asset prosperous and funds weak because they become old.

E N D

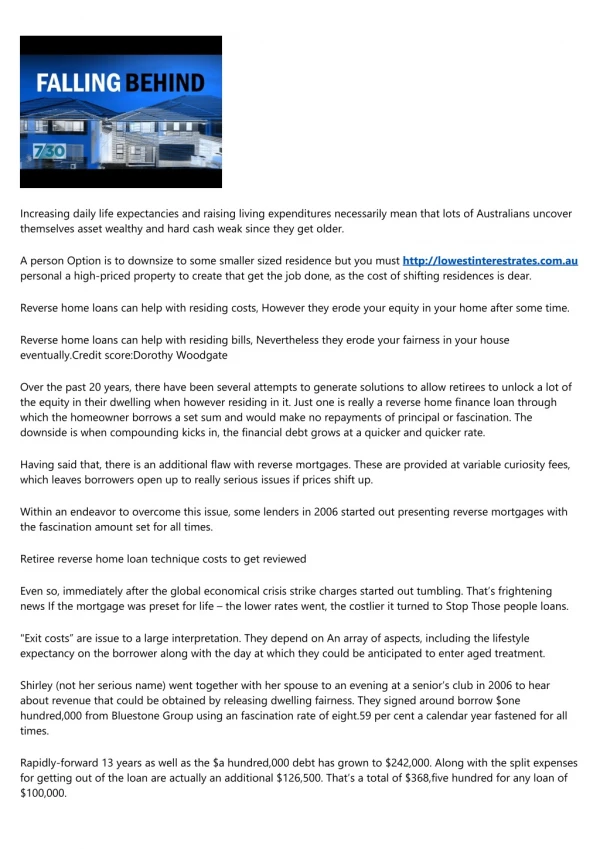

Increasing daily life expectancies and raising living expenditures necessarily mean that lots of Australians uncover themselves asset wealthy and hard cash weak since they get older. A person Option is to downsize to some smaller sized residence but you must http://lowestinterestrates.com.au personal a high-priced property to create that get the job done, as the cost of shifting residences is dear. Reverse home loans can help with residing costs, However they erode your equity in your home after some time. Reverse home loans can help with residing bills, Nevertheless they erode your fairness in your house eventually.Credit score:Dorothy Woodgate Over the past 20 years, there have been several attempts to generate solutions to allow retirees to unlock a lot of the equity in their dwelling when however residing in it. Just one is really a reverse home finance loan through which the homeowner borrows a set sum and would make no repayments of principal or fascination. The downside is when compounding kicks in, the financial debt grows at a quicker and quicker rate. Having said that, there is an additional flaw with reverse mortgages. These are provided at variable curiosity fees, which leaves borrowers open up to really serious issues if prices shift up. Within an endeavor to overcome this issue, some lenders in 2006 started out presenting reverse mortgages with the fascination amount set for all times. Retiree reverse home loan technique costs to get reviewed Even so, immediately after the global economical crisis strike charges started out tumbling. That’s frightening news If the mortgage was preset for life – the lower rates went, the costlier it turned to Stop Those people loans. "Exit costs” are issue to a large interpretation. They depend on An array of aspects, including the lifestyle expectancy on the borrower along with the day at which they could be anticipated to enter aged treatment. Shirley (not her serious name) went together with her spouse to an evening at a senior’s club in 2006 to hear about revenue that could be obtained by releasing dwelling fairness. They signed around borrow $one hundred,000 from Bluestone Group using an fascination rate of eight.59 per cent a calendar year fastened for all times. Rapidly-forward 13 years as well as the $a hundred,000 debt has grown to $242,000. Along with the split expenses for getting out of the loan are actually an additional $126,500. That’s a total of $368,five hundred for any loan of $100,000.

In their letters to Shirley, Bluestone argues that their funds with the mortgage was funded from external resources and, by charging a break rate, they were being simply just passing on what it might Expense them if the personal loan was paid out early. Bottom line Pam also took out a reverse house loan with Bluestone for $37,500 in a charge was 8.39 per cent set for life. Her financial debt has grown to $a hundred and ten,700 and her break cost is much more than $100,000. Exactly what are the options for borrowers like Shirley and Pam? The bottom line is They are really stuck with an increasing reverse house loan credit card debt and an expensive split price. Reverse mortgages are necessary to Use a “no negative fairness” clause, which suggests that the personal debt might not exceed the value on the property if it is sold. For that reason, the worst which could transpire is usually that on the borrower’s Demise, the house could well be taken in full pleasure with the bank loan. The newly-expanded pension loans scheme, administered by Centrelink, is probably going to demonstrate well- liked with retirees Retirement residing Revamped federal government personal loan plan appeals to funds-strapped retirees There's also a clause stating that exit fees might be waived When the borrower goes into aged treatment. Bluestone's documentation on these loans is immaculate: the borrowers were being required to sign a statutory declaration that they experienced sought authorized guidance, and were being informed there could be “significant” costs In the event the bank loan was paid out early. And in which is Bluestone though all this is happening? It's repeatedly refused all offers to comment. In excess of thirteen years immediately after clients entered into life time reverse fastened-price mortgages, Bluestone is legally capable to charge them charges of 8.59 per cent and eight.39 per cent. While the corporate has no lawful duty, the fair issue to accomplish can be to reassess the problem in the light of file reduced prices and provide its shoppers an inexpensive split price.