Download

1 / 15

150 likes | 265 Views

Reform Experiences in Eastern Europe HUNGARY. Csaba NAGY. STRUCTURE OF LONG TERM SAVINGS. VOLUNTARILY. Insurance business was set up in 1989 Voluntary mutual pension funds have been established since 1993 Mandatory private funds were set up during 1998 and 1999. Other savings. Insurance.

E N D

Reform Experiences in Eastern Europe HUNGARY Csaba NAGY

STRUCTURE OF LONG TERM SAVINGS VOLUNTARILY • Insurance business was set up in 1989 • Voluntary mutual pension funds have been established since 1993 • Mandatory private funds were set up during 1998 and 1999 Other savings Insurance Voluntary pension funds Mandatory Private Pension Funds State Social Security Pension OBLIGATORILY

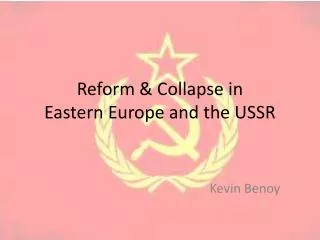

MAJOR INDICATORS ON SAVINGS Data as of December 31st, 2003 1 EUR = 266 hufs

Based on number of members Based on assets in 2003 Market participation – Mandatory Funds

KEY FEATURES (MPPF, VPF) • Non for profit organisations:any operation profits will be distributed among the members • Fully funded schemes • Tax incentives are granted: in order to stimulate people’s intention to savings • Defined contribution type of schemes: benefits will be determined based on the contributions paid on behalf of the member and the investment returns earned • Mutual ownership:members are the owners, representatives of the funds are appointed by the general assembly. Founders or employers may support the funds, however decisions will be made by the elected representatives of the members

Board of Directors General assembly of the members Supervisory Committee MEMBERS ORGANISATION STRUCTURE (VPF, MPPF) STATE SUPERVISORY AUTHORITY PROVIDERS • Bank account manager • Administrator • Asset manager • Custodian • Auditor • Other (Certificate Authority of digital signatures from 2005, etc.) SPONSORS

THE ROLE & IMPORTANCE OF FUNDS • The most efficient savings vehicle to provide pension supplement after retirement • Long-term savings generate demand on financial markets • 1.22 million persons, i.e.28.4 % of labourforce, joined to voluntary pension funds by the end of 2003. • Mandatory private funds covered 2.31 million persons by the end of 2003, i.e. 53.8 % of labourforce • Assets of voluntary funds increased to 1.633 million EUR by 2003; mandatory funds’ assets to 2.111 mEUR • It represents 2.34 % resp. 2.59 % of GDP by December 31, 2003 • It amounts to over 3% resp. 4 % of population’s financial savings

MAJOR ACHIEVEMENTS • Larger portion of the active labourforce opted for the two-pillar scheme than it was initially assumed by designers of the reform • Mandatory Private Pension Funds operate in competitive environment, therefore a strong emphasis is set on performance issues • The solutions applied to MPPFs provoke an enhanced transparency, accountability and better performance regarding the state PAYGO scheme • The developments in regulation and supervision of funds and providers (investors, trustees, auditors, administrators, etc.) tend to enhance quality of services in the interest of the members

For Voluntary Pension Funds: Possibility of withdrawal the account balance on maturity of the 10 year waiting period Market became saturated, thus the acquisition of new members is more costly Members and financial resources are being pulled by the growing health-care funds Treatment of non-paying members For Mandatory Pension Funds Market became saturated thus competition is growing Persistency became an issue Achievement of high investment returns in an underperforming stock and money market Obligation to recover due but unpaid membership fees proves a hard and costly requirement CHALLENGES

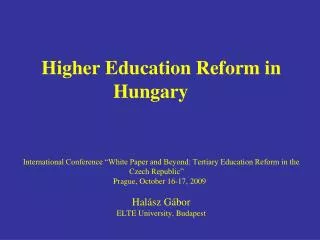

TYPICAL COSTS OF MANDATORY FUNDS Breakdown based on aggregate data for mandatory funds for 3 quarters in 2003 published by Hungarian Financial State Authority,