Download

1 / 4

40 likes | 67 Views

The general beneficiary clause of the trusts deed is very wide, basically including almost anyone related by blood or marriage to the Primary Beneficiaries, as well as trusts and companies in which they may have an interest. Call 095994 45568. https://bit.ly/2KZd3BR

E N D

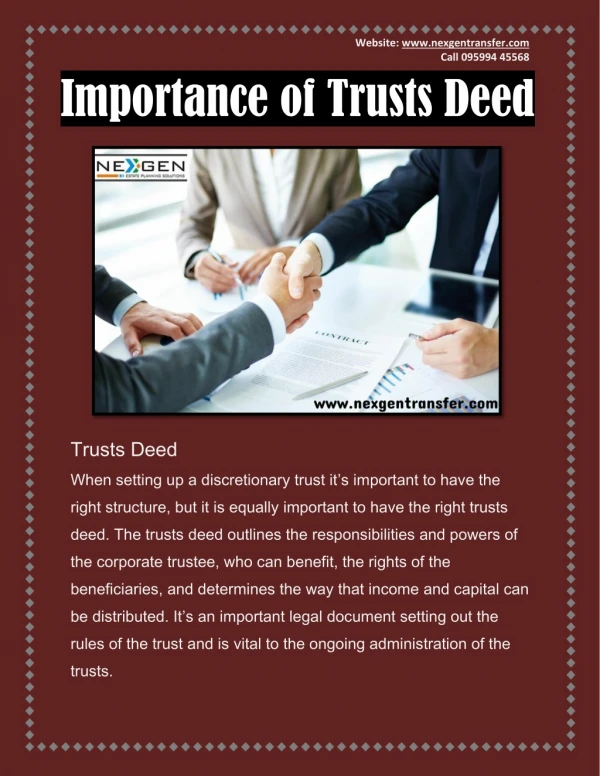

Website: www.nexgentransfer.com Call 095994 45568 Importance of Trusts Deed Trusts Deed When setting up a discretionary trust it’s important to have the right structure, but it is equally important to have the right trusts deed. The trusts deed outlines the responsibilities and powers of the corporate trustee, who can benefit, the rights of the beneficiaries, and determines the way that income and capital can be distributed. It’s an important legal document setting out the rules of the trust and is vital to the ongoing administration of the trusts.

Website: www.nexgentransfer.com Call 095994 45568 Corporate Trustee T The he g gener bas basi ic cal all ly y i inc th the Pri e Prima w whi hic ch they h they may di dis stribut tribute the i i inc ncome ome wi Pri Prim mary B ary Ben e trus ated by rusts and c no determi termin nati r a partic particul ular ar i inc ual di dis stributi tribution am re. When th en the t up up (w eff effec aft after t c comm omme enc c cor orpor r the trust i rust is s i in So ass sets ets of t of the tr he trus ot make e a det a determi ermina nati tion, they ry Benefi enefic ci iaries aries ( (unl unles ess s a any e thei eir sha r share wil re will l be di be dis stribu tributed none of ne of them a them are ali re aliv ve, eq e, equal uall ly y to t trustee rustee’ ’s s pow powers hav ers have e been been dra al all lowi owing ng the t the trustee rustee to ac to act as t as i if i f it i t is s the of of the as the ass sets ets of of the the trust f trust fund, und, and s eneral al benefi benefic ci iary c ncl ludi uding mary B ry Benefi enefic ci iaries may hav have e an i e the inc ncom wil ll l be hel be held o enefi efic ci ia aries ary cl laus most any t anyone aries, as , as w an inte nterest. If ome of th e of the tr e trus d on tr n trus usts ts for eq ries aged aged 18 o ause of th e of the tr one r rel elated wel ell l as as t trusts rest. If no de usts ts fo for a for equal 18 or mo r more. Wh ery wid de, r marr rri iage anies es i in n on i is s made made to ncom ome y e year, on amongs ongst th e trusts rusts i is s wound (whi hic ch wi h wil ll l ecti tiv vel ely y be 80 y be 80 yea er th he t e trust rust nces es, , unl porate t ate trustee rustee n South A uth Aus ust trali ust fund t fund as as i it thi t think on, they wi wil ll l be be di ny of the of them hav m have e di died, i ted equal equall ly y to thei to their chi to th the gen e general b eral benefi enefic ci iaries drafted fted as as bro broadl adly y as as pos the s sol ole and e and bene and sh houl ould i d inc ncl lude mo ude mos st s usts ts deed deed i is s v very wi by bl blood o ood or ma and comp ompani ation e, ng al almos age to to to the ear, the t the e wound ears rs unles ess s the the dec deci ides t trustee rustee c can an and, i d, if i f it does th the Pri e Prima c cas ase th no des t to wi o wind an di dis stri tribu t does n not mak mary B nd i it u t up ea p earli rlier o bute the te the as er or the t ralia) th a) the e nks s fi fit t dis stributed tributed to ed, in w n whi hic ch h r chil ldren dren, or aries). ). The poss si ibl ble, al e, als so o benefi fic ci ial al owner t si ituati tuatio ons to , or, i , if f The owner ns

Website: www.nexgentransfer.com Call 095994 45568 th that a t at a trustee no notorious torious f for may may s sti til ll l i ins to to ac act und t under th th the i e inv nves estment o s si imi mil lar pr ar prope th they ey retain retain thei tax taxe ed at a d at adul w when th hen there ere i is s mo ag agree reement. I ment. If ther dec deci is si ions ons unani p provi rovide oth de other erwi th they ey c can an’ ’t reach rustee wi or requiri nsi is st on thi t on this s des er the de e deed). tment of f p prope operty) to rty) to be di their p r prefe dult rates) t rates). Th mor re tha f there i unanimo mous wis se e), an t reach an an agr wil ll l e en nc counte requirin ng v ounter ( g very s ery spec despi pite te the tr ed). Th The trust e trust de roperty r rty rec be dis stribut tributed to referential rential tax . There is ere is a e than one n one trustee e is s more more than usl ly y (unles (unless s t the ), and the d there is agreeme eement. r (al althoug though not peci ifi fic c pow the trus deed al ecei eiv ve ed f d from ed to mi tax s stat tatus a di dis sput trustee and t than one one appoi he deed deed has re is a di a dis sput nt. h note that e that bank powers to ers to be i ustee h tee hav avi ing v ed all lows ows i inc rom a dec a deceas minor nor benefi benefic ci ia aries us (i.e. f (i.e. for th or the i pute resol e resolv vi ing mec and they hey c can appoint ntor, or, they has be been v pute resol e resolv vi ing m banks s a are be ins nse erted, ng very ery broa ncome ome deriv eased ed es ries s suc e inc ncome t ng mech hani an’ ’t t reach a reach an n they mus must m en va aried to ried to ng mec re rted, and broad po d power derived f ed from estate tate (and uch that h that ome to be o be anis sm m and wer rom (and t mak ake e echani hanis sm i m if f Will Format If the trustee received a testamentary gift (i.e., under the will of a deceased person) and there may be a problem with a technical

Website: www.nexgentransfer.com Call 095994 45568 legal rule known as “the rule against the delegation of testamentary power” (or any other such legal rule or law) then that gift is considered to be held on trust for the beneficiaries existing at the time the trustee receives the gift. New beneficiaries can be added but if any such technical rules apply, they cannot share in that gift. It depends upon the will format. Will format is the main thing for the trusts. Website: www.nexgentransfer.com Call 095994 45568 Thank You