Download

1 / 31

310 likes | 408 Views

Workshop overview on MTEF implementation for poverty reduction strategies, focusing on budgeting, policy priority alignment, and resource allocation in Nigeria.

E N D

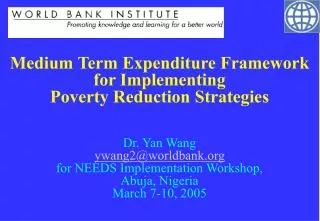

Medium Term Expenditure Framework for Implementing Poverty Reduction StrategiesDr. Yan Wangywang2@worldbank.orgfor NEEDS Implementation Workshop, Abuja, NigeriaMarch 7-10, 2005

“A budget is much more than a collection of numbers. A budget is a reflection of a nation’s priorities, its needs, and its promise.” • Alexander Hamilton

Overview Outline • Introduction of MTEF • International experiences: African countries • Pre-conditions of MTEF and Issues To Be Addressed • More capacity building /training needed • Implementation Strategy for Nigeria: to be discussed

What is a MTEF? • A tool for linking policy, planning & budgeting over a medium-term ( 3 years) at the Government-wide level; • It consists of a top-down resource envelope & a bottom-up estimation of the current & medium-term costs of existing policies;

What is a MTEF? • Matching of policy priorities and budget in the context of the annual budget process; and • Involves rolling over this exercise every year by incorporating policy changes.

Objectives of MTEF • Improved macroeconomic balance esp. fiscal discipline • Integrating policy priorities (identified in NEEDS) into annual budget: Resources allocated to priorities – to ensure credible policy. • Better inter- and intra-sectoral resource allocation • Greater budgetary predictability for line ministries by providing mid-term perspective (3-5 yrs) • Enhancing operating efficiency: high quality, low cost • Greater accountability for public expenditure

What can it do? If successfully applied, MTEF can • Improve macroeconomic balance by developing a multi-year resource framework (expenditure & revenue); • Assist in improving resource allocation between & across sectors; • Improve predictability of funding for line ministries.

Medium Term Expenditure Framework Setting Fiscal Targets Allocation of Resources to Strategic Priorities Economic and Fiscal Update Fiscal Framework Statement Report Budget Policy Statement Corporate Plans Central Agencies Cabinet Minister

MTEF Process (simplified) Updated cost estimate of existing policy/program Macro-economic forecasting Fiscal Target Total Expenditure Setting For multi years Sectoral Ceiling Setting for multi years Annual Budget Formulation New sectoral demand for t+2 (priority/cost) Sectoral Budget Preparation

Experiences in Africa Source: Houerou and Taliercio 2002

Lessons from International Experiences • Integration of multi-year planning with annual budget - MTEF and annual budgeting is one process • Realistic macroeconomic forecasting; honest revenue projection • Separation of total budget from detailed program • Clarification of new roles of MOF/line ministries • Capacity building and incentives for MOF/line ministries • Development of feedback mechanism

Preliminary lessons from MTEF experience • The importance of initial PEM conditions. The MTEF is a complement to – not a substitute for -- basic budgetary management reform: • Budget comprehensiveness –including donors’; off-budget items, • Classification – integrate capital and recurrent budgets; • Budget execution. Timely reporting (publication) • Timely audit (and publication) underpinned by sanctions against misappropriations of resources. 2. Sequencing and phasing of the MTEF reform: • Phased vertically (macro, sector, service delivery) • Piloted horizontally (across sectors) • Timing and elements tailored to capacity

An ideal country case • Consensus on priorities built through the participatory process, built on ongoing programs. Lower priority activities dropped/scaled down • Comprehensive“Critical to the success of the PRSP is the need to implement only the PRSP” • PRSP-budget link is central: Budget preparation & scrutiny by MOF to ensure that line agency budget submissions are consistent with the PRSP • Transition phase for donor activities: • Existing projects “grand fathered” • All new projects must fit within PRSP priorities • Annual review vehicles, envisaged as country’s central policy review process • PER – expenditures & impacts • PRSP review (annual progress report) complemented by a comprehensive review every three years

Need for patience and perseverance: • Prioritisation and costing will likely need continuing improvement in the context of implementation and monitoring of the first PRSP • Prioritization and costing will only be possible if the PRSP is linked to the budget process • MTEF can be valuable: • The MTEF should be integrated with existing budget processes • the institutional arrangements for the MTEF & PRSP should be consistent in both exercises, and recognize the central role of Ministry of Finance • Phasing-in of MTEF, by sector and functions, needed

Pre-conditions for Implementing MTEF • There may be different views on pre-conditions. This is one view: We need • Strong political support • MOF /NPC’s willingness/commitment - clear understanding of MTEF and incentives - strong leadership within MOF • Line ministries’ compliance - proper incentives: discretion and policy prioritization • Capacity building for MOF and line ministries

How to Build Macro Forecasting Capacity in MOF? • MOF plays a key role in macro forecasting for fiscal policy purpose - strong need to increase institutional capacity - consideration of social/political factors • Coordination mechanism with MoF, CB of Nigeria, public/private research institutes • Formula for conservative forecasting for budgeting - in Canada, add 0.5-1% to forecasted interest rates

How/Who Decide Total Budget & Sectoral Ceiling? (1) • Two stage approach: total envelope setting sectoral allocation • Total budget setting - macro/fiscal targets,social/political demands - new sectoral demands and updated costs estimates • Sectoral allocation - national policy priority - determined within total budget : zero-sum game

How/Who Decide Total Budget & Sectoral Ceiling? (2) • Final draft is prepared by MOF in consultation with the President • Send draft to cabinet meeting for consensus building - sectoral ceiling is not revealed until total decided - in Sweden, 2-3 days’ cabinet retreat • In case of disagreement, final decision is made by President “It is President who holds ultimate responsibility of budget”

Use of budget margin • Serves as a Bumper for 1) macro forecasting deviations 2) ‘inevitable’‘unexpected’ demand 3) President’s new initiatives under exceptional situations • Budget margin = total envelope – aggregate of sectoral ceiling * in Sweden, 3.33% in 1997, and 0.05% in 2003 • Unused margin to be used to accelerate debt payment

How much sectoral ceiling is binding? • In principle, no breach is allowed • Amendment allowed for substantial macroeconomic change (cost estimate basis) • Exception is explicitly identified ex-ante with MOF’s consent, through cabinet meeting 1) ministry makes trade-off within sectoral cap 2) trade-off between ministries within total budget 3) budget margin to be used

How Much Discretion Allowed for Line Ministries? • Sectoral priority discussed and agreed between MOF and line ministries • Line ministries prepare own budget request within provided ceiling & priority line • monitoring and coordination mechanism • Incentive for efficient spending - allowed to carry-over certain % of savings to ministries

How to Build Incentive System? For MOF /NPC ? - Shift to higher level, macro decision-making by integrating national policy priorities with budgeting - Close interaction with President For Line Ministries - Budgetary Discretion to prioritize policies - Flexibility in implementing policy and executing budget

How to Ensure Line Ministries’ Accountability? (1) • Ministers hold ultimate responsibility over performance • MOF /NPC plays a role as a watchdog • Performance management serves as a feedback mechanism for increased discretion • Linking budgeting with accounting system • Information system needs to be integrated between MOF, NPC, and line ministries, and Office of Statistics

Capacity Building is needed on all these aspects: More training can be provided • How to Improve Budget Structure and Scope ? • How to improve the incentive system • How to make line ministries accountable for delivery? • Performance Management System • - utilized as information gathering and analysis - long-term, phased approach is desirable - need to adopt realistic short-term approach - pilot projects to introduce output-based indicator development and performance evaluation system - expand into all programs with outcome indicators

Implementation Strategy for NigeriaSome suggestions and followed by discussion by Victoria Kwakwa

Creating Enabling Environment for MTEF • Use MTEF as an instrument to alter status quo • Fiscal reform along with Public Sector reform • Leadership and Capacity Building - champion of reform and creating a core team - motivating self-development and capacity building • Performance oriented environment in government - e.g., regulation-free organizations

Implementation Strategy [a suggestion] • Stage I : top-down approach - macroeconomic forecasting and fiscal target setting - setting total and sectoral ceiling prior to program details • Stage II : bottom-up approach (Gradual Approach) - line ministries’ discretion within sectoral ceiling and priority - allowing discretion on operating costs • Stage III :incorporation with performance management - well-functioning information system - performance information reflected in budgetary decision

Strategies for Nigeria • To be discussed by Victoria Kwakwa and representatives from the government