Understanding Off-Balance Sheet Debt and Consolidation Methods in Financial Reporting

180 likes | 351 Views

This article delves into off-balance sheet debt, emphasizing Special Purpose Entities (SPEs), the equity method, and consolidation rules. It defines SPEs, their activities, and the accounting principles that govern their reporting. We explore partial versus full consolidation, including practical examples and their impact on financial ratios. Industries heavily reliant on debt, like energy and airlines, are highlighted for their strategic use of off-balance sheet financing. This analysis provides insights into how companies manage risks and optimize financial presentation.

Understanding Off-Balance Sheet Debt and Consolidation Methods in Financial Reporting

E N D

Presentation Transcript

Off-Balance Sheet Debt (SPEs, Equity Method) RCJ Chapter 11 (pg 583-585) & Chapter 16 (pg 891-895)

Key Issues • Special Purpose Entity (SPE) • Definition, types of activity • Rules for off-B/S accounting • Partial vs. full consolidation (to put on B/S) • Example • Ratio effects Paul Zarowin

Off-Balance Sheet Debt • In order not to appear too risky firms that operate in debt intensive industry, such as energy, communication and airline, try to keep debt off the balance sheet. • Construct deals in such a way as to avoid reporting debt/liabilities. • We’ll review several forms of off-balance sheet financing: • Special purpose entities • Equity method vs. consolidation of subsidiaries • Operating leases (vs. capital lease) • Synthetic leases Paul Zarowin

Special Purpose Entity (SPE) • Subsidiary, partnership, etc. set up for specific, finite period, activity. • Often highly leveraged (high ratio of debt/equity or debt/assets). • Also for ongoing investments, subs, joint ventures. Paul Zarowin

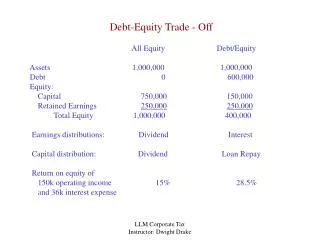

Consolidation of Subs, SPEs To avoid consolidation of SPE subsidiary, investment, or joint venture, parent must have: • 50% or less of sub’s common O/E, or • for SPE’s outside residual claim must bear substantial risk; de facto implementation has required 3% of total assets. Example: A = L + E SPE 100 94 6 P=parent 97 94 (upto 97) 3 (or less) Outside owner 3 0 3 key point: keep debt off of the Balance Sheet Paul Zarowin

Equity Method vs. Consolidation Equity method for parent investment in A or B: DR Investment 1 CR Cash or C/S 1 note: both sub’s have same BV of O/E = 1 (assume BV = MV, so GW = 0) sub’s A’s and L’s not recognized; only O/E recognized sub’s A’s and L’s recognized Paul Zarowin

One Line Consolidation • Under the equity method, subsidiaries’ net assets (A-L) collapse into one line usually called ‘investment’. • Equity method is often called “one line consolidation” Paul Zarowin

Effect of Consolidation on D/E and D/A P’s Equity method for A and B: Start with P’s A=L+E and add JE’s effects from slide #6 * no change since DR to sub’s assets is cancelled by CR to cash P consolidates A: (same as equity method since L = 0) P consolidates B: key issue: incentives for equity method vs. consolidation

Correction JE To go from equity method to consolidation: • sub A DR Assets 1 CR Investment 1 • sub B DR Asset 10 CR Investment 1 CR Liab 9 Key point: replace investment with assets and liabs Ex. P16-16, sections 1-3 Paul Zarowin

Solution (Correction JE): Partial or Full Consolidation Assume GW=0 P’s owns x% in Sub’s common O/E • P’s investment in sub: • External interest: common equity of sub owned by parties other than parent • Note: (3) I + E = O/E = A – L Key point: replace investment with assets and liabs

Example • Ex: Parent = Petroleum and Sub = Supply • P owns 40% of S and uses equity method (GW = 0) Parent: Sub: Q: What indicates the % Parent owns of Sub?

Proportionate (Partial) Consolidation Petroleum Equity Method + 40% * Supply = consolidated B/S Assets cash 100 8 DR 108 inventory 200 20 DR 220 A/R 300 20 DR 320 PPE 280 72 DR 352 investment 20 (20) CR - total assets 900 100 1000 liabs A/P 200 32 CR 232 LTDebt 200 68 CR 268 O/E 500 - 500 tot liab+O/E 900 100 1000 Remember: this j.e. eliminates investment (see slide #10)

Full Consolidation (balance sheet) Petroleum Equity Method + 100% * Supply = consolidated B/S Assets cash 100 20 DR 120 inventory 50 DR 250 A/R 300 50 DR 350 PPE 280 180 DR 460 investment 20 (20) CR - total asset 900 280 1180 liabs A/P 200 80 CR 280 LT Debt 200 170 CR 370 external interest - 30 CR 30 O/E 500 - 500 tot liab +O/E 900 280 1180 Remember: this j.e. eliminates investment (see slide #10)

Example (cont’d) Note: What % of subs’ A + L are recognized? equity method < proportionate consolidation < full consolidation: recognize more and more of the Sub’s assets and liabilities Note: P’s O/E is equal for • equity method; • proportionate consolidation; and • full consolidation • So D/E Paul Zarowin

Income Statement (assume no inter-company sales) Sub’s NI = 10; 40% * 10 = 4 = P’s equity in NI of S PSPropFull Rev 1000 200 1080 1200 Equity in NI of Sub 4 - - - CGS 800 140 856 940 SG&A 80 26 90 106 Int exp 20 17 27 37 External interest in S’s NI - - - 6 pre-tax inc 104 17 107 111 tax exp 40 7 43 47 NI 64 10 64 64 Note: #’s in bold are positive; #’s not in bold are negative Note: NI is equal for equity method, proportionate consolidation, full consolidation.

Consolidation JE for I/S • Proportionate: • Full: eliminate eliminate

Ratios RatioEquity methodProportionate ConsolFull Consol LTDebt/OE 200/500 = .40 268/500=.54 370/500=.74 ROA (NI/TA) 64/900=.071 64/1000=.064 64/1180=.054 Note: equity method proportionate consolidation full consolidation: ROA LTDebt/OE Note: Since P’s NI and O/E are equal under all 3 methods, ROE (= NI ÷O/E) is equal Ex. C16-5 Ratios Paul Zarowin

Ex: Partial or Full Consolidation with GW (GW = MV - BV of P’s Investment) x% = P’s ownership % in Sub’s common O/E • I = Investment = x% O/E + GW = (x% Assets - x% Liab) + GW • E = external interest = (1-x%) O/E = (1-x%) Assets - (1-x%) Liab • I + E = O/E + GW = A - L + GW Note: don’t recognize GW for external interest; only for fraction owned by parent