Download

1 / 37

380 likes | 827 Views

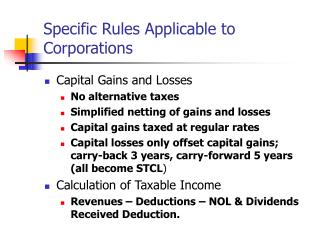

Specific Rules Applicable to Corporations. Capital Gains and Losses No alternative taxes Simplified netting of gains and losses Capital gains taxed at regular rates Capital losses only offset capital gains; carry-back 3 years, carry-forward 5 years (all become STCL )

E N D

Specific Rules Applicable to Corporations • Capital Gains and Losses • No alternative taxes • Simplified netting of gains and losses • Capital gains taxed at regular rates • Capital losses only offset capital gains; carry-back 3 years, carry-forward 5 years (all become STCL) • Calculation of Taxable Income • Revenues – Deductions – NOL & Dividends Received Deduction.

Specific Rules Applicable to Corporations • Net Operating Losses • Calculation is usually simple: Revenues – Deductions • Dividends Received Deduction • Based on % ownership • Less than 20% ownership 70% deduction • 20% - 79.99% 80 • 80+ 100 • Limited to 80/70% taxable income unless corporation has orgenerates an NOL. • Generally carry back 2 years and carry forward 20 years with an election to carry forward.

Specific Rules Applicable to Corporations • Charitable Contributions • Limited to 10% of taxable income before contributions and special deductions (dividends received deduction, NOL & Capital Loss Carry-back) • Carry-forward unused amounts for 5 years. • Accrual basis corporations must pay authorized contributions within 2 ½ months of the succeeding tax year.

Computation of Tax • Graduated Rates • For most mid sized C corporations the rate is 34 % • Corporations have an alternative minimum tax. • Structure is similar to individuals except for: • ACE adjustment • No itemized deductions • Exemption is $ 40,000 • AMT rate is 20%

Computation of Tax--Continued • Penalty Taxes • Accumulated Earnings Tax (Rare) • Personal Holding Company Tax • Relates to closely held corporations with passive (investment) income • Rate coincides with the highest individual rate.

Controlled Groups • Two types: • Brother-sister • 5 or fewer individuals, estates or trusts own at least 80% of the voting power or value of all classes of stock of each corporation. • Shareholders commonly own more than 50% of the total voting power or value of all classes of common stock, (identical interest) • Parent-subsidiary (more common) • A common parent owns at least 80% of the stock of at least one subsidiary corporation. • At least 80% of the stock of each other member is owned by the other members of the controlled group., • Review handout on controlled groups

Controlled Groups--Continued • Combined Controlled Groups • Common parent owns at least 80% of at least one subsidiary corporation and • The common parent corporation is a member of a group of corporations that constitute a brother-sister group. • Computation of Tax • A controlled group must apportion the lower tax rates among group members as if only one corporation existed. • Consolidated Returns • Must be members of an affiliated group (parent/sub) relationship. Certain corporations are not permitted to members of the group.

Transfers of Property to a Controlled Corporation § 351 • No gain or loss if certain conditions are met: • Property (other than services) is transferred to the corporation in exchange for stock in the transferee corporation. • Immediately after the exchange the transferor shareholders in aggregate control the transferee corporation by owning at least 80% of the stock. • Gain is recognized for specific transactions: • If the transferor receives money or property (and also to the corporation if it transfers appreciated property) • Character of the gain is determined by the character of the assets transferred to the transferor.

Transfers of Property to a Controlled Corporation--Continued • Basis of stock received by the transferor: • Basis of Property transferred to corporation + Gain recognized – money received (including liabilities transferred to corporation) – FMV of property received = Basis of stock received. • Basis of Property received by the transferee corporation: • Basis of Property = Adjusted basis of property to transferor + Gain recognized by transferor

Transfer of Property to a Controlled Corporation • Treatment of Liabilities • Treatment of Gain—Under § 357(a) no gain or loss is recognized by the transferee corporation. • Exceptions for: • Tax Avoidance Arrangements § 357(b) • Total liabilities transferred are in excess of the basis of the total assets transferred § 357 (c)

Earnings & Profits § 312 • Similar in many ways to accrual basis retained earnings, not defined in the Code. • Current versus Accumulated E & P § 316 • Distributions to shareholder’s come first from current E & P • Accumulated E & P represent the total of all prior years’ undistributed current E & P as of the first day of the tax year. Distributions are deemed to be made out of AEP only after current E & P is exhausted. • If total E & P is 0 or negative, distributions reduce the shareholder’s stock basis. • Distributions in excess of the shareholder’s stock basis are capital gains.

Distributions of Property • Tax Consequences to the Shareholder • The amount distributed equals the FMV of the property (reduced by any associated liabilities) • The amount distributed is treated as a taxable dividend if the corporation has sufficient E & P • The basis of the distributed property equal its FMV. • Tax Consequences to Distributing Corporation • No gain or loss, except gain on distributions of appreciated property.

Stock Redemptions • Two possible tax consequences: • Redemption treated as a taxable dividend to the extent of E & P • The redemption is treated as an exchange of stock (Capital gain treatment) • Determining whether a redemption is a dividend or capital gain: • § 302(b)(2) redemption is substantially disproportionate with respect to the shareholder’s interest. CG • § 302(b)(3) complete termination of a shareholder’s interest. CG • § 302(b)(4) partial liquidation—CG for non-corporate shareholder • Review examples 25 & 26 on page 20-23

Corporate Distributions in Complete Liquidation § 336 • Tax Consequences to the Liquidating Corporation • Liquidating corporation recognizes gains and losses on distributions of property and on sales of assets. • Liquidating subsidiary recognizes neither gain or loss when it distributes property to its parent corporation. • Liquidating corporation recognizes no loss when it distributes property to a related person or if property was acquired within the last five years in a § 351 transaction. • Tax attributes disappear • Tax Consequences to Shareholder • Shareholder generally recognizes capital gain or loss equal to the difference between the money and/or property received and the adjusted basis of the shareholder’s stock.

§§ 332/337: Liquidation of a Subsidiary Corporation • Gain or Loss Considerations (Mandatory) • Neither the parent nor the subsidiary recognize gain or loss if the parent owns an 80+% subsidiary. • Subsidiary must do either of the following: • Distribute all of its property to the parent corporation in complete liquidation within a single tax year. • Make a series of liquidating distributions resulting in a complete liquidation over a three year period that commences with the close of the tax year in which the first liquidating distribution is made. • Subsidiary recognizes gain on distributions to minority shareholders.

§§ 332/337: Liquidation of a Subsidiary Corporation--Continued • Basis Considerations § 334 (b)(1) • The basis of the subsidiary’s assets carry over to the parent corporation and the parent corporation’s interest in the subsidiary stock disappears. • Subsidiary tax attributes carry over to parent.

Schedule M-1, Reconciliation of Book to Taxable Income • Begin with Net Income per Books • Additions • Federal income tax expense • Excess of capital losses over capital gains • Income subject to tax not recorded on books • Expenses recorded on books, not recorded on return • Subtractions • Income recorded on books and not on return • Expenses deducted on return and not on books • Equals Taxable Income before Special Deductions, Form 1120 (Page 1, Line 28) • Review Example 14 on Page 20-15.

S Corporation Qualification Requirements • Entity • Must be a domestic corporation • Must not be an ineligible corporation (insurance co., financial institution, possessions corp.) • Must not have more than 75 shareholders • Must have only individuals, estate, certain types of trust & tax exempts as shareholders • Must not have a non-resident alien as a shareholder • Must issue only one class of stock. • If the corporation does not meet any of these requirements, the election (if made) terminates.

S Corporation Election Requirements • Requirements • All shareholders must consent • File Form 2553 • For current year, during preceding year or within 2 mos. 15 days during the current year. • Elections made after the current year deadline are consider made for the following year. • IRS has latitude in correcting election deficiencies. • Termination Conditions • Generally for the entire year if the corporation files a statement within 2 mos. 15 days., otherwise next year. • May specify termination date. • Cannot elect S status again for five years.

S Corporation Operations • Similar to Partnerships • Ordinary Income (page 1, Form 1120S & Schedule K). The residual amount. • Separately stated items • Schedule K-1 for each shareholder • However, the allocations are based on shares owned on each day of the year. • Other characteristics • No dividends received or NOL deduction • Special taxes on S corporations that were previously C corporations • Built in gains • Excess net passive income • Lifo conversions

Basis Adjustment to S Corporation Stock § 1367(a) • Increased by: • Stock purchases • Capital contributions • Non-separately computed income • Separately stated income items • Depletion in excess of basis • Decreased by

Basis Adjustments to S Corporation Stock § 1367(a) • Increased by: • Stock purchases • Capital contributions • Non-separately computed income • Separately stated income items • Depletion in excess of basis • Decreased by distributions not reported as income by shareholders (tax free distributions and return of capital) • Then decreased (but not below zero) by: • Non-deductible expenses • Non-separately computed loss • Separately stated loss and deduction items

Basis Adjustments for S Corporations--Continued • Excess Losses • Once the stock basis is zero, any additional basis reductions from losses or deductions but not distributions decrease (but not below zero) the shareholder’s basis in loans made to the S corporation. Any excess of losses or deductions is suspended until there is subsequent basis. • Restoration of Basis • If a shareholder’s basis in the loan is reduced by a loss deduction, subsequent increases restore first the loan, and then the shareholder’s stock basis. • Passive Activity Losses • S corporation shareholders are subject to the PAL rules

Other S Corporation Considerations • Distributions of Cash and Property • Assuming the S corporation was not previously a C with AEP, money and property distributions are treated as a return of capital to the shareholder (tax free, unless they exceed the shareholder’s basis, then CG) • Tax Year Restrictions • Generally S corporations use a calendar year.

S Corporations—Treatment of Fringe Benefits • S corporation shareholders who own more than 2% of the outstanding stock are not eligible for tax-free corporate employee fringe benefits. These include: • Group term insurance • Accident and health insurance premiums • Cafeteria plan benefits • Employer provided fringe benefits • Meals and Lodging • Not all fringe benefits are subject to this special treatment. These include • Stock Options and Non-qualified deferred comp. • Qualified fringes, dependent care assistance, no-additional cost fringes • Educational Assistance Programs

§ 721 Formation of a Partnership • No gain or loss upon either transfer of property in exchange for a partnership interest or subsequent transfers of property by the partners in exchange for a pro rata increase in their partnership interests. • Principal Exceptions: • Sales by partner to partnership or partnership to partner • Contributions to the partnership of services • Liabilities transferred exceed partner’s basis

§ 722 Basis of a Partnership Interest • Basis = sum of money contributed + adjusted basis of other property transferred to the partnership. • If a contributing partner renders services to the partnership in exchange for a partnership interest , the contributing partner’s basis = income recognized (FMV) • § 752 Basis Adjustments: Includes partner’s ratable share of partnership liabilities • Increase in liabilities increases the basis. • Decrease in liabilities decreases the basis. • § 731 Basis cannot be negative. Negative Basis Gain 0 basis

Other Partnership Formation/Contribution Issues • Holding Period for Partnership Interest • Cash and Ordinary Asset Contributions Date interest is acquired • Capital and § 1231 Asset Contributions generally includes the holding period of the property • Basis of Partnership Assets • § 723 provides for carry-over basis • Holding period includes the period the property was held by the contributing partner. • No basis adjustment for gains related to contributions of negative basis assets.

Other Partnership Formation/Contribution Issues • Financial Accounting Considerations • GAAP basis of accounting does not apply carryover basis and non-recognition rule. • GAAP approximates approach required by special allocation rules. • Organization and Syndication Fees • Organization expenses include legal and accounting fees incident to organizing the partnership. Amortize over 60 months • Syndication fees are expenses incurred to promote and market partnership interests. No amortization.

Partnership Operations • Partnership Schedule K • Partnership ordinary income/loss, Page 1, Line 22 form 1065 (the residual amount) • Separately Stated Items • Rental income, capital gains/losses, § 1231 gains/losses, contributions, § 179 deduction, tax exempt interest. • Schedule K-1 shows individual partner’s share. schedule K = (schedule K-1) • Individual partner’s share of ordinary income/lossis determined by the partnership agreement.

Partnership Operations--Allocations • Special Allocations § 704 • Partners have latitude to decide how income, deductions, losses and credits are to be allocated among the partners. • Special allocations must show “substantial economic effect” (i.e. similar to GAAP accounting). • Particularly important in allocation of depreciation deductions and gain/loss for contributed property. • Allocation of Partnership Income, Deductions, Losses and Credits • If any partner’s interest in the partnership changes during the year, all partners must determine their distributive share of income, deductions, losses & credits.

Calculation of Partner’sBasis § 705 • Initial basis • + Partner’s subsequent contributions • + Debt increase • Taxable income items • Exempt income items • Excess of depletion over adjusted basis • - Partner’s distributions and withdrawals • - Debt decrease • Non-deductible items charged to the capital account • Special depletion deduction for oil and gas wells • Loss items • The basis of a partner’s interest can never be negative.

Limitations on Losses and Restoration of Basis • § 704 (d) limits the deductibility of losses to the partner’s adjusted basis in his or her partnership interest as determined at the end of the partnership tax year. All positive and negative adjustments are made before the limitation is considered. • Any unused losses and deductions carry over indefinitely and are allowed in subsequent years when the partner again has a positive basis. • Passive activity losses are determined at the partnership level buy applied at the partner level.

Transactions between a Partner and a Partnership • § 707(b) disallows losses and recognizes ordinary income in certain situations: • Losses are disallowed: • On sales or exchanges between a partner and the partnership if the partner owns more than a 50% interest in the partnership. Review example 47. • On sales or exchanges between two partnerships in which the same partners own more than a 50% interest. • Gains are treated as ordinary income if the partner owns more than a 50% interest in the partnership and if the exchanged asset is not a capital asset in the transferee’s hands. Review Example 48

Guaranteed Payments and Partnership Distributions • Guaranteed Payments • Partnership deducts fixed payments for salary and interest to arrive at ordinary income. • Partner includes such payments in gross income in the year received. Guaranteed payments are subject to SE tax. Review example 40 on page 20-34 • Partnership Distributions • Non Liquidating Distributions • Generally no gain or loss to partner of partnership. • Partner recognizes gain if the amount of money received exceeds the partner’s basis. • Property is assigned basis after considering the cash distribution.

Sale of a Partnership Interest • Liquidating Distributions • Generally results in capital gain or loss. • § 741 Gain or Loss = Amount Realized (including share of liabilities) less Adjusted Basis in Partnership (including liabilities) • § 751 Ordinary Income Treatment for “Hot Assets” • Ordinary income rather than capital gain treatment may result if a partnership has unrealized receivables or inventory items when a partnership interest is sold. • Unrealized receivables = 0 basis A/R, §§ 1245, 1250 recapture • Inventory = Inventory + Other ordinary assets

Partnerships—Other Issues • Optional Basis Adjustments § 754 • Generally occurs when a partnership interest is sold or terminated. • Results because the sale price or distribution amount is greater than the partnership basis. • If elected, the partnership adjusts the tax basis in its assets to reflect the difference • Tax Year Restrictions—generally a calendar year. • Cash method of accounting is generally available.