Download

1 / 11

110 likes | 138 Views

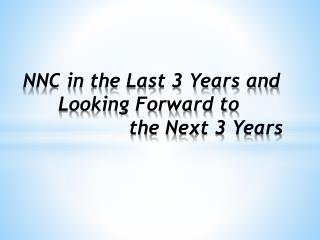

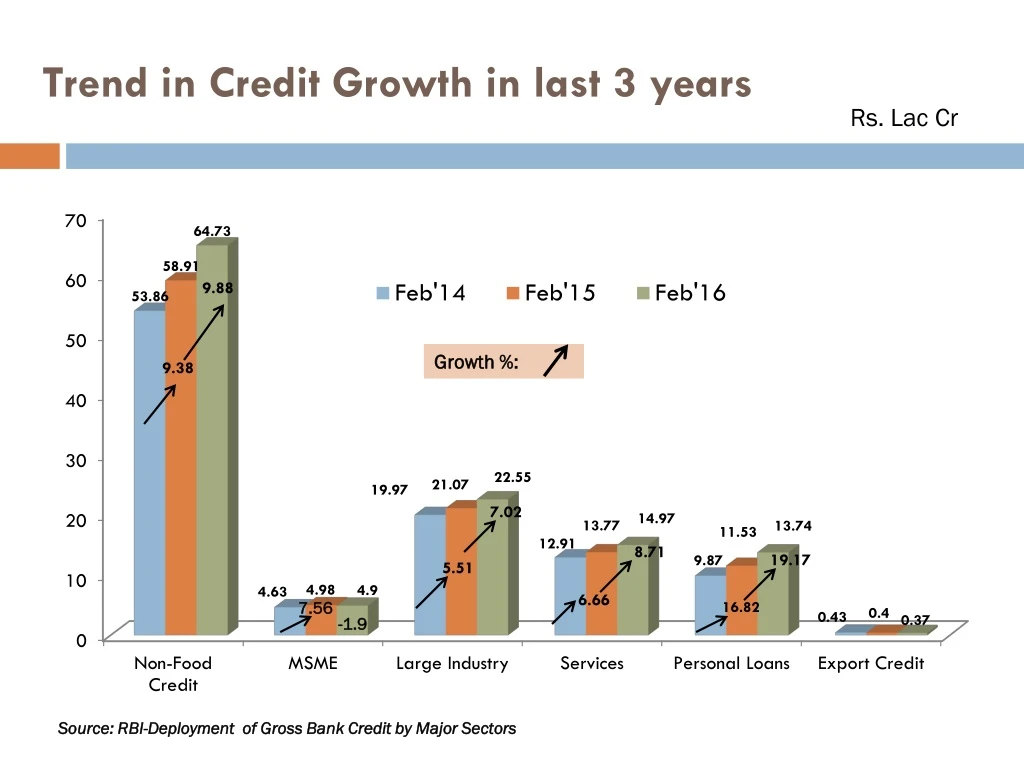

Trend in Credit Growth in last 3 years. Rs. Lac Cr. Growth %:. 7.56. -1.9. Source: RBI-Deployment of Gross Bank Credit by Major Sectors. How technology is changing SME financing.

E N D

Trend in Credit Growth in last 3 years Rs. Lac Cr Growth %: 7.56 -1.9 Source: RBI-Deployment of Gross Bank Credit by Major Sectors

How technology is changing SME financing • Technology playing critical role in entire loan lifecycle viz. origination, lead management, appraisal and sanction, EWS, supervision and monitoring • Supply chain financing EDFS, EVFS enabled by technology. • E commerce end to end credit process digitalised, decision within a few minutes • Asset based lending becoming very popular • Shift away from PBS to cash flow based financing. Technology to play critical role in verification of cash flows • Score cards based on data analytics and consumer behaviour for small value loans • Franchise financing emerging opportunity

How technology is changing SME financing • State of the art early warning systems • Digitalisation of inspection process. • Emergence of direct lending platforms

Scoring models in SME lending • SME Credit Card to provide loans for micro enterprises up to Rs. 1 million, to meet any kind of credit requirement including purchase of shop or furniture based on behavioral Scores • SME Smart Score based on financial Scores • Cluster Specific Packagebased on sectoral Scores • Cluster Specific Packagebased on region specific Scores • Rice Mill/ Dal Mill plus scheme to provide loans for acquisition of fixed assets and working capital needs for rice millers and dal millers based on activity specific Scores

New platform for financing of receivables & PSL Certificates TReDS • RBI has recently issued licenses to three entities for operating the Trade Receivable Discounting System (TReDS) • This would address a major issue faced by MSMEs i.e. timely realization of receivables. • Needs wholehearted support from all the major stakeholders, i.e. the large corporates, the PSUs and eventually, the Government enterprises. • Priority Sector Lending • Medium enterprises have been brought within the ambit of priority sector • Loans to medium enterprises in the manufacturing sector and those up to Rs. 10 crore in the service sector now qualify for priority sector classification. • The target for banks’ lending to micro enterprises has been progressively increased to 7 percent by March 2016 and 7.5 percent by March 2017 • PSL certificates becomes trade able

Peer-to-peer lending • Peer-to-peer lending, is the practice of lending money to individuals or businesses through online services that match lenders directly with borrowers. • Since the peer-to-peer lending companies offering these services operate entirely online, they can run with lower overhead and provide the service more cheaply than traditional financial institutions. • As a result, lenders often earn higher returns compared to savings and investment products offered by banks, while borrowers can borrow money at lower interest rates. • In India, peer-to-peer lending is currently unregulated. • Most P2P platforms are in nascent stages. • Several peer-to-peer lending services initiated operation and loan origination during 2012, neogrowth.in, smecorner.com, capital float.com are some examples

Growth Drivers • The Government of India has launched Rs.10000 crstartup fund in Union budget 2014-15 • Out of above, Rs 2,000 crore has been channelised through the India Aspiration Fund. (Managed by SIDBI) • In order to boost innovative product companies, Government has launched ‘Bank of Ideas and Innovations’ program. • RBI’s in-principle approvals for 10 Small Finance Banks (SFBs).

Growth Drivers • Government backed ‘PradhanMantri Micro Units Development and Refinance Agency Limited (MUDRA)’ starts with an initial corpus of Rs. 20,000 crore to extend benefits to around 10 lakhs SMEs. • State specific programs to encourage small businesses (Kerala State Self Entrepreneur Development Mission (KSSEDM), Maharashtra Centre for Entrepreneurship Development, Rajasthan Startup Fest, etc.) • Mandates to all Central Government Ministries/ Departments and PSUs to procure 20% of their annual procurements from MSMESs • UdyogAadhaar, Start-up India, Make in India and steps for improving “Ease of Doing Business”

Innovation to drive growth and productivity gains • ‘SBI InCube’, a dedicated branch at Bangalore, for Start-ups. • SBI InCube would offer advisory services to the entrepreneurs under one roof • Venture capital/angle funding in the initial years. Bank lending on maturity

What is needed ? • Rehabilitation fund for sick but viable units • Relook needed for asset classification Of SMEs • Stricter penalties for delayed payments to SME by Govt Depts and Corporates • Popularise schemes of Ministry of MSME. • Investment in technology and people by the banks. • Securitisation market needs to be given a boost • Faster resolution of Stressed Assets