Download

1 / 17

170 likes | 191 Views

This presentation provides an overview of the design and performance of the Swedish Second Pillar pension system. It explores the transformation of the pension scheme, the role of the Premium Pension Authority, the regulation and structure of private funds, and the preliminary results of the system. The presentation also discusses the costs of operating the second pillar and highlights potential issues and considerations for other countries.

E N D

THE SWEDISH SECOND PILLAR Design, Performance, Outstanding Issues, and Applicability to Other Countries

Background • Pension reform legislated in 1994 • Transforms PAYG DB Scheme into: • NDC (PAYG) (16% contribution) • FDC (FF) (2.5% contribution) • Makes occupational funds mandatory, converts them from DB to DC (3.5% contribution) • Therefore, second pillar has 2 components and total contribution of 6% • Presentation focuses on first part of second pillar

Background • Reform only implemented in 2000 • Need to prepare IT systems, raise information from 1960 (NDC capital) • Individual choices introduced in 2000, supported by: • Local offices (SSSA) • Call center • Internet (personal account, providing information on the system, pension projection model)

Design of Second Pillar • Designed to minimize costs, especially in view of small contribution of 2.5% • Achievement of economies of scale and competition simultaneously through: (i) single basic service provider; (ii) blind accounts/blind quotation system; (iii) several asset managers; (iv) system of fee rebates

Design of Second Pillar • The single basic provider: The Premium Pension Authority (PPM), utilizing the existing structures of the SSSA and the Tax Authority • Functions of PPM: • Organizes collection of contribution through SSSA and Tax Authority • Manages accounts, information • Contracts asset management from private funds on behalf of members, clears all flows of funds • Benefit payments (monopoly annuity provider)

Regulation, Structure, Performanceof Private Funds • All asset management companies licensed in the EU are allowed to operate • By 2004, 75 companies licensed, managing 650 funds, 4.4 million participants • PPM is the legal representative of all participants vis-à-vis these funds • Clients can choose up to 5 funds • Non-choosers allocated to a default public fund • In the first year, substantial information provided by PPM and marketing expenses by private funds

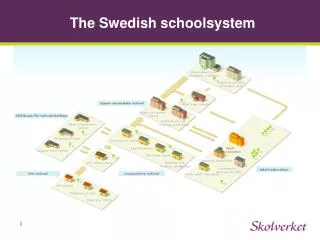

Preliminary results • Assets grew to 5% of GDP in 2004 • Large base, but small contribution and poor returns in 2001, 2002 • Large share of participants making active choices in the first year, declining sharply in following years, average choice: 3.4 funds • Strong preference for equity funds: 72% of active choosers chose only equities • Default fund has large share of equities (80% equities, 10% indexed bonds, 4% hedge funds)

Percent of New Participants Making an “Active” Investment Choice

Costs of Operating Second Pillar Three Basic Components • PPM’s Own Operating Costs • Internal management of individual accounts, information to members • Reimbursements to SSSA • Revenue collection, sharing of annual individual statements, sharing of local offices (NDC, FDC) • Payment of Private Fund Fees, Net of Rebate • Very low marketing expenses • Rebate system based on size of assets, reduces fees further

Fee Rebate System • Gross charges apply to all customers, whether in second or not • However, to operate in second pillar funds have to accept additional rules, especially a fee rebate system • Rebate increases (reducing net fees) with the volume of second pillar assets managed • Rebate is credited in the individual accounts

Issues for Other Countries • Attractive option, especially for small countries • Strong aspects: combines economies of scale and competition, leading to small fees • Possible weaknesses/issues include: • Excessive number of funds • Investment regime without risk limits • Regulation of basic provider • Governance issues for public default fund • Monopoly on the payout phase • Most of these potential weaknesses can be addressed