Effective Cash Forecasting Strategies for Business Success

80 likes | 178 Views

Learn the importance of short-term cash forecasts and how to develop monthly cash budgets. Understand the differences between daily and monthly cash forecasting, as well as the methods used for forecasting cash flows. Explore forecasting philosophy, parameters, and tools to optimize your financial planning.

Effective Cash Forecasting Strategies for Business Success

E N D

Presentation Transcript

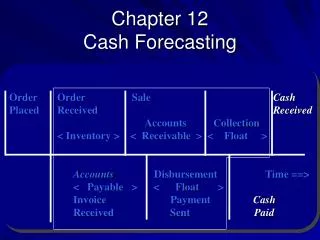

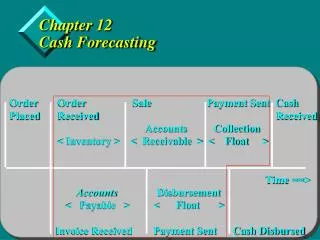

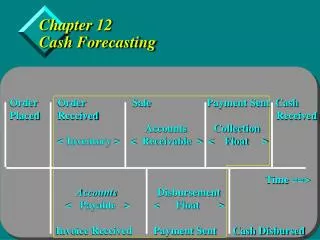

Chapter 12Cash Forecasting • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • AccountsDisbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

Learning Objectives • Explain importance of short-term cash forecasts. • Indicate why the monthly cash budget is important to top management, and specify the two objectives for its development. • Indicate how daily cash forecasting differs from monthly forecasting. • Explain the receipts and disbursements, pro forma balance sheet, and distribution methods of cash forecasting.

Forecasting Monthly Cash Flows • Importance to top management • Monthly cash forecast objectives • Forecasting philosophy • Forecast parameters • Statistical tools

Forecasting Philosophy • Number and type of forecasts • Expenditure on forecasts • External versus internal forecasts • Quantitative versus judgmental forecasting

Forecast Parameters • Forecast horizon • Variable identification • Modeling the cash flow sequence • Format of the receipts and disbursement forecast • Interpreting the receipts and disbursement forecast • Developing the receipts and disbursement forecast • Modified accrual method • Pro forma balance sheet method • Model estimation • Model validation

Forecasting Daily Cash Flows • Horizon • Variable identification • Modeling the cash flow sequence • Structuring the daily cash forecast • Distribution method • Model estimation • Model validation

The Distribution Method • Using the method for disbursements • Using the method for collections • Example • Final comments

Summary • The chapter began with a discussion of the philosophy and environment within which cash forecasts are made. • The value of forecasts is to borrow less or extend investment maturities. • The two major cash forecasting time intervals (monthly and daily) were presented and the processes for variable identification, modeling the cash flow sequence, model estimation, and model validation discussed.