Download

1 / 48

540 likes | 1.3k Views

And why Enron, Satyam Computers and Nepal Development Bank collapsed. OECD Principles on Corporate Governance. Presented by: GROUP 1, EMBA 2009, Corporate Law Bibek Pandeya Bikash Shrestha Sandesh Dhakal Sanjeeb Jha Sulabh Tuladhar. Introduction to OECD Principles.

E N D

And why Enron, Satyam Computers and Nepal Development Bank collapsed OECD Principles on Corporate Governance Presented by: GROUP 1, EMBA 2009, Corporate Law • BibekPandeya • Bikash Shrestha • SandeshDhakal • SanjeebJha • Sulabh Tuladhar

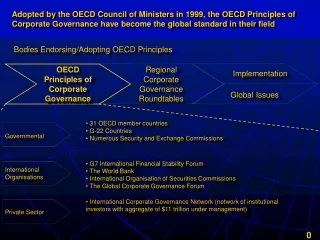

Introduction to OECD Principles • The integrity of businesses and markets is central to the vitality and stability of our economies. • Good corporate governance contributes to growth and financial stability by underpinning market confidence, financial market integrity and economic efficiency.

Introduction to OECD Principles • The OECD (Organization of Economic Corporations Development) Principles of Corporate Governance provide specific guidance for policymakers, regulators and market participants in improving the legal, institutional and regulatory framework that underpins corporate governance, with a focus on publicly traded companies.

Introduction to OECD Principles • They also provide practical suggestions for stock exchanges, investors, corporations and other parties that have a role in the process of developing good corporate governance. They have been endorsed as one of the Financial Stability Forum’s 12 key standards essential for financial stability.

Introduction to OECD Principles • The OECD Principles were originally issued in 1999 and have since become the international benchmark for corporate governance, forming the basis for a number of reform initiatives, both by governments and the private sector.

Key Principles and issues that OECD addresses • The Principles cover 6 key areas of corporate governance: • Ensuring the basis for an effective corporate governance framework. • The rights of shareholders. • The equitable treatment of shareholders. • The role of stakeholders in corporate governance. • Disclosure and transparency. • The responsibilities of the board.

Satyam Computers and Corporate Governance • In the context of Satyam Computer's new scam, while adopting the present model of Corporate Governance there was discussions over its suitability for a country like India. • The reason - they were copying western model of corporate governance. • Professor J. Rama Varma of IIM Bangalore had extensively commented on the unsuitability of the Western Code of Corporate Governance in his well researched paper on the subject titled 'Corporate Governance in India: Disciplining the dominant shareholder'. J.RamaVarma did research on 1997.

Satyam Computers and Corporate Governance • Satyam is a company which had won the Golden Peacock Global Award for excellence in Corporate Governance. This company was named the winner by the World Council for Corporate Governance as recently as in September 2008. This is after approving the false balance sheet presented in the Board of Directors. • The Satyam story poses a big question over the credibility of auditors in general, as Price Waterhouse Coopers was the auditor of the company. The bankers to Satyam included Bank of Baroda, BNP Paribas, ICICI, HDFC, CitiBank, HSBC. Even after placing false account details in its balance sheet no bank came out and asked details about it.

Satyam Computers and Corporate Governance • Satyam was also being accused by the World Bank for bribing its employees to get certain contracts awarded in the company's favor. • In one of the biggest frauds in India’s corporate history, B. RamalingaRaju, founder and CEO of Satyam Computers, India’s fourth-largest IT services firm, announced on January 7 that his company had been falsifying its accounts for years, overstating revenues and inflating profits by $1 billion.

Satyam’s reason for failure • On the basis of ensuring for an effective corporate governance framework, what should have promoted transparent and efficient markets, along with being consistent with the rule of law and clearly articulate the division of responsibilities among different supervisory, regulatory and enforcement authorities, it showed that the company had been feeding investors, shareholders, clients and employees a steady diet of lies.

Satyam’s reason for failure • The rights of shareholders and key ownership functions where the corporate governance framework should have protected and facilitated the exercise of shareholders’ rights, it was mentioned in a letter addressed to the board, the stock exchanges and the market regulator Securities & Exchange Board of India (SEBI) that Satyam’sprofits were inflated over several years to “unmanageable proportions” and that it was forced to carry more assets and resources than its real operations justified.

Satyam’s reason for failure • The equitable treatment of shareholders objective states that the corporate governance framework should ensure the equitable treatment of all shareholders, including minority and foreign shareholders. All shareholders should have the opportunity to obtain effective redress for violation of their rights. • Satyam’sstocks were listed on the Bombay Stock Exchange as well as the New York Stock Exchange. International regulators could swing into action if they believed U.S. laws had been broken. At least two U.S. law firms have filed class-action lawsuits against Satyam, but given the company’s precarious finances, it is unclear how much money investors will be able to recover.

Satyam’s reason for failure • The corporate governance framework should recognize the rights of stakeholders established by law or through mutual agreements and encourage active co-operation between corporations and stakeholders in creating wealth, jobs, and the sustainability of financially sound enterprises.

Satyam’s reason for failure • Also, the corporate governance framework should ensure that timely and accurate disclosure is made on all material matters regarding the corporation, including the financial situation, performance, ownership, and governance of the company. • But, it was acknowledged that Satyam’s balance sheet included Rs. 7,136 crore (nearly $1.5 billion) in non-existent cash and bank balances, accrued interest and misstatements. It had also inflated its 2008 second quarter revenues by Rs. 588 crore ($122 million) to Rs. 2,700 crore ($563 million), and actual operating margins were less than a tenth of the stated Rs. 649 crore ($135 million).

Satyam’s reason for failure • The corporate governance framework should ensure the strategic guidance of the company, the effective monitoring of management by the board, and the board’s accountability to the company and the shareholders. • This is where Satyam failed miserably.

Decision of the Court • Hyderabad, Jan 28: A local court in India dismissed the bail petitions of disgraced Satyam founder B. RamalingaRaju, his brother and former MD of the company and its ex-CFO, V. Srinivas, but their counsel stated that a review petition will be filed or they will go to a higher court.

Conclusion and Analysis • B. RamalingaRaju, who is politically influential, disclosed details of the fraud in a resignation letter to the company’s board of directors forwarded to stock exchange authorities as well as the regulator of the country’s capital markets, the Securities and Exchange Board of India (SEBI). • Of the revenue reported as of Sep.30, 2008, the letter said, almost 1.03 billion dollars, or 95 percent, never existed.

Conclusion and Analysis • An alarming aspect of the episode was that B. RamalingaRaju acknowledged that his company’s financial records had been fudged and manipulated for the "last several years". • "It was like riding a tiger, not knowing how to get off without being eaten," wrote the disgraced Raju in his letter.

Conclusion and Analysis • "It’s a wake-up call for the Indian corporate sector," said Ashok Kumar Bhattacharya, national managing editor of Business Standard newspaper in an exclusive interview to IPS. "Companies have to stick to the rule-book," he added.

Enron and Corporate Governance • “When a company called Enron… ascends to the number seven spot on the Fortune 500 and then collapses in weeks into a smoking ruin, its stock worth pennies, its CEO, a confidante of president, more or less evaporated, there must be lessons in there somewhere.” -Daniel Henninger, The Wall Street Journal

Enron and Corporate Governance • With the demise of Enron, corporate governance has come to the forefront of economic discussion. The fall of Enron was a direct result of failed corporate governance and consequently has led to a complete re-evaluation of corporate governance practice in the United States.

Reasons for Enron’s failure • According to Newsweek's estimates, Enron lost $2 billion on broadband, $2 billion on water, $2 billion on a Brazilian utility and $1 billion on an electricity plant in India. • To hide their debt, Enron engaged in "aggressive accounting."

Reasons for Enron’s failure • They created partnerships with nominally independent companies. • Those companies were headed by Enron execs, and backed, ultimately, by Enron stock. • But Enron did not count their "partners"' debt as its own, using "off-balance-sheet" accounting. • Enron also found ways to count loans from banks as "profit." • These all resulted in Enron’s bankruptcy.

Reasons for ENRON’s failure • The Enron failure demonstrated a failure of corporate governance, in which internal control mechanisms were short-circuited by conflicts of interest that enriched certain managers at the expense of the shareholders. • Enron’s actions appear to have been undertaken to mislead the market by creating the appearance of greater creditworthiness and financial stability than was in fact the case. The market in the end exercised the ultimate sanction over the firm.

Reasons for ENRON’s failure • There is no evidence that existing regulation is inadequate to solve the problems that did occur. Had Enron complied with existing market practices, not to mention existing accounting and disclosure requirements, it could not have built the house of cards that eventually led to its downfall. • It is likely that additional government regulation, by increasing moral hazard and decreasing legal certainty, could have the unintended consequence of making future failures and market instability more likely along with increasing the cost and decreasing the availability of risk management tools.

Approaches to Balance Corporate Power • Corporate governance structures have traditionally been a private matter between shareholders and managers with some state law restrictions, but the Sarbanes-OxleyAct has made structures governing the conduct of the corporation a matter of federal law.

Sarbanes-Oxley Act • Sarbanes-OxleyAct addresses the perceived weaknesses in auditing, reporting and corporate governance of U.S public companies and has been hailed as the most dramatic change to federal securities law in over 50 years.

Sarbanes-Oxley Act • Some of the provisions of Sarbanes-OxleyAct and new stock exchange rules can be listed as: • Strengthening corporate responsibility through governance. • Listed company must have a majority of independent directors. • Non management or independent directors must meet without management in regularly scheduled executive sessions. • The Audit Committee is responsible for the fiscal integrity of the corporation. • It is illegal for officers and directors to fraudulently influence an independent auditor. • Company Codes of Ethics is essential and changes are to be notified. • Accelerated reporting of and new restrictions on trading by insiders. • Future personal loans to officers and directors are prohibited. • Real time disclosures of important changes.

Problem • The systemic problems at Enron arose because of an imbalance of power in favor of top management in corporate organizations. • The shift in power from shareholders to management started with the appearance of large corporations as a result of the Industrial Revolution, when small capitalists pooled their resources to finance bigger ventures that were operated by professional managers referred to subsequently as “managers for hire.”

What went wrong with Enron • One of the obvious systemic causes of the Enron scandal is the legal and regulatory structure. • A private company like Enron hired and paid its own auditors. • Most large companies like Enron are allowed to manage their own employee pension funds. • Most companies like Enron have codes of ethics that prohibit managers and executives from being involved in another business entity that does business with their own company. But these codes of ethics are voluntary and can be set aside by the board of directors. The legal structure largely allows managers to enter these arrangements, which constitute a conflict of interest.

Nepal Development Bank Limited • Nepal Development Bank Limited (NDBL) has been established under the Company Act, 2053 (1997) in March 19,1998. • It is the first national level development bank established by the private sector in Nepal. • It has commenced its operation January 31, 1999 as per Development Bank Act, 2052 (1996). • Since May 4, 2006 it has been imparting its services in accordance with Bank and Financial Institution Act, 2063.

Principles of Corporate Governance in Banking Sector OECD focus on the following critical elements of desirable corporate Governance for the banks. • Board members should be qualified for their positions, have a clear understanding of their role in corporate governance and be able to exercise sound judgment about the affairs of the bank. • The board of directors should approve and oversee the bank’s strategic objectives and corporate values that are communicated throughout the banking organization. • The board of directors should set and enforce clear lines of responsibility throughout the organization.

Principles of Corporate Governance in Banking Sector • The board and senior management should effectively utilize the work conducted by the internal audit function, external auditors, and internal control functions. • The board should ensure that compensation policies and practices are consistent with the bank’s corporate culture, long-term objectives and strategy, and control environment • The bank should be governed in a transparent manner. • The board and senior management should understand the bank’s operational structure, including where the bank operates in jurisdictions, or through structures, that impede transparency (“know-your structure”) • The board should ensure that there is appropriate oversight by senior management consistent with board policy

Liquidation Decision • Under clause 74 of the Banks and Financial Institutions Act, NRB must file a case to begin of liquidation of a financial institution whose damages are beyond repair. Before filing the case NRB must seek justification from the bank. • Explanation sought by NRB to NDB on June 3,2009 – why it should not be liquidated. • NDB submitted its reply seeking time till October 2009, saying new investors would be ready to invest in it then. • Seized all cash, cheques and securities.

The central bank has stated that these officials committed crimes under Clause 95 of the NRB Act 2001 and embezzled bank assets and cash, which is a crime under Clause 1 and 2 of the Civil Code (Fraud). • NRB has sought action against the culprits as per Clause 96 of the NRB Act and Clause 4 of the Civil Code. "Those officials abused their authority to take illegal financial benefit, while causing serious damage to the financial health of the bank and ultimately pushing it to bankruptcy. • Nepal Rastra Bank on July 9,2009 requested the Home Ministry to take action against Nepal Development Bank (NDB)’s patron Uttam Pun and chairman AmarGurung as well as other senior management members. They have been charged of misusing NDB assets worth Rs. 1.08 billion.

Liquidation Decision • Accumulated loss 678.6 million by the end of mid-March, 2009. Non-performing loan 30 percent. • Required capital adequacy ratio 11 percent. NDB's capital adequacy negative by 41 percent. • Issued Right Shares – to increase capital. • Board members did not applied for rights shares - bad intentions.

Liquidation Decision • NRB had repeatedly warned NDB and declared it ‘problematic’ in 2007. • Rana Bahadur Bam and BhoopdhojAdhikari at the PatanAppallate Court had issued ex-parte stay order overturning the NRB’s decision. • Depositors cannot withdraw their money after NRB’s move.

According to Chairman of NDB - AmarGurung: • "NDB only has an accumulated loss of Rs 620 million, whereas RastriyaBanijya Bank has an accumulated loss of Rs 15.13 billion, and Nepal Bank Limited has an accumulated loss of Rs 5.51 billion; even private sector banks such as Nepal Bangladesh Bank has an accumulated loss of around two billion rupees, and Nepal Credit and Commerce Bank has an accumulated loss of Rs 420 million”. • "Is NRB trying to liquidate them as well? We need an answer. If it is not, is NRB, which should be playing a guardian´s role, discriminating among banks?"

The Association of Nepali Development Banks and the Association of Nepali Finance Companies have also asked NRB not to liquidate the bank, but to instead, make efforts to revive its financial condition by working together.

REVIVING NDB • Two groups have submitted proposals to investigation officer T.R Upadhyaya to revive troubled Nepal Development Bank (NDB). • Nimbus Group of JagdishAgrawalalongwith World Link, ICTC Group, Golchha Group, Kailash Chandra Goyal, Ravi Singh Group, Guna Chandra Bista and others have submitted one proposal. • BadriBhattarai, the current promoter of NDB, and his group have submitted another proposal.

Significance of Corporate Governance in Banking Sector • Banks & FI depends on Other Peoples Money (OPM). • There may be a gap among major stakeholder - owners, depositors and management. • Limited people have a right to access in resources and decision.

CG in Nepalese Banking Sector • Nepal implemented the Basel II from 2008 July in banking sector and good corporate governance forms important part of Basel II. • Basel Committee has introduced principles on Enhancing Corporate Governance for Banking Organizations (2006 revised version of the principles introduced in 1999) • BIS (Bank for International Settlement) OECD (Organization of Economic Co-operation and Development)

Existing Laws and Regulation • Banks and Financial Institutions Act 2063 • Directive 6 issued by the NRB • Companies Act 2063

Issues related to Regulators • Lack of institutional capacity for enforcement of laws, regulations. • Enforcement authorities themselves lack good governance. • Lack of accountability of employees of regulating bodies (need to have internal rules) . • Lack of resources within regulator . • Transparent and scientific licensing policy . • Lack of political and leadership will. • Court have frequently intervened in regulatory enforcement

Issues related to BOD • Board members are interested to use public deposits as their own assets which is against the BAFIA 2063, article 48 . • Generally, Board members (non executive) are liking to use power like executive or, executive director and executive chairman in the area of loan sanction, employee selection and daily office activities which is again the against the BAFIA, 2063 article 24.

Board members are prohibited take loan from own company however, it is general practice to take loan directly or, indirectly. • Big houses running many same nature business are manipulating public deposits and transferring the fund within the group in their own interest.

Conclusion • The responsibility for good governance lies within the bank’s and FIs’ senior management. Regulators can only facilitate but not ensure improved governance. Last but not least, we would like to say SELF REGULATION IS BEST REGULATION.

End of Presentation Thank you.