Download

1 / 25

370 likes | 991 Views

Mergers, Acquisitions, and Corporate Control. VENTURE CAPITAL CONSULTANTS Course VCC / MCCI060107. Corporate Control. Corporate control: monitoring, supervising and directing a corporation or other business organization. Acquisitions (purchase of additional resources by business enterprise):

E N D

Mergers, Acquisitions, and Corporate Control VENTURE CAPITAL CONSULTANTS Course VCC / MCCI060107

Corporate Control Corporate control: monitoring, supervising and directing a corporation or other business organization • Acquisitions (purchase of additional resources by business enterprise): • Purchase of new assets • Purchase of assets from another company • Purchase of other business entity (merger) • Concentration of voting power (LBOs and MBOs) • Divestiture: transferring ownership of a business unit • Spin-off: creation of new corporation Changes in corporate control occur through:

Corporate Control Transactions Statutory mergers • Acquired firm is consolidated into acquiring firm with no further separate identity. • Acquired firm maintains its own former identity. • PepsiCo and Pizza Hut maintained their identities after merger in 1977. Subsidiary merger • Two or more firms combine into a new corporate identity. Consolidation • Leverage buyout (LBO): public shares of a firm are bought and taken private through use of debt. • Management buyout (MBO): an LBO initiated by the firm’s management “Going private” transactions

Resource Disintegration Divestiture: resources of a subsidiary or division are sold to another organization. Spin-off and split-off: a new company is created from a division or subsidiary. Equity carve-outs: sale of partial interest in a subsidiary Split-up: sale of all subsidiaries. Company ceases to exist Bust-up: takeover of a company that is subsequently split-up

Corporate Control Transactions • Buy enough shares on the open market to obtain controlling interest • Regulation in most developed countries prevents this form of acquisition. Open market purchases • Gain corporate control through consignment of other shareholders voting rights Proxy fights Tender offers • Open and public solicitation for shares Open market purchases, tender offers and proxy fights can be combined to launch a “surprise attack.”

Mergers by Business Concentration • Between former intra-industry competitors • Attempt to gain efficiencies of scale/scope and benefit from increased market power • Susceptible to antitrust scrutiny Horizontal mergers • Between former buyer and seller • Forward (Disney merger with Capital Cities/ABC) or backward (Texaco and Getty Oil merger in 1984) integration • Creates an integrated product chain Vertical mergers • Between unrelated firms • Creates a “portfolio” of businesses • Product extension mergers vs. pure conglomerate mergers • For example, merger between GM and EDS Conglomerate mergers

Transaction Characteristics Method of payment used to finance a transaction • Pure stock exchange merger: issuance of new shares of common stock in exchange for the target’s common stock • Mixed offerings: a combination of cash and securities Attitude of target management to a takeover attempt • Friendly deals vs. hostile transactions Accounting treatment used for recording a merger • Prior to June 30, 2001, two methods: pooling-of-interest and purchase methods • With the implementation of FASB Statements 141 and 142, one standard method of accounting for mergers

Merger and Intangible Assets Accounting • Target firm has 5 million shares at $10 per share. • Acquirer pays a 20% premium ($12 per share) to expand in the geographic area where target firm operates. • Transaction value 5 million shares x $12/share = $60 million. • Net asset value of target company is $45,000,000. Current assets $10,000,000 Restated fixed assets $65,000,000 Less liabilities $30,000,000 Net asset value $45,000,000 • Acquirer pays $15 million for intangible assets ($60 million - $45 million). Goodwill will remain on the balance sheet as long as the firm can demonstrate that it is fairly valued.

Returns to Target and Bidding Firm Shareholders Shareholders of target firm experience significant wealth gains in case of merger. Jensen and Ruback survey: average 29.1% premiums for tender offers and 15.9% for mergers On average, positive returns result for tender offers and zero returns for successful mergers. Negative trend in acquirer returns over time attributed to adoption of Williams Act.

Empirical Findings in Corporate Control Events • Shareholders gain higher returns in cash transactions than in stock transactions. • Signaling model: Equity offers signal that acquirer’s stock is overvalued. • Tax hypothesis: Target shareholders require capital gains tax premium for cash transactions. • Preemptive bidding hypothesis: premium for cash offers required to deter other potential bidders. Mode of payment Returns to other stakeholders • Significant wealth gains result for holders of convertible and nonconvertible bonds.

Value-Maximizing Motives for Mergers and Acquisitions Geographic (internal and international) expansion • Greenfield (internal) entry vs. external expansion • M & A is better alternative for time-critical expansion. • External expansion provides an easier approach to international expansion. • Joint ventures and strategic alliances give alternative access to foreign markets. Profits are shared. Synergy, market power, and strategic mergers • Operational, managerial and financial merger-related synergies • Eisner on Disney and Cap Cities/ABC merger: “1+1=4”

Value-Maximizing Motives for Mergers and Acquisitions Operational synergies • Economies of scale: • Merger may reduce or eliminate overlapping resources. • Economies of scope: • Involve activities that are possible only for certain company size • The launch of national advertising campaign • Economies of scale/scope most likely to be realized in horizontal mergers • Resource complementarities: • One company has expertise in R&D, the other in marketing. • Successful in both horizontal and vertical mergers

Value-Maximizing Motives for Mergers and Acquisitions Managerial synergies and market power • Managerial synergies are effective when management teams with different strengths combine. • Market power is a benefit often pursued in horizontal mergers. • Number of competitors in industry declines. Other strategic reasons for mergers • Product quality in vertical merger • Defensive consolidation in a mature or declining industry • Tax-considerations for the merger

Non-Value-Maximizing Motives Agency problems: management’s (disguised) personal interests are often drivers of mergers and acquisitions. • Dennis Mueller (1969) • Managerial compensation is often tied to corporation size Managerialism theory • Michael Jensen (1986) • Managers invest in projects with negative NPV to build corporate empires Free cash flow theory • Richard Roll (1986) • Acquirer’s management overestimate their capabilities and overpay for target company in belief they can run it more efficiently Hubris hypothesis

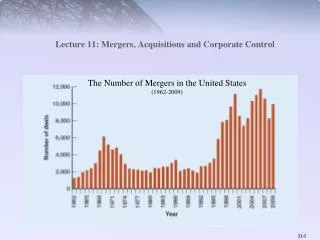

History of Merger Waves Five merger waves in the U.S. history Merger waves positively related to high economic growth Concentrated in industries undergoing changes Regulatory regime determines types of mergers in each wave. Usually ends with large declines in stock market values

History of Merger Waves • Period of “merging for monopoly” • Horizontal mergers possible due to lax regulatory environment • Ended with the stock market crash of 1904 First wave (1897-1904) • Period of “merging for oligopoly” • Antitrust laws from early 1900 made monopoly hard to achieve • Just like first wave: intent to create national brands • Ended with the 1929 crash Second wave (1916-1929) • Conglomerate merger wave • Celler-Kefauver Act of 1950 could be used against horizontal and vertical mergers. • Stock market decline of 1969 Third wave (1965-1969)

History of Merger Waves, cont. • Spurred by the lax regulatory environment of the time • Junk bond financing played a major role during this wave: LBOs and MBOs commonplace • Hostile “bust-ups” of conglomerates from previous wave • Ended with the fall of Drexel, Burnham, Lambert Fourth wave (1981-1989) • Friendly, stock-financed mergers • Relatively lax regulatory environment • Consolidation in non-manufacturing service sector • Explained by industry shock theory Fifth wave (1993 – 2001)

Not Concentrated Moderately Concentrated Highly Concentrated HHI Level 1000 1800 Determination of Anti-Competitiveness • Since 1982, both DOJ and FTC have used Herfindahl-Hirschman Index (HHI) to determine market concentration. • HHI = sum of squared market shares of all participants in a certain market (industry) • Elasticity tests (“5 percent rule”)is an alternative measure used to determine if merged firm has the power to control prices.

The Williams Act Enacted in 1968 for fuller disclosure and tender offers regulation Section 13-d must be filed within 10 days of acquiring 5% of shares of publicly traded companies. Section 14 regulates tender offer process for both acquirer and target. Section 14 provides structural rules and restrictions on the tender offer process in addition to disclosure requirements. Section 14-d-1 for acquirer and section 14-d-9 by target company

Insider Trading SEC rule 10-b-5 outlaws material misrepresentation of information for sale or purchase of securities. Rule 14-e-3 addresses trading on inside information in tender offers. The Insider Trading Sanctions Act, 1984 awards triple damages. Section 16 of Securities and Exchange Act establishes a monitoring facility for corporate insiders.

Merging firms may be integrated in a number of ways. Target shareholders almost always win, but acquirers’ return are mixed. Managers have either value-maximizing or non-value maximizing motives for pursuing mergers. Merger activity occurs in waves. Mergers, Acquisitions, and Corporate Control