Download

1 / 44

440 likes | 443 Views

Learn about the three major credit monitoring companies and discover effective saving techniques to avoid relying on credit for purchases. Find out how to quickly obtain $300 and increase your net worth. Understand the importance of saving, paying off debts, and making non-cash payments. Explore credit vocabulary, loan basics, and the components of a credit score.

E N D

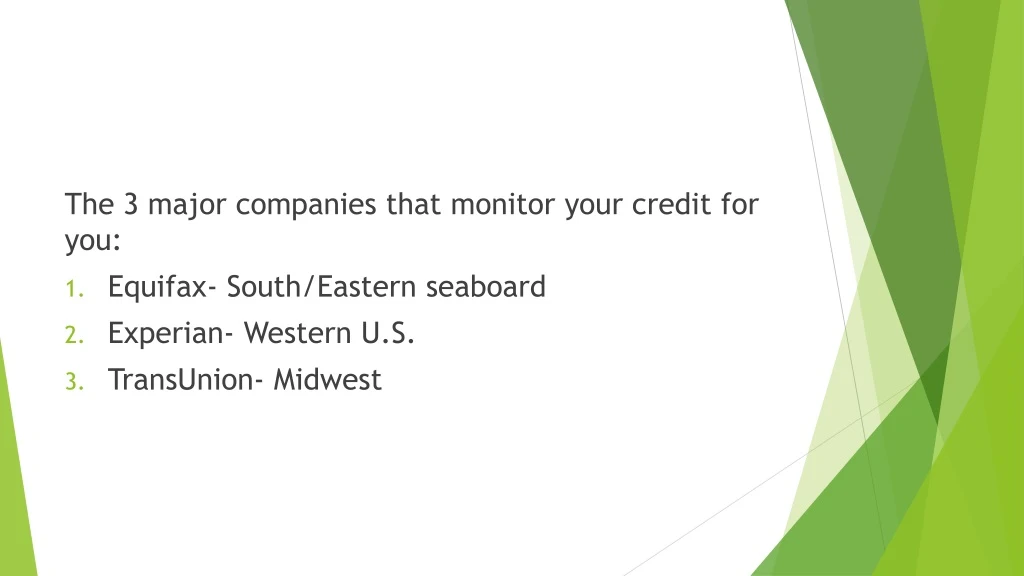

The 3 major companies that monitor your credit for you: • Equifax- South/Eastern seaboard • Experian- Western U.S. • TransUnion- Midwest

Instead of using credit- how do you go about making purchases? Learn to save first: • Emergency fund-unexpected events • Big Purchases • Wealth Building

How can I get my $300 quickly? • Allowance- if you get one then save it. • Hold a yard sale- sell stuff you don’t need. • Become an entrepreneur- start a business. • Part time job- work for someone else’s business. • Talk with your parents- negotiate with them. • Use your skills- what skill set do you have that you can market?

How can you increase your net worth? • Increase your savings • Increase your investments • Reduce your expenses • Reduce your debts

5 Reasons for Saving • Get an Emergency fund- try $300.00 to begin with. • As you get older than you should increase it to 3-6 months worth of expenses. • It is for EMERGENCIES ONLY! • Keep it separate from your regular money.

Get out of debt- don’t take on any new debt either. • Pay off your bills ASAP • TRIAGE your debts- pay the biggest ones off first. • Continue this till all debts are paid.

Pay cash for everything- the pain of watching money leave your wallet. • Avoid the credit card- emergency only • The debit card today is much like a credit card- you forget about the pain of $$$ leaving. • A sinking fund- pay cash

Pay for college • Don’t take out student loans • Scholarships, grants, and college jobs. • Average college student graduates with roughly $30,000 in student loan debt.

Build wealth • By staying out of debt you build net worth. • Add your assets (items of value that you own). • Subtract your liabilities (money or debts you owe), • Net Worth= assets minus liabilities.

How have non-cash payments changed the way people do business? Changed the way people do banking? • Some stats to consider:

Categories of Wealth • Liquid assets- this is any money that you have in cash, checking, or savings. • Real Estate- market value determines this. *Hard to convert to cash • Possessions- anything of value that you own. • Investment assets- would include retirement accounts (401K) and securities (stocks, bonds, mutual funds, etc.)

Credit Terminologyhttps://www.youtube.com/watch?v=GLDO7o1yLOw • Credit Report- summary of loan and bill payments kept by a credit bureau. (activity remains for 7 years; 10 years if you go through bankruptcy) • used by financial institutions and other potential creditors to determine the likelihood that future debt will be repaid. • Lenders, insurers, and employers use information along with your credit score to set loan and insurance rates or review job applications.

Credit Bureau- an organization that compiles credit information on individuals. • Makes the information available to companies for a fee. • Equifax, Experian, and TransUnion are the 3 major ones. (there are minor ones but most businesses use these 3)

Credit Score- your financial GPA (it is a measure of how you handle your financial obligations) • It is a snapshot of your level of risk to a lender at a specific point in time. • A credit score is NOT on your credit report. • When you borrow money you are given a FICO credit score (Fair Issac Corporation) • A perfect score from FICO is 850

LOAN BASICS • Annual Percentage Rate (APR): the interest rate for the whole year as applied on a loan, credit, mortgage, ect.. * Nominal APR- simple interest rate for a year. * Effective APR- the fee(s)+ compound interest rate calculated over a year. • Your terms of credit are contained in the Shumer box.

Collateralized loan: something of value that a borrower lets the lender claim if a loan is not repaid. • Consumer Credit Counseling Services: a nonprofit organization that offers counseling to those that have serious debt problems.

Installment credit: a type of closed credit that requires equal payments. (car loans) • Revolving credit: a type of open credit agreement that allows consumers to pay off all or part of an outstanding balance on a loan or credit card. (credit card) • Finance charge: the total amount that you pay to use credit. (principal+interest= Finance charge)

Lien: a legal claim one person has upon the property of another person to secure the payment of a debt. • Garnishment: a legal process that allows part of your paycheck to be withheld for payment of a debt. • Predatory lending: to take advantage of ill-informed consumers through high fees.

5 Components of a Credit Score • Payment History-35% • Amount Owed-30% • Length of Credit History-15% • Type of Credit used-10% • New Credit-10%

Well, there are 3 C’s for Credit? • Capacity Can one repay the debt? * Borrower's ability to service a loan from his or her disposable income or cash flow • Character will one repay the debt? Credit History • Collateral- is the creditor fully protected if one fails to repay? * You may need a co-signer (what does this mean?)

6 Things that will impact your credit score the most: • Time since you last opened up an account- don’t open a lot. • How much credit history do you have? • Debt utilization ratio- keep amount of credit available high. • Keep you credit report clean- no red flags. • Carrying a balance on too many credit cards. • Too many hard inquiries…avoid too many inquiries where you are seeking to borrow things.

Ways you can establish a line of credit when you are ready: • Open a bank account (checking/savings) • Purchase of a cell phone contract • Make car payments on time • Make car insurance payments on time • Pay utility/rent bills on time

Ways you can establish a line of credit when ready (cont.) • Have one credit card and designate if for 1 purpose- Example buying gas. (pay off each month)

5 Things to consider if you decide to get a Credit Card • Does the card have an annual fee? • What is the APR/interest rate? • What are the penalty fees and rates? • How long is the grace period? • What type of billing cycle is used?

3 most Common mistakes on the Credit Report • Inaccurate Account Information: other account info shows up under your name. • Incorrect personal details: verify the information to be accurate. (name, addresses, S.S. #) • Fraudulent accounts: in 2016 15.5 million Americans were victims of identity theft. It amounted to 16 billion in stolen funds.

What to do when you find inaccurate information on your credit report • Report it immediately to the credit bureau. • By law, the credit bureau has 60 days to correct it or they must remove it from your credit report. • Contact them by e-mail, telephone, and a certified letter from the Post Office. • Once the credit bureau has your complaint they will contact the creditor or business. If there is a dispute about a paid claim then you and the creditor are now in dispute and the credit bureau is out of the equation.

Do not pay any fees to anyone who says that they maybe able to “fix” your credit report problem. • Maintain a paper trail in the case of future questions or if there are civil matters.

How to keep good Credit and Use Credit wisely • Make timely payments • Consider the type of credit you need • Maintain accurate financial records • Protect your identity on your financial records • Qualify vs. Usage

Your credit score is your financial “GPA”. • You are entitled to one free credit report a year- if you have your credit score run more than 1 time they will deduct points. • Your credit report grows every time you borrow money or opened up a credit line/account. • You can obtain your free credit report by going to: www.annualcreditreport.com

What happens if it all goes sideways and I go bankrupt? • Bankruptcy is always the last option! • Seek bankruptcy only as a last resort and if you have to do this than seek professional financial advice.

Types of Bankruptcy • Chapter 7- called consumer bankruptcy (or small business) and typically lasts 3-6 months. • Most common form of bankruptcy. • Declaring bankruptcy prevents legal action from being taken against the bankruptee.

Some of your property may be sold to pay down your debt and all your unsecured debts are erased. • Unsecured debts are debts with no collateral. • Your clothes, car, and household furnishings are considered exempt under chapter 7. • If you declare bankruptcy you will not be released from the following: child support, taxes, and student loans.

Chapter 13- the “wage earner” bankruptcy. You must have a steady reliable income to be able to repay a portion of the debt.

You must set up a payment plan to repay all your debts in the next 3-5 years. • There are debt limits set forth by the Federal government in this type of bankruptcy. • The amount you have to pay is determined by how much you make, how much you owe, and if you filed chapter 7

Chapter 11- typically reserved for large businesses but is available to individuals businesses. (very costly and time consuming).

If you consider this type- then you need to see a lawyer. • It is used by those whose debts exceed the Chapter 13 limits. • There will be filing fees and it will get complicated so the best thing to do is get legal advice.

Chapter 12- almost identical to Chapter 13 but 80% of your debts must come from a family farm or fishery. • The debt amounts are much higher as it is expensive to operate a farm.

Laws that protect you and your credit • Truth in Lending Act 1968 • Equal Credit Opportunity Act of 1975 • Fair Credit Reporting Act of 1971 • Fair Credit Billing Act • Fair Credit Collections Practices Act of 1977