Download

1 / 3

0 likes | 9 Views

Charge creation in finance happens when a lender takes an asset, such as property or a vehicle, as security for a loan. This ensures that if the borrower doesnu2019t repay the loan, the lender can sell the asset to recover the money. This process helps both borrowers and lenders, as it provides security to the lender and may help the borrower get a loan more easily.<br> <br>

E N D

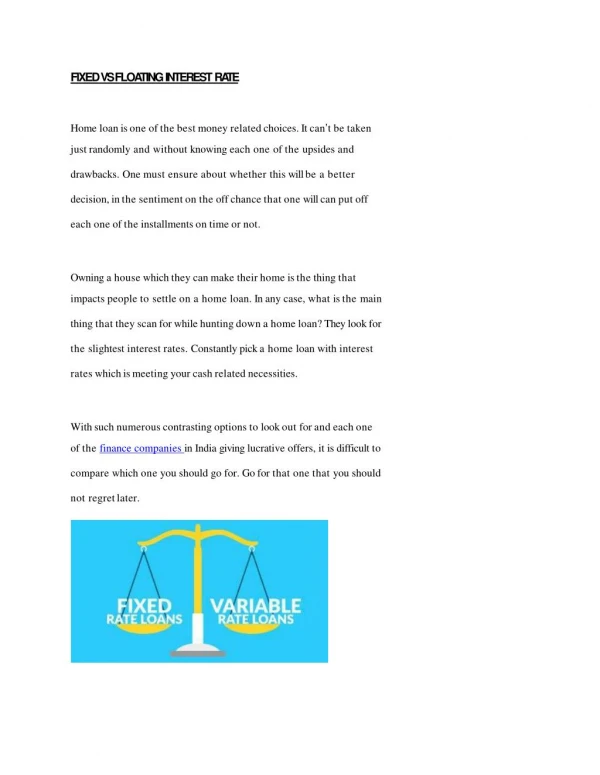

Charge Creation in Finance: A Detailed Overview of Fixed and Floating Charges Charge creation in finance happens when a lender takes an asset, such as property or a vehicle, as security for a loan. This ensures that if the borrower doesn’t repay the loan, the lender can sell the asset to recover the money. This process helps both borrowers and lenders, as it provides security to the lender and may help the borrower get a loan more easily. What is Charge Creation? Charge creation happens when a lender takes something valuable, such as a house or a car, as security for a loan. This way, if the borrower doesn’t pay back the loan, the lender can sell the asset and recover the money. The charge is like a promise from the borrower that the lender will get paid one way or another. There are two main types of charges in finance: fixed charges and floating charge. Each works differently to protect the lender. Types of Charges in Finance 1. Fixed Charge A fixed charge is attached to a specific item, such as a building, vehicle, or machinery. The borrower can’t sell or transfer that item without permission from the lender until the loan is fully paid off.

2. Floating Charge A floating charge is different because it doesn’t attach to one single item. Instead, it covers assets that change often, like inventory or stock. The borrower can freely use or sell these assets in day-to-day business until the lender decides to "fix" the charge if there is a problem with the loan. How Does Charge Creation Work Legally? Charge creation is guided by laws that protect both the borrower and lender. The lender usually creates a legal document called a loan agreement or charge deed, which sets out the terms of the charge. This document ensures both parties understand their rights and responsibilities. Registering Charges In many countries, charges must be registered with government authorities to be legally valid. For example, in the UK, companies must register their charges with Companies House within a certain time after the charge is created. If the charge isn’t registered, the lender could lose their right to claim the asset. Enforcing the Charge When a borrower fails to repay the loan, the lender can enforce the charge by taking possession of or selling the asset. Where is Charge Creation Used? Charge creation is common in many financial situations, including:

Mortgages: A mortgage is a type of fixed charge where the lender has a claim on a borrower’s house or property. Business Loans: Companies often create charges over assets like machinery or stock to secure loans for their business. Debentures: These are documents that create both fixed and floating charges over a company’s assets, giving the lender security over both specific and changing assets. Conclusion Charge creation in finance helps both lenders and borrowers. For lenders, it reduces the risk of losing money if the borrower doesn’t repay the loan. For borrowers, it can help them get credit more easily. By understanding how charge creation works, you can see why it is such an important part of many financial agreements.