Download

1 / 3

50 likes | 743 Views

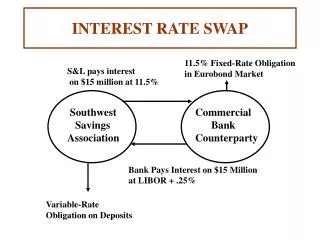

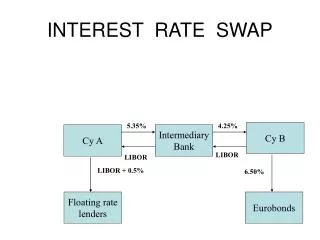

INTEREST RATE SWAP. 5.35%. 4.25%. Cy B. Cy A. Intermediary Bank. LIBOR. LIBOR. LIBOR + 0.5%. 6.50%. Floating rate lenders. Eurobonds. CROSS CURENCY & INTEREST RATE SWAP. Bank of Commonwealth Swap with Notional Deposit A$ 200 Mio Facility US$ 170 Mio. Fixed US$

E N D

INTEREST RATE SWAP 5.35% 4.25% Cy B Cy A Intermediary Bank LIBOR LIBOR LIBOR + 0.5% 6.50% Floating rate lenders Eurobonds

CROSS CURENCY & INTEREST RATE SWAP Bank of Commonwealth Swap with Notional Deposit A$ 200 Mio Facility US$ 170 Mio Fixed US$ Interest at 5.25% A$ 200 Mio US$ 1 = A$ 1.1125 ANZ transact Swap Contract, Starting spot FX Deutsche Bank Initial exchange 4/2008 Swap Counterparty Interest Flows for US$ 170 Mio loan US$ 178 Mio Floating A$ Interest LIBOR+1.28% Floating A$ Interest LIBOR +1.25% Fixed US$ Interest At 5.5% US$ 170 Mio A$ 200 Mio A$ 200 Mio A$ 200 Mio Floating rate Bond Due 4/2013 Company A Fixed US$ Interest At 6% Deutsche Bank Interest flows Swap Counterparty Interest Flows for A$ 200 Mio deposit Floating A$ Interest LIBOR + 2.5% Floating A$ Interest LIBOR + 1.5% A$ 200 Mio proceeds US$ 170 Mio A$ 200 Mio A$ 200 Mio ANZ transact Forward in accord To Swap contract Deutsche Bank final exchange 4/2013 US$ 160 Mio US$ 1 = A$ 1.25

CROSS CURENCY & ZERO COUPON SWAP A$ 125 Mio US$ 1 = A$ 1.1125 Floating A$ Interest LIBOR+1.5% A$ 200 Mio ANZ transact Swap Contract, Starting spot FX Deutsche Bank Initial exchange 4/2008 Bank of Commonwealth Deposit A$ 200 Mio A$ Debtor Interest Flows A$ 200 Mio US$ 113 Mio Floating A$ Interest LIBOR +2% US$ 110 Mio A$ 125 Mio A$ 200 Mio A$ 200 Mio Floating rate Bond Due 4/2013 Company A Baloon amount of US$ 60 Mio Deutsche Bank Interest flows Floating A$ Interest LIBOR + 2.5% Floating A$ Interest LIBOR + 1.5% A$ 125 Mio proceeds US$ 60 Mio US$ 110 Mio A$ 200 Mio A$ 200 Mio Deutsche Bank final exchange 4/2013 ANZ transact Forward in accord To Swap contract US$ 100 Mio US$ 1 = A$ 1.25