Download

1 / 43

430 likes | 528 Views

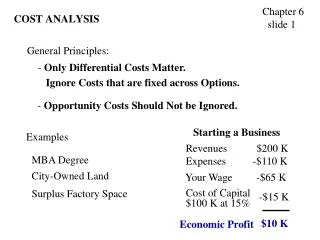

Cost Analysis Techniques. Project. something related to purchasing how the purchasing function affects a company? how can a company improve its purchasing functions? possible forms a case study on a company literature review on a topic related to purchasing methodology

E N D

Project something related to purchasing how the purchasing function affects a company? how can a company improve its purchasing functions? possible forms a case study on a company literature review on a topic related to purchasing methodology management principle 2

Project Proposal a 15-minute presentation what is it about? why is the project important? Useful? Interesting? how will you proceed? what are the expected results? Expected challenges? examples 3

Outline collaborative cost management total cost ownership model Kazuo Inamori’s idea on pricing and costing activity-based costing value analysis and value engineering process mapping learning curve quantity discount 4

Collaborative Approaches to Cost Management target pricing: price acceptable by market, or price for competition searching for design methods, material, and production process to match the target price reducing the gap between the target price and the actual price provided by suppliers cost-saving sharing: incentive offered to a vendor for cost saving pre-requisites information sharing vendor to buyer: details of production process, cost structure buyer to vendor: quantity, quality requirements, plan from near to intermediate term agreement on cost saving sharing example: data setting and calculation 6

Total Cost Ownership Model costs throughout the life cycle of an item hidden cost in purchasing#1 payment method, inflation, life, salvage value, auxiliary charge, packaging, transportation, installation, service support, training, maintenance, service parts, etc. example: cost structure and calculation #1 Zeger Degraeve and Filip Roodhooft (2001) A Smarter Way to Buy, Harvard Business Review. 8

『稲盛和夫の実学 経営と会計』稻盛和夫的實學 :會計與經營Kazuo Inamori's Pragmatic Studies: Management and Accounting いなもり かずお稲盛 和夫Kazuo Inamori 9

Some Ideas in the Book core of business: divine doctrine(天道)、 self-evident truth (公理)、 consensusand concord (人心) cash-basis management: a grip on true cash flow of company fair accounting: one-to-one correspondence between orders and items muscular management: the cheapest method for a given task perfectionism transparency amoeba management double-checking system with shared responsibility 10

Some Glimpses ofPragmatic Studies: Management and Accounting the difference between reality and accounting rules standard accounting rules for depreciation of machines difference between actual working life of a machine and its depreciation life by rules 11

Some Glimpses ofPragmatic Studies: Management and Accounting asset or cost? would equipment for production an asset or cost? example: a stall selling banana a box of ¥300; a table cloth of ¥1,000; a stick of ¥200 buying 20 hands of banana, ¥50 per hand, selling at ¥150 per hand all sold out how much profit ¥2,000 or ¥500? TAX!!! 12

Some Glimpses ofPragmatic Studies: Management and Accounting difference among book profit, actual profit, and cash flow distortion of actual profit by accounting rules, classification of asset cost, account payable and account receivable, etc. 13

Questions Pricing and costing of an item are always important issues in purchasing. Discuss what you have learnt about these two issues from the book “Kazuo Inamori's Pragmatic Studies: Management and Accounting” by Dr. 稻盛和夫. 14

Pricing and Costing Issues in Pragmatic Studies: Management & Accounting overhead cost depreciation: difference in law and in reality inventory and equipment as resource or liability obsolete inventory and equipment, especially for small production lot price setting first item price acceptable to market then (material and production) cost matching with the price 15

Activity-Based Costing (ABC) assigning overhead of a product or service traditional cost accounting based on fixed percentage of direct labor, direct material, or both direct labor and material more overhead for high volume items ABC trace the cause and effect of overhead cost drivers: activities in the overhead for the product or service 17

Example#1 a factory producing only 2 products, L & S 1,500 pieces of L & 150 pieces of S setups: 2 for each product, each of $900 direct material cost: L $2 and S $3 ignoring labor cost for simplicity #1許振邦(2007)採購與供應管理(originally from Raedels (2000) 18

A Single-Item Example DLH = Direct Labor Hours Fixed Burden Rate (TC) = Estimated Annual Factory Fixed Manufacturing Overhead/Estimated Annual Factory DLH = $967,500/15,000 DLH = $64.50/DLH 20

MH = Machine Hours; Insp. = Inspections; ECO = Engineering Change Orders Fixed Rate (ABC) = Estimated Annual Factory Fixed Manufacturing Overhead / Estimated Annual Factory MH = $500,000/40,000 MH = $12.50/MH 21

Value Analysis and Value Engineering value analysis: examining all elements of a component, assembly, end product, or service to make sure it fulfills its intended function at the lowest total cost value engineering: application of value analysis principles during product or service design value = function/cost 23

Personnel in Value Analysis everyone: executive management, suppliers, supply management, design engineering, marketing, production, industrial/process, engineering, quality control 24

Typical Questions to Ask in VA Does the use of this product contribute value to our customers? Is the cost of the final product proportionate to its usefulness? Are there additional uses for this product? Does the product need all its features or internal parts? Are product weight reductions possible? Is there anything else available to our customers given the intended use of the product? Is there a better production method to produce the item or product? Can a lower cost standard part replace a customized part? Are we using the proper tooling considering the quantities required? 25

Typical Questions to Ask in VA Will another dependable supplier provide materials, components, or subassemblies for less? Is anyone currently purchasing required materials, components, or subassemblies for less? Are there equally effective but lower cost materials available? Do material, labor, overhead, and profit equal the product’s cost? Are packaging reductions possible? Is the item properly classified for shipping purposes to receive the lowest transportation rates? Are design or quality specification too tight given customer requirements? If we are making the item now, can we buy it for less? Or vice versa? 26

Value Analysis Process gather information speculate analyze recommend and execute summarize and follow up 27

Value Analysis Process gather information what does this product do for the customer? why does a customer buy this product? primary vs. secondary functions name each function with a noun and a verb collect detailed product information speculate wide-open, creative thinking use brainstorming or other idea creating techniques develop as many improvement ideas as possible without judgment 28

Value Analysis Process analyze perform critical evaluation of ideas created in speculate stage cost/benefit analyses feasibility assessment do ideas address the original goals and objectives? general specific recommend and execute determine priorities make proposal to management for approval requires: motivation and creativity good communication skills analytical thinking and product knowledge commitment and salesmanship 29

Value Analysis Process summarize and follow up implement timing budget responsibilities generate support from outside the team 30

Example of Value Analysis rescue of Nissan by Carlos Ghosn reduction of design cost by eliminating special parts or components condition: without compromising quality, service, or both headlight some components better than competitors minor differences not picked up by eyes reducing cost by 2.5% by changing reflectors and illuminators 31

Example of Value Analysis rescue of Chrysler by Lee Iacocca design of K-car: no more than 176” to pack more car in transportation 32

Example of Value Analysis experience of 4 first-tier suppliers of automobiles benefits and challenges to leverage their suppliers’ expertise in collaborative VA process benefits and barriers Hartley, J.L. (2000) Collaborative Value Analysis: Experiences from the Automotive Industry, The Journal of Supply Chain Management, Fall, 27-32. 33

Process Mapping process: an outcome of a set of tasks, activities, or steps expressing processes as their component parts or activities by a cross-functional team identifying and eliminating non-value-added activities 35

Process Mapping Example Non-value-adding Value-adding 36

Process Mapping Example • Remove non-value-adding steps • Seek to combine other steps Non-value-adding Value-adding 37

Learning Curve reduction of production time due to repetition of task empirical evidence: learning rate as production double e.g., 85% learning rate: reduction of 15% direct labor as production double 39

Example on Learning Curve first order 200 pieces at $228/unit material $90; direct labor $50 (5 hours per unit, at $10 per hour) overhead at 100% of direct labor profit margin 20% total cost per unit = ($90+$50+$50) = $190 price per unit = ($190)(120%) = $228 40

Example on Learning Curve price for another 600 pcs for 80% learning rate average time for 800 units = 5(0.8)2 = 3.2 hr total time for 800 units = (3.2)(800) = 2,560 hr total time for the additional 600 units = 2,5601,000 = 1,560 hr direct labor cost per unit = $(10)(1560)/600 = $26 total cost per unit = ($90+$26+$26) = $142 price per unit = ($142)(120%) = $170.4 41

Quantity Discount Analysis is a discount scheme reasonable? for better understanding of incremental price two types of quantity discount: prices at specific quantities vs. prices at quantity ranges quantity discount analysis for price breaks at specific quantities 1 unit @ $85 each 3 units @ $80 each 6 units @ $70 each 10 units @ $69 each 42

Quantity Discount Analysis Number of 1 3 6 10 units/order Price/unit (quoted) $85.00 $80.00 $70.00 $69.00 $85.00 $240.00 $420.00 $690.00 Total price/order Price difference $85.00 $155.00 $180.00 $270.00 between orders Quantity 1 2 3 4 difference/order Price/unit/order $85.00 $77.50 $60.00 $67.50 quantity difference 43