Fraud Theories

Fraud Theories. Dr. Raymond S. Kulzick, CPA, CFE St. Thomas University Miami, Florida Copyright 2004 R. S. Kulzick. Fraud Theories. Sutherland – White Collar Crime Cressey – Fraud Triangle Albrecht – Fraud Scale Hollinger - Clark Study. Edwin H. Sutherland.

Fraud Theories

E N D

Presentation Transcript

Fraud Theories Dr. Raymond S. Kulzick, CPA, CFE St. Thomas University Miami, Florida Copyright 2004 R. S. Kulzick

Fraud Theories • Sutherland – White Collar Crime • Cressey – Fraud Triangle • Albrecht – Fraud Scale • Hollinger - Clark Study

Edwin H. Sutherland • 1939 First defined “white-collar crime” • Criminal acts of corporations • Individuals in corporate capacity • Theory of differential association • Crime is learned • Not genetic • Learned from intimate personal groups

Cressey’s Offender Types • 1. Independent businessmen • “Borrowing” • Funds really theirs • 2. Long-term violators • “Borrowing” • Protect family • Company cheating them • Company generally dishonest

Cressey’s Offender Types • 3. Absconders • Take the money and run • Usually unmarried, loners • Blame “outside influences” or “personal defects

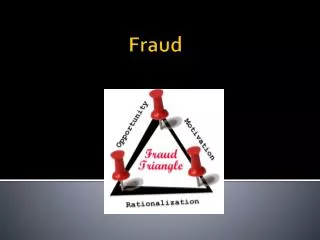

The Fraud Triangle PRESSURE RATIONALIZATION OPPORTUNITY

Nonsharable Problems • Violation of ascribed obligations • Personal failures • Business reversals • Physical isolation • Status gaining • Employer-employee relations

Pressure • Financial • Vice • Work-related • Other

Opportunity • Controls • Environment • Accounting • Procedures • Performance quality • Discipline perpetrators • Access to information • Ignorance, apathy, incapacity • Audit trail

Rationalization • They owe me • Borrowing • Nobody will get hurt • I deserve more • It’s for a good purpose

W. Steve Albrecht Nine motivators of fraud • Living beyond means • Overwhelming desire for personal gain • High personal debt • Close association with customers • Pay not commensurate with job

W. Steve Albrecht Nine motivators of fraud • Wheeler-dealer • Strong challenge to beat system • Excessive gambling • Family/peer pressure

The Fraud Scale • Situational pressures • Immediate problems with environment • Usually debts/losses • Perceived opportunities • Poor controls • Personal integrity • Individual code of behavior

Hollinger-Clark Study • Hollinger-Clark study (1983) • Surveyed 10,000 workers • Theft caused by job dissatisfaction • True costs vastly understated

Employee Deviance • Two categories: • Acts against property • Production violations (goldbricking) • Strong relationship: theft and concern over financial situation

Age and Theft • Direct correlation • Younger employees less committed • But, higher position = bigger theft • Opportunity is only a secondary factor

Job Satisfaction and Deviance • Dissatisfied employees • More likely to break rules • Regardless of age/position • Trying to right perceived inequities • Wages in kind

Organizational Controls • Some impact, but limited • Hollinger studied five aspects: • Company policy • Selection of personnel • Inventory control • Security • Punishment

Hollinger’s Conclusions • Employee perception of controls is important • Increased security may hurt, not help • Employee-thieves exhibit other deviance • Sloppy work, sick leave abuses, etc. • Management should be sensitive to employees • Pay special attention to young employees

Hollinger’s Conclusions Four key aspects of policy development • Understand theft behavior • Spread positive info on company policies • Enforce sanctions • Publicize sanctions

Overall Conclusion 1 • Perpetrators feel justified • Must counter this • Morally • Legally • Consequences

Overall Conclusion 2 • Concept of wages-in-kind • Hire the right people • Treat them well • Have reasonable expectations

Overall Conclusion 3 • Controls must pose a visible and highly likely threat of apprehension • Perception of detection is the greatest deterrent • Hidden controls do not deter • Controls cannot be predictable