Download

1 / 38

400 likes | 565 Views

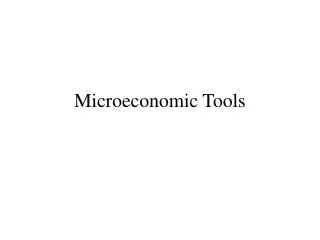

Slide Show #8. Microeconomic Concepts Related to Price and Growth . Single Input-Output Relationships. Costs associated with levels of output. $45. P=MR=AR. Profit maximizing level of output, where MR=MC. 11.2. Where is the firm’s supply curve?. P=MR=AR. Marginal cost curve

E N D

Slide Show #8 Microeconomic Concepts Related to Price and Growth

$45 P=MR=AR Profit maximizing level of output, where MR=MC 11.2

Where is the firm’s supply curve? P=MR=AR

Marginal cost curve above AVC curve? P=MR=AR

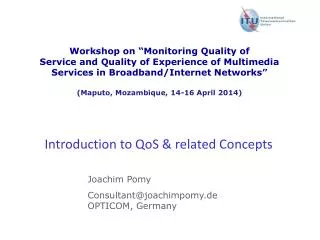

Use a variable input like labor up to the point where the value received from the market equals the cost of another unit of input, or MVP=MIC D C E B F G 5 I H J

D If you stopped at point E on the MVP curve, for example, you would be foregoing all of the potential profit lying to the right of that point up to where MVP=MIC. C E B F G 5 I H J

If you went beyond the point where MVP=MIC, you begin incurring losses. D C E B F G 5 I H J

Least Cost Input Choice for 100 Units At the point of tangency, we know that: slope of isoquant = slope of iso-cost line, or… MPPLABOR÷ MPPCAPITAL = - (wage rate÷ rental rate)

What Inputs to Use for a Specific Budget? Firm can afford to produce only 75 units of output using C3 units of capital and L3 units of labor

How to Expand Firm’s Capacity Optimal input combination for output=10

How to Expand Firm’s Capacity Two options: 1. Point B ?

How to Expand Firm’s Capacity Two options: 1. Point B? 2. Point C?

Expanding Firm’s Capacity Optimal input combination for output=20 with budget FG Optimal input combination for output=10 with budget DE

Expanding Firm’s Capacity This combination costs more to produce 20 units of output since budget HI exceeds budget FG

Expanding Firm’s Capacity Expansion path

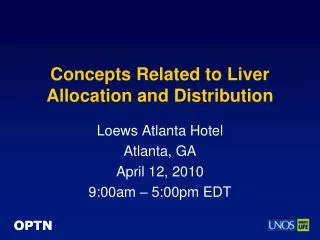

The Planning Curve The long run average cost (LAC) curve reflects points of tangency with a series of short run average total cost (SAC) curves. The point on the LAC where the following holds is the long run equilibrium position (QLR) of the firm: SAC = LAC = PLR where MC represents marginal cost and PLR represents the long run price, respectively.

What can we say about the four firm sizes in this graph?

Size 1 would lose money at price P

Firm size 2, 3 and 4 would earn a profit at price P…. Q3

If price were to fall to PLR, only size 3 would not lose money; it would break-even. Size 4 would have to down size its operations!

Firm is a “Price Taker” Under Perfect Competition The Market The Firm Price Price D S AVC MC PE QE OMAX Quantity

If Demand Increases…… The Market The Firm Price D1 Price D S AVC MC PE QE 10 11 Quantity

If Demand Decreases…… The Market The Firm Price Price D S D2 AVC MC PE QE 9 10 Quantity

Firm is a “Price Taker” in the Input Market Labor Market The Firm Price Price D S MVP MIC PE QE LMAX Quantity

If Demand Increases…… Labor Market The Firm Price Price D S MVP PE MIC QE LMAX Quantity

Total revenue is equal to the area 0PECQE, which forms the blue box to the left… Notice the monopoly, like the previous forms of imperfect competition, produces where MC=MR (point A), but then reads up to the demand curve (point C) when setting price PE.

Total variable costs for the monopolist is equal to area 0NAQE, or the yellow box to the left.

Total fixed costs for the monopolist is equal to area NMBA, or the green box to the left…

Total cost is therefore equal to area 0MBQE, or the green box plus the yellow box to the left.

Finally, the economic profit earned by the monopolist is equal to area MPECB, or total revenue (blue box) minus total costs (green box plus yellow box).