Download

1 / 11

110 likes | 129 Views

This review provides an overview of the rapidly growing Islamic finance industry, including the market for Islamic financial products and services such as sukuk (Islamic bonds), as well as a comparative analysis of sukuk versus conventional bonds and bank debt.

E N D

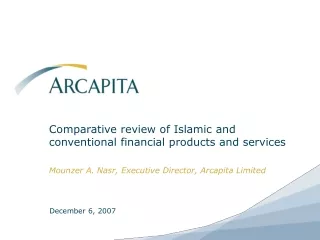

Comparative review of Islamic and conventional financial products and services Mounzer A. Nasr, Executive Director, Arcapita Limited December 6, 2007

Market Overview of Islamic finance • Over the last 10 years, Islamic finance has been growing very rapidly: • There are now over 300 institutions offering Islamic Financial products worldwide, managing assets in excess of $300 billion (as of End of 2006) • Assets at Islamic financial institutions have been increasing at an annual 10% in the Gulf and 15% worldwide over the past 10 years • Significant developments indicate that Islamic finance is no longer a niche market but increasingly becoming a mainstream industry: • Introduction of numerous sharia-compliant investment products in the US, European and Asian markets • Increasing number of corporates issuing sukuks (Islamic bonds) • A growing number of top investment banks (Credit Suisse, Morgan Stanley) setting up Islamic operations, in competition with established players (HSBC, Citigroup) • Wide range of financial institutions (banks, commercial finance companies, funds) have bought Islamic acquisition financing paper (Ijara) • Investors’ appetite for sharia-compliant financing instruments has led to the growth of sukuk issuance • Islamic structures continue to be used extensively for real estate, as well as project and equipment finance

Comparative Analysis – Sukuk versus Conventional Bond and Bank Debt

Market Overview of Sukuks • The sukuk market has grown at a CAGR of over 100% since 2000 • Sukuk issues to date amount to $92 billion worldwide • While the majority of issues have come from the Middle East and Malaysia, there is an increasing interest from issuers in other jurisdictions CORPORATE VS. SOVEREIGN SUKUK ISSUANCES TOTAL SUKUK ISSUANCE WORLDWIDE 2000 – 10 Months 2007 US$mm US$mm Source: IFIS

Islamic Development Bank USD 400 million Hybrid Sukuk (66% Ijara, 31% Murabaha and 3% Al-Istisna’a) Examples of Sukuk Issues With Innovative Structures Convertible Sukuk Exchangable Sukuk Hybrid Sukuk Dubai Ports USD 3.5bn Khazanah USD 750 million Largest sukuk to date, first Sukuk convertible into equity upon an IPO. More than four times oversubscribed World’s first sharia-compliant exchangeable bond, exchangeable into shares of Teleko, Malaysian operator Sukuk Fund Acquisition Financing Murabaha and Ijara High-Yield sukuk Done for a number of Arcapita deals First sukuk fund to provide direct investment to sukuks, (75% in sukuks and 25% in sharia-compliant syndications)

Examples of Corporate and Sovereign Sukuk Issues National Central Cooling Company (Tabreed) USD 200 million Emirates USD 550 million Saudi Basic Industries Corporation USD 800 million Banks USD 1.1 billion East Cameron USD 166 million Corporates First listed sukuk on the LSE First airline sukuk First Saudi Arabia fully tradable sukuk Sukuk financed by 52 different institutions US gas company Malaysia USD 32 billion Pakistan USD 164 million State of Saxony-Anhalt EUR 100 million UK £ Sovereign Issuer of the first sovereign sukuk in the world ($600m) Water & Power development authority First state government in Germany & Europe to issue a sukuk To issue a sovereign sukuk in 2008

Arcapita Sukuk – Syndicate Members by Region 1 2 3 5 4 1 2 3 4 5

The Liquidity Issue • Although the market of quoted sukuk is expanding, it only represents 20% to 25% of entire sukuk market ($10 to $15 billion) • Dubai has been the main financial place for traded sukuks but the secondary market is quasi-inexistent • Most of the paper is being kept by buy-and-hold Islamic investors keen to put their cash to work in sharia-compliant investments, all the more they benefit from increased cash resources thanks to oil prices • There also has been a scarcity of sharia-compliant bonds so far compared to the growing investor base looking for sharia-compliant low risk products • Increased listings, outside the GCC states and in other currencies than the $, should increase the secondary market, such as Tabreed sukuk listed on the LSE

Infrastructure - Total US$ 76 billion Real Estate and Project Finance • An estimated US$ 115 billion of real estate and infrastructure projects have been financed or committed using Islamic structures since 2000 • At least US$ 10 billion of this total involve projects in non-Muslim countries, including the US, UK, China, India and France and an estimated $ 14 billion are outside the Middle East • These financings continue to be dominated by local banks but US and European banks have a growing presence

Arcapita has completed more than US$ 5.0 billion of buyouts in the US using traditional Ijara and Murabaha financing However, in Europe, significant tax and regulatory issues continue to constrain the development of the market. These include: Capital gains, transfer tax and VAT Stamp duty Financial assistance and corporate benefit The key difference is that Ijara is regarded as a financial lease in the US and therefore treated as a financing where no transfer of asset ownership risk takes place, and therefore sale and lease tax rules are disregarded The UK is so far the only country in the process of implementing legislative changes in order to address the specific issues relative to Islamic finance and facilitate the growth of the market Acquisition / LBO Financing

Contact Arcapita Arcapita Bank B.S.C.(c) Arcapita Inc. Arcapita Limited P.O. Box 1406ManamaKingdom of Bahrain Tel: +973 1721 8333Fax: +973 1721 7555 75 Fourteenth Street, 24th FloorAtlanta, GA 30309United States of America Tel: +1 404 920 9000Fax: +1 404 920 9001 15 Sloane Square, 2nd FloorLondon SW1W 8ERUnited Kingdom Tel: +44 207 824 5600 Fax: +44 207 824 5601 www.arcapita.com