Download

1 / 36

370 likes | 847 Views

Chapter 17 Financial Management and Institutions. Learning Goals. Identify the likely sources of short-term and long-term funds for business operations. Describe the financial system and major financial institutions. Explain the Federal Reserve System and its tools.

E N D

Chapter 17 Financial Management and Institutions Learning Goals Identify the likely sources of short-term and long-term funds for business operations. Describe the financial system and major financial institutions. Explain the Federal Reserve System and its tools. Describe the global financial system. 6 Identify the functions performed by a firm’s financial managers. Describe the characteristics and functions of money. Identify the various measures of the money supply. Explain how a firm uses funds. Compare the two major sources of funds for a business. 1 7 2 8 3 9 4 5

Finance Business function of planning, obtaining, and managing a company’s funds in order to accomplish its objectives effectively and efficiently. • THE ROLE OF THE FINANCIAL MANAGER • Financial manager Executive who develops and implements the firm’s financial plan and determines the most appropriate sources and uses of funds. • • Chief financial officer Head of an organization’s finance operation. • • Reports directly to CEO or COO. • • Often a member of the board of directors.

• Three executives typically report to the CFO: • • Vice president for financial management or planning Responsible for preparing financial forecasts and analyzing major investment decisions. • • Treasurer Responsible for all of the company’s financing activities, including cash management, tax planning and preparation, and shareholder relations. • • Controller Chief accounting manager; keeps the company’s books, prepares financial statements, and conducts internal audits. • • Often balance risk with expected financial returns: Reward Gain or loss from an investment over a specified period of time Risk Uncertainty of gain or loss

Risk-return trade-off Optimal balance between the expected payoff from an investment and the investment’s risk. Reward Gain or loss from an investment over a specified period of time Risk Uncertainty of gain or loss

The risk reward tradeoff did not work very well for this couple.

The Financial Plan • Financial plan Document that specifies the funds a firm will need for a period of time, the timing of inflows and outflows, and the most appropriate sources and uses of funds. • • Built based on the answers to three questions: • • What funds will the firm require during the appropriate period of operations? • • How will it obtain the necessary funds? • • When will it need more funds? • • Also involves financial control, the process of checking actual revenues, costs, and expenses and comparing them against forecasts.

CHARACTERISTICS AND FUNCTIONS OF MONEY • Characteristics of Money • Money Anything generally accepted as payment for goods and services. • • To be efficient, money must have certain characteristics: • Divisibility • • Allows for easy exchange of a wide variety of products. • Portability • • Light weight of modern paper currency facilitates the exchange process.

Durability • • U.S. dollar bills survive an average of twelve to eighteen months. • • Coins can last 30 or more years. • Difficulty in Counterfeiting • • Counterfeit money undermines a nation’s monetary system and economy by ruining the value of legitimate money. • Stability • • Fluctuating values make people reluctant to use a form of currency.

THE MONEY SUPPLY • • M1 Total value of coins, currency, traveler’s checks, bank checking account balances, and the balances in other demand deposit accounts. • • M2 Financial assets that are almost as liquid as cash but do not serve directly as a medium of exchange. • • Examples: various savings accounts, certificates of deposit, and money market mutual funds.

• Use of credit cards growing rapidly. • • Amount of outstanding credit card debt has risen by more than 400 percent in the last 20 years. • • Percentage of college students with at least one credit card now exceeds 50 percent. • • Companies issue credit cards to both individuals and businesses. • • Branded credit cards Organization partners with bank to issue branded credit cards and receives a payment from the bank based on how much the card is used. • • Emergence of prepaid shopping cards. • • Convenient and easy to use, but a very expensive source of business or consumer credit • • Fraud is also a concern.

WHY ORGANIZATIONS NEED FUNDS • • Run day-to-day operations. • • Compensate employees and hire new ones. • • Pay for inventory. • • Make interest payments on loans. • • Pay dividends to shareholders. • • Purchase property, facilities, and equipment. • • Use financial planning process to determine how to address shortfalls and surpluses.

Generating Funds from Excess Cash • • Most excess cash balances are invested in marketable securities. • • Close to cash because they are easy to convert into cash. • • Most popular marketable securities: • • U.S. Treasury bills—short-term securities issued by the U.S. Treasury and backed by the full faith and credit of the U.S. government. • • Commercial paper—securities sold by corporations maturing anywhere from 1 to 270 days from the date of issue. • • Repurchase agreements—an arrangement in which one party sells a package of U.S. government securities to another party, agreeing to buy back the securities at a higher price on a later date. • • Certificates of deposit—a time deposit at a financial institution, such as a commercial bank, savings bank, or credit union.

SOURCES OF FUNDS • Debt capital Funds obtained through borrowing. • Equity capital Funds provided by the firm’s owners when they reinvest earnings, make additional contributions, or issue stock to investors. • • Even established firms may not generate sufficient funds to cover all of the costs of expansion or a significant equipment upgrade.

Short-Term Sources of Funds • • Repaid within one year. • • Used to meet short-term needs, such as building inventory for holiday shopping season. • • Three major sources:1 Trade credit extended by suppliers when a firm receives goods or services, agreeing to pay for them at a later date. • 2 Short-term loans from commercial banks and other sources. • • Unsecured, firm does not pledge any assets as collateral. • • Secured, specific assets pledged as collateral. • 3 Commercial paper, which has interest rates typically 1 or 2 percent lower than short-term bank loans • • Only large firms with considerable financial strength and stability can sell commercial paper.

Long-Term Sources of Funds • • Repaid over many years. • • Used for major investments. • • Three common sources: • 1 Long-term loans. • 2 Bond Certificate of indebtedness sold to raise long-term funds for a corporation or government agency. • 3 Equity financing from selling stock in the firm or reinvesting company profits.

Public Sale of Stocks and Bonds • • Major source of funds for corporations. • • Provide cash inflows for the issuing firm in exchange for either a share in its ownership (for a stock purchaser) or a specified rate of interest and repayment (for a bond purchaser). • Private Placements • • Stock or bond issues sold only to a small group of large investors such as pension funds and insurance companies. • • One-third of all new corporate debt issues are privately placed. • Venture Capitalists • • Invest funds in promising firms in exchange for part ownership of the business. • Leverage • Leverage Technique of increasing the rate of return on an investment by financing it with borrowed funds.

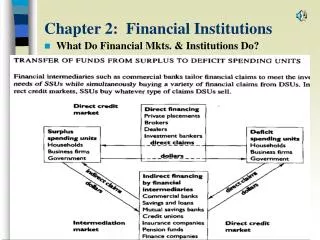

FINANCIAL SYSTEMS AND FINANCIAL INSTITUTIONS • Financial system System by which funds are transferred from savers to users.

• In U.S., households are generally net savers while businesses and governments are net users. • • Funds can be transferred through the financial markets or through financial institutions. • • Financial institutions greatly increase the efficiency and effectiveness of the transfer of funds between savers and users. • • Because of financial institutions, savers earn more, and users pay less. • Depository institutions Financial institutions that accept deposits that can be converted into cash on demand. • • Examples: commercial banks, savings banks, and credit unions. • • Nondepository institutions include life insurance companies, pension funds, and the various government- sponsored financial institutions such as Fannie Mae and Freddie Mac.

Commercial Banks • • In U.S., approximately 7,600 commercial banks. • • Have total assets of approximately $8.5 trillion. • • Offer a wide range of checking and savings deposit accounts, consumer loans, credit cards, home mortgage loans, business loans, and trust services. • • Number of banks has declined almost in half in last 25 years, but the typical banks is twice as large as 10 years ago. • • Growing countertrend of small community banks, which typically serve a single city or county and have millions, rather than billions, of dollars in assets and deposits. • How Banks Operate • • Raise funds by offering checking and savings deposits to customers. • • Then pool these funds and offer consumer and business loans.

Electronic Banking • • Electronic funds transfer systems (EFTSs) Computerized systems for conducting financial transactions over electronic links. • • Examples: Direct deposit of paychecks, ATMs. • • Check cards that allow consumers to make purchases directly from their checking or savings account. • Online Banking • • More than one-third of American households use some form of online banking. • • Five million Bank of America customers annually pay $80 billion worth of bills online. • • Allows customers to make transactions at any hour on any day.

Bank Regulation • • Among the nation’s most heavily regulated businesses. • Who Regulates Banks? • • Most are state chartered. • • Federally chartered banks control more than half of all banking assets. • • Regulated by the Federal Deposit Insurance Corporation and the Comptroller of Currency. • • State banks that are federally insured are subject to FDIC regulation. • Federal Deposit Insurance • • Insures deposits of up to $100,000 per depositor. • • Enacted in 1933 to restore public confidence during the Great Depression. • • Shifts risk of bank failure from depositor to FDIC.

Recent Changes in Banking Laws • • Congress revised Depression-era laws to allow banks to enter securities and insurance businesses. • • Also allowed financial services firms to offer banking services. • Savings Banks and Credit Unions • • Offer may of the same services as commercial banks. • • In U.S., 1,300 savings banks with $1.7 trillion in assets. • • More than 70 percent of loans are for home mortgages. • • Credit unions are cooperative financial institutions owned by their members. • • 85 million Americans belong to one of the U.S.’s 9,200 credit unions. • • Credit unions have $650 billion in assets. • • Laws requiring that members share similar occupations or other traits keep their size small.

Nondepository Financial Institutions • Insurance Companies • • Households and businesses buy insurance to transfer risk from selves to insurance company. • • Underwriting The process insurance companies use to determine whom to insure and what to charge. • • Have total assets of $4 trillion. • Pension Funds • • Provide retirement benefits to workers and their families. • • Have $6.5 trillion in assets. • Finance Companies • • Offer short-term loans to borrowers in exchange for collateral.

THE FEDERAL RESERVE SYSTEM • Federal reserve system U.S. central bank. • • Four basic responsibilities:• Regulating commercial banks • • Performing banking-related activities for the U.S. Treasury • • Providing services for banks • • Monetary policy • Organization of the Federal Reserve System • • Nation divided into 12 federal districts. • • Each district bank supplies banks within its district with currency and facilitates the clearing of checks. • • Governed by a board of directors. • • Federal Open Market Committee sets monetary and interest rate policies.

Check Clearing and the Fed • • Americans write billions of checks each year. Desired outcomes Money deposited in store’s account Consumer writes check Process If both use the same bank Money withdrawn from consumer’s account Store deposits check in its bank If they use different banks Store’s bank deposits check at Federal Reserve Bank Federal Reserve Bank withdraws funds from consumer’s bank; transfers funds to store’s bank

Monetary Policy • Monetary policy Using interest rates and other tools to control the supply of money and credit in the economy. • • If money supply grows to slowly, unemployment will increase. • • If money supply grows too quickly, inflationary pressures will build. • • If Fed raises interest rates: • • The growth rate in the money supply will slow. • • Economic growth will slow. • • Inflationary pressures will ease. • • If Fed pushes rates down:• The growth rate in the money supply will increase. • • Economic growth will pick up • • Unemployment will fall.

U.S. FINANCIAL INSTITUTIONS: A GLOBAL PERSPECTIVE • • Major U.S. bankshave extensive international operations. • • U.S. banks have more than $200 billion in outstanding loans to international customers. • • Only 3 of the 20 largest banks in the world (measured by total assets) are U.S. institutions • • Japan’s Mitsubishi UFJ Holdings is world’s largest. • • More than $1.7 trillion in assets. • • Other nation’s central banks play roles much like the Fed, often responding to changes in the U.S. financial system.