Download

1 / 75

1.99k likes | 3.8k Views

Basics of Accounting (The Language of Finance) Devotional Introduction Video Discussion of Fundamentals Basic Accounting Problem Grade on Neatness – Bring Back Problem on Wednesday Note: Use a Pencil & Take Good Notes Business & Accounting

E N D

Basics of Accounting (The Language of Finance) Devotional Introduction Video Discussion of Fundamentals Basic Accounting Problem Grade on Neatness – Bring Back Problem on Wednesday Note: Use a Pencil & Take Good Notes

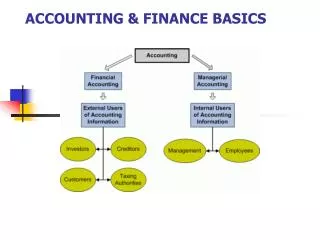

Business & Accounting • Accounting is the universal language of Business and Finance. • More CEO’s from fortune 500 companies have come up through the ranks of accounting than from any other area in business. Currently: 54% • Small businesses and usually fail because of poor accounting understanding. • Marriages usually fail because of poor financial management (80% of divorces are $$$$ related.) • If you want to get ahead in business & marriage determine that you are going to understand accounting basics.

What do Accountants Account For? • Everything of value!

Terms • Assets: Tangible and Non-tangible resources of a business that have future value. Usually sub-classified as follows: • Quick Assets (Liquid Assets) • Cash – Petty Cash – Receivables - Securities • Current Assets (Turn into cash/use annually) • All the above + Inventories, Supplies • Fixed Assets (Depreciated over several yrs.) • Buildings, Equipment, Natural Resources • Land (Fixed, but never depreciated) • Intangible Assets: Patents, Trademarks, Copyrights

What are your Assets? • Bank Account & Money in your pocket • Car • Clothes • Books • Stocks/Bonds/CD’s • Prepaid rent • Computers & Electronic Equip. • Knowledge???? • Abilities????

Accounting Term: Liabilities • Other people’s claims against your assets! • What you owe!! Debts! • Classified as: • Current Liabilities (one year debt) • Credit Card Debt, Accounts Payable • Long Term Liabilities • Car, Mortgage, Note Payable • Unearned revenues • Bonds (usually super long term)

What are your liabilities? • School Loan • Car Loan • Credit Card Balance • J.C. Penny Account • BYU-Idaho Amount Due

Capital or Owners Equity • The portion of your assets that you can legally claim. (Net Assets) What you really own legally. • Assets – (minus) Liabilities = Owners Equity (or Capital) • Example (purchased a building for $500,000 with a 10% down payment ($50,000) • Cost of a building (sales price = Asset amount) $500,000 • Less: What you still owe on the building (Liability) $450,000 • Equals: Your equity in the building (Capital) or your net worth in the building. $50,000 • Formula universally used in all financial and personal financial institutions: • Assets = Liability + Owners Equity (Balance Sheet Equation) • (Resources you have) =(What you owe on them) + (the principle you have paid on them.)

Owners Equity Account Titles • Single Proprietorship: • Capital • Corporation: • Common Stock (what owners paid in) • Preferred Stock (what owners paid in) • Retained Earnings (profits that the business keeps in the business)

What is your net worth??? • What you have minus what you owe. • What format do we use in business and in personal finance to show our net worth? • A Balance Sheet Financial Statement • List of Assets (classified by type in accounts) • Compared or balanced with: • List of Liabilities and Owners Equity (classified by type and in accounts) • Text Book Example Page 660

Example (Simplified) • John Doe’s Business or Personal Records Balance Sheet September 10, 2003 • Assets: • Current: • Cash at Home $100 • Cash Deposits in Bank 500 • Fixed: • Wardrobe 2000 • Equipment 1000 • Car 5000 • Total Assets: $8,600 • Liabilities: • Current: • Credit Card Payable $500 • Long Term: • Note Payable (on Car) $2000 • Total Liabilities $2,500 • Capital, John Doe: 6,100 • Total Liabilities & Owners Equity: $8,600

Other Terms • Temporary Accounts are used in addition to balance sheet accounts to record changes in owners equity each reporting period. • Expenses – Decrease in owners equity during the period by using up an asset or a portion of an asset. (or creating additional liabilities) • Revenue – Increase in owners equity during the period by performing a service or selling an asset. • Drawing or Dividends – Decrease in owners equity due to personal withdrawals by the owner(s).

Income Statement Report • Used to determine the net income or net loss of an individual or business for a defined period of time. • Used for marking progress by comparing months and years • Used by financial institutions for determining the progress and status of a company or individuals financial health. • Used by the IRS for determining taxes

Income Statement – What does it contain? • Matches Expenses with Revenues for a specific period of time. (Only the temporary type of accounts are on the income statement.) No Assets/Liabilities • Income Statement accounts are closed out at the end of the reporting period and started over again the next period….so comparisons can be made. • Personal Income Statement sometimes called a Cash Flow Statement example on page 661

Income Statement – Example Name of Individual or business Income Statement For period of time (Month of Sept. 2003) Revenue: Income from Job $500 Income from Pell Grant 2000 Total Revenue: $2500 Expenses: Clothes Expense $300 Rent Expense 200 Food Expense 50 Tuition Expense 1200 Misc. Expense 250 Total Expenses: $2000 Net Income for September: $ 500

Pop Quiz – Use a Pencil Today • 1. Which financial report is a “snapshot” of the of the financial status of a business or a family…..and is given a specific date? • 2. Which financial report is a “moving picture” of the business/enterprise for a period of time? • 3. What does a balance sheet balance? • 4. What are the two kinds of accounts found on an Income Statement? • 5. On what financial report(s) is the “cash” account found? • 6. What are the three subtitles of a income statement. (name them in the order they are given on the report) • 7. If the bank wanted to know your “Net Worth” what report would they ask for? • 8. Capital in a corporation is entitled ? • 9. Two ways to increase the capital account are? • 10. Two ways to decrease the capital account are?

How do individuals or businesses keep track for all their assets, liabilities, capital, expenses, revenues. Etc.? • The “Accounting Process” or otherwise known as the Accounting Cycle. (also called the “Audit Trail” of business. • Based on universally accepted accounting principles. (Generally accepted accounting principles) • Double Entry Bookkeeping • Accrual Accounting vs. Cash Accounting • Bookkeeping part of accounting.

Accounting Cycle – Start with financial transactions (you will need to know these steps!) • Verbs & Nouns for each step • #1 AnalyzeSource Documents • Check, receipts, invoices, deposit slips, etc. • Decide what accounts they represent • #2 Enter (journalize) data in the journal. • Chronological record of transactions • Book of original entry – checks and balances • Two or more accounts entered at cost • Make a Journal – Required

Accounting Cycle • #3 Post from the journal to the individual ledger accounts. (to keep a running balance of each account) • Ledger divided up into these different accounts: • Assets (100 accounts) • Liabilities (200 accounts) • Capital/Owners Equity (300 accounts) • Revenues (400 accounts) • Cost of Goods Sold (Expense) – (500 accounts) • General Expenses (600 accounts) • Make some ledger accounts - required

Accounting Cycle #4 • Adjust the necessary accounts to bring them up to date. • Requires internal transactions • Requires journal entries & posting as well • Example: Maybe some of your Supplies valued at $500 when you bought them have been used…you need to bring their value up to date and expense what has been used. • Example: Depreciation of Equipment

Accounting Cycle #5 • #5 At the end of the period or at any time (with computers) balance all of the accounts in a trial balance. (Checks and balance step to see if all of your journal entries and posting was correct.) • The trail balance is a list of all of your accounts with balances. • The total of the debit balances must equal the total of the credit balances. • Make a Trial Balance - Required

Accounting Cycle #6 & 7 & 8 • #6 Prepare the Financial Statements • Income Statement • Statement of Changes in Owners Equity • Balance Sheet • Make Financial Statements - Required • #7 Close out all the temporary accounts to zero, so that you can start a new period/cycle. • Requires journal entries and postin gs • #8. Analyze your financial findings.

The Balance Sheet and Debits and Credits • Balance Sheet Equation • A = L + OE • Use of another checks & balance method • Debits and Credits are terms used to increase or decrease various accounts and show balances. • All Accounts have either a debit or credit balance. • Assets/Expenses/Withdrawals have debit balances • Increased by debiting and decreased by crediting • Liabilities, Capital, and Revenues have credit balances. • Increased by crediting, and decreased by debiting

Assets = Liabilities + O.E. • Cash A/P Capital • Debit Credit Debit Credit Debit Credit • + - - + + - • 100 50 100 • 75 • -Drawing -Expense +Revenue • Dr Cr Dr Cr Dr Cr • + - + - - + • 50 75 • Each Transaction in finance has a debit and a credit. The debit amount must always equal the credit amount. (Checks & Balances) • Example: Invested 100 Cash in my business. • Example: Paid $50 for Advertising Expense. • Example: Earned $75 for performing services • At the end of the day: (Assets = 125) = (Liabilities = 0) + (OE = 125) and debits = 225 and credits = 225 (Double balance, double witness)

Quiz Preview – Review with Partner • 1-2. Give the accounting equation and define each element in the equation. • _____________________________ = _________________________ + ______________________ • Define:_________________________ _______________________ ______________________ • 3. Accounting is called the _____________________________________ of business. • 4-7. Name these two statements (The Trial Balance is not a Statement) used in accounting which are used by managers to make financial decisions (the ones completed in your accounting project) What type of accounts are on each statement? • First Statement Prepared_____________________________________________________________ • Types of accounts found on this statement._______________________________________________ • Last Statement Prepared___________________________________________________________ • Two accounts found on this statement?__________________________________________________ • 8-12. Give the verbs and nouns of the Six first steps in the accounting cycle: (fill in the blanks) • VerbNoun • 1.) _________________________________ _________________________________ • 2.) _________________________________ _________________________________ • 3.) _________________________________ _________________________________ • 4.) ____Adjust _______________________ ____Internal Accounts_______________ • 5.) _________________________________ _________________________________ • 6.) _________________________________ _________________________________

Accounting Quiz - Continued • 13. If the accountant wanted to know the balance of cash currently owned by the business he would go to the: • ______________________________________________________ • 14. If the accountant wanted to know what type of transaction happened on a specific day he would go to the: • ______________________________________________________ • 15. The report that determines the net profit or loss of a business for a specific period of time is called the: • ______________________________________________________ • Credit Debit Matching • 16. ______Increase to Assets when recorded in the journal are: A. Debit(s) • 17._______Increase to Liabilities when recorded in the journal are: B. Credit(s) • 18. _______Increase to Expenses when recorded in the journal are: C. Can be either Dr or Cr. • 19._______Asset accounts carry what kind of balances: D. Always both Dr & Cr • 20._______Revenue accounts carry what kind of balance:

Quiz – Last Page • 21. What does ROI stand for in finance/accounting? _____________ __________ ______________________ • 22. What is the “Separate Entity Principle”_______________________________________________________ • 23. Net Income is added to what account in the “Statement of Owners Equity”__________________________ • 24. In what two ways can you decrease the Capital Account? _________________ _____________________ • On the Back • 25-26. Draw/format the ledger account for cash (only) with a beginning balance of $2000 and post the following two transactions in the account that occurred today. (You do not need to make any journal entries.) • A. Received $5000 into the business from a personal investment from the owner of the business. • B. Paid out $1000 to employees in wages. • 27-30. Format the April Income Statement for “Ace” company that has these accounts: (You may not need to use all of the accounts): Cash: $100, A/P $50, Service Revenue: $500, Sales Revenue: $1000, Cost of Goods Sold Expense: $400, Advertising Expense: $100, Misc. Expense: $300, Wages Expense $200, A/R: $300.

The best way to learn: • Complete a simplified practice set that covers the entire accounting cycle. • Work in partnership with another student and the teacher. Use a pencil! • Final product: Do your own set of personalized financial statements. • Problem due on Friday 1/16/04. Quiz over the accounting language and Accounting Cycle on Friday.

Separate Entity Principle (Keep your business records separate from you personal records) • Lets start a home cleaning business. • First Transaction on 1/1 • Pull $1,000 savings out of your personal account and put it into your business account. • Assets = Liabilities + Owners Equity Cash = 0 Capital 1,000 1,000

Record in Daily Journal • Date Entries PR DR CR Pg1 • 1/1 Cash 101 $1000 • Capital 301 $1000 • Started business with personal investment.

Posting to the Ledger Accounts: • Post $1000 as a debit to the cash account • Post $1000 as a credit to the capital account • Cash 101 • Date Explanation PR DR CR BAL • 1/1 J1 $1000 $1000 • Capital 301 • 1/1 J1 $1000 $1000

2nd Transaction • Acquire a Loan of $5,000 to buy equipment and materials to start a cleaning business. • Assets = Liabilities + OE • Cash Loan Payable Capital $6,000 $5,000 $1,000 ($1,000 + $5,000) $6000 = $6000

Journal Entry • Date Explanation PR DR CR • 1/2 Cash 101 $5000 • Loan Payable 201 $5000 • Received cash on credit.

Posting • Cash (101) • Date Explanation PR DR CR BAL • 1/1 J1 1000 1000 • 1/2 J1 5000 6000 • Loan Payable (201) • Date Explanation PR DR CR BAL • 1/2 J1 5000 5000

3rd Transaction – Jan 3rd • Purchased Equipment (Vacuum, Carpet Cleaner, Floor Polisher etc.) Cost: $3,000 • Assets = Liabilities + OE • Cash Loan Payable + Capital • Equipment • Accounting Equation Stays in Balance: • Cash = $3000 = $5000 + $1000 • Equipment = $3000

Journal Entry • Date PR Dr Cr___ • 1/3 Equipment 120 $3000 • Cash 101 $3000 • Used cash to purchase equipment

Posting to the Ledger Accounts • Cash 101 • Date PR Dr Cr Bal___ • 1/1 J1 1000 1000 • 1/2 J1 5000 6000 • 1/3 J1 3000 3000 • Equipment 120 • Date PR Dr Cr Bal__ • 1/3 J1 3000 3000

Pop Quiz – Are you ready? • 1. Give the accounting equation and define each element. • 2. What is the separate-entity principle? • 3. Give the first three steps in the accounting cycle using verbs and nouns. • 4. When a family or a business does something to change their financial picture or position it is called what? • 5. What are the two financial statements discussed in class and what type of accounts are on each. • 6. When we increase an asset what do we say in terms of debits and credits? How about a liability? • 7. What are the temporary accounts used in financial management? • 8. What kind of a balance do the following accounts carry:? • Assets Expenses Revenues Liabilities Capital Drawing • 9. Format a balance sheet and income statement. • 10. What do the following terms mean? ROI, Liquidity, Profit, Goodwill

4th Transaction – 1/4 • Paid $200 for full page ad in the Newspaper.

Journal Entry • Date PR Dr Cr • 1/3 Advertising Expense 601 200 • Cash 101 200 • Purchased ad for business

Postings • Advertising Expense 601 • Date PR Dr Cr Bal______ 1/4 J2 200 200 • Cash 101 • Date PR Dr Cr Bal___ • 1/1 J1 1000 1000 • 1/2 J1 5000 6000 • 1/3 J1 3000 3000 • 1/4 J2 200 2800

5th Transaction 1/5 • Had my first cleaning job for $400. Was paid $100 down with the rest due at the end of the month.

Journal Entry Date PR Dr Cr 1/5 Cash 101 100 A/R 110 300 Revenue 401 400 Performed services and received down payment. Bal due: 1/31

Postings • Cash 101 • Date PR Dr Cr Bal___ • 1/1 J1 1000 1000 • 1/2 J1 5000 6000 • 1/3 J1 3000 3000 • 1/4 J2 200 2800 • 1/5 J2 100 2900 • Accounts Receivable 110 • Date PR Dr Cr Bal___ • 1/5 J2 300 300 • Service Revenue 401 • Date PR Dr Cr Bal___ • 1/5 J2 400 400

Transaction #6 #7#8#9&10 • Hired my little brother to help me and paid him $100 in wages • Worked all day on second cleaning job and was paid $500 • Had to spend $300 on cleaning supplies to be used during the next two months. • Took $200 out of my business to take my wife on a mini moon. • Allocated 50% use of my truck to my business. Book price of truck = $6000

Journal Entries • Date PR Debit Credit • 1/6 Wages Expense 620 100 • Cash 101 100 • 1/7 Cash 101 500 • Service Revenue 401 500 • 1/8 Cleaning Supplies 130 300 • Cash 101 300 • 1/9 Drawing 320 200 • Cash 101 200 • 1/10 Truck 150 3000 • Capital 301 3000

Postings • Wages Expense 620 • Date PR Dr Cr Bal • 1/6 J2 100 100 • Cash 101 • Date PR Dr Cr Bal___ • 1/1 J1 1000 1000 • 1/2 J1 5000 6000 • 1/3 J1 3000 3000 • 1/4 J2 200 2800 • 1/5 J2 100 2900 • 1/6 J2 100 2800 • 1/7 J2 500 3300 • 1/8 J2 300 3000 • 1/9 J2 200 2800

Posting Cont. • Service Revenue 401 • Date PR Dr Cr Bal___ • 1/5 J2 400 400 • 1/7 J2 500 900 • Cleaning Supplies 130 • Date PR Dr Cr Bal_____ • 1/8 J2 300 300 • Anderson, Drawing 320 • Date PR Dr Cr Bal______ 1/9 J2 200 200

Posting Cont. • Truck 150 • Date PR Dr Cr Bal_____ • 1/10 J2 3000 3000 • Capital 301 • 1/1 J1 $1000 $1000 • 1/10 J2 $3000 $4000

Adjustments at the end of the month – Internal Transactions – Step #4 in the Accounting Cycle • Adjusted the cleaning supplies to show that 33% had been used up. • Adjusted the truck account to show that one month had been used up. • Truck was expected to last for two more years • $3000/24months = $125 use per month