Download

1 / 13

130 likes | 299 Views

The Federal Reserve and Monetary Policy. The Demand for Money and the Quantity Equation The quantity of money and the rate of interest Reducing the interest rate increases investment, and therefore (with a multiplier effect) GDP. The connections don’t always work perfectly in practice:

E N D

The Federal Reserve and Monetary Policy • The Demand for Money and the Quantity Equation • The quantity of money and the rate of interest • Reducing the interest rate increases investment, and therefore (with a multiplier effect) GDP. • The connections don’t always work perfectly in practice: • real/nominal rates and the Fisher effect • short term (Federal Funds) and long term (AAA and BAA bonds) • importance of expectations for investment decisions • Potential conflicting goals: GDP gap and inflation • The Taylor Rule and the Fed’s policy reaction function.

The Quantity Equation and the Demand for Money • MV = PY(money * velocity = GDPDEF * GDP) • Interest rates are the opportunity cost of holding money; so people will hold LESS money at HIGHER interest rates. • This means that velocity will INCREASE at higher interest rates -- money will change hands more rapidly. • Let V = 0.5 R for a numeric example; the result is: • Md = 2 PY / R, and since M.demand = M.supply, • Fed can change the money supply to set a target interest rate: R = 2 PY / Ms

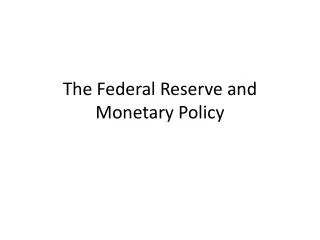

Fed control of interest rates • The Federal Reserve: • TARGETS the Federal Funds rate (overnight bank loans) • OPERATES in the Treasury Bill market • Controls both those rates CLOSELY. • However, those rates are SHORT TERM, SAFE, NOMINAL interest rates, and more important for the level of investment are: • LONG TERM, RISKY, REAL rates -- • the rates on corporate bonds such as Moody’s AAA or BAA bonds adjusted for inflation

Fed Funds Rate and Treasury Bill (6 month) rate

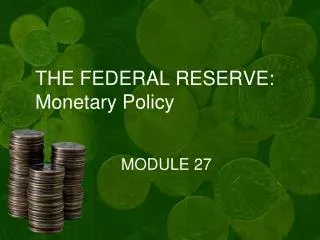

The Federal Reserve influences, but does not control, real long term interest rates (example: BAA bonds) The time series graph shows several cases in which the Fed cut short-run rates without much immediate response by long-run interest rates. Note: 1972.1 and 1977.1 and 1993.4 and 2001.3 -- the Fed cut rates to fight recessions, and real BAA rates did NOT follow. The scatterplot shows low real rates in the 1970s despite high Federal Funds rates; and high real rates in the 1980s despite cuts in the Federal Funds rates.

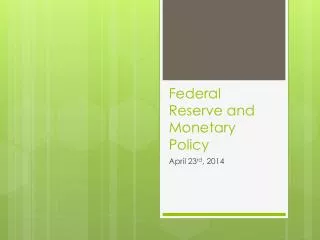

Investment is influenced by, but NOT determined by, real long term interest rate. • The next scatterplot shows investment as a percentage of GDP against real, long term interest rates. • Note especially: • In normal times, the interest rate does influence investment: see the late 70s and early 80s data points, during reasonably stable economic times. • When expectations of future profit turn down, the investment relation shifts back: note the data points for 1982 and 1983, when despite lower interest rates, investment fell sharply -- as the economy moved into a recession, businesses refused to invest whatever the interest rate.

Investment as a share of GDP and interest rates: not an unchanging relationship.

The Fisher Effect: the Dilemma of Monetary Policy • Real rates = nominal rates - inflation • To preserve the value of interest payments, lenders will tend to set nominal rates = real rate + inflation • The Fed lowers interest rates by expanding the money supply. • But the long run effect of continuing to expand the money supply will be inflation. • And inflation leads to higher interest rates • The Fisher relation is loose enough to permit temporary impact of monetary policy, but it is there in the long run.

Two policy targets, one policy instrument • Target # 1 = GDP gap -- output below potential leads to unemployment; which Fed would like to counter • Target # 2 = inflation -- reduction of inflation is also a desirable policy goal. • Policy instrument -- change in the Federal Funds rate. Cutting the Fed Funds rate might stimulate investment, but it might also increase inflation • Taylor Rule (John B. Taylor) describes the Fed’s reaction function R = 1.0 - 0.5 YGAP + 0.5 INFL • R = Real rate of interest • YGAP = (Potential GDP - Actual GDP) / Potential GDP given a positive (recessionary) YGAP, cut interest rates. • INFL = Inflation rate. As inflation increases, increase real rate of interest.