Download

1 / 13

130 likes | 159 Views

Check out the presentation titled: Types of Construction Business Loans. Brought to you by Moula - https://moula.com.au/finance/complete-guide-business-loans-australia . Moula was founded to help hard-working business owners in Australia access the funding they need to grow. In the past, getting funding meant going through weeks of paperwork, hassle, and hurdles. We use data to assess your loan application, which means we can keep things painless and lightning-speedy. <br><br>With Moula, you can apply online with no paperwork and no hassle, and have the funds in your account the next day. For more info, check out: https://moula.com.au today.

E N D

Construction Business Loans • Construction business loans help to drive the economy. • In Australia, the construction industry includes 1.1 million workers or 9.4 per cent of total employment, making it the third largest employing industry.

Here we’ll Examine some of the Types of Construction Business Loans and How They Can Be Used:

Supporting a Growing Industry with Construction Business Loans • Although there are many opportunities in construction, finance can be a challenge due to seasonal fluctuations that negatively affect cash flow. • At the same time, construction company expenses can seem like they’re endless. These include buying and maintaining equipment, purchasing material and making payroll. • The lack of working capital can make it difficult to start a new construction project while you are waiting to be paid.

Challenges of Getting Bank Construction Loans • While traditional bank loans are available, these require collateral as secured loans. • Many construction business owners are not comfortable using their homes as collateral, so other options are needed when it comes to small business loans.

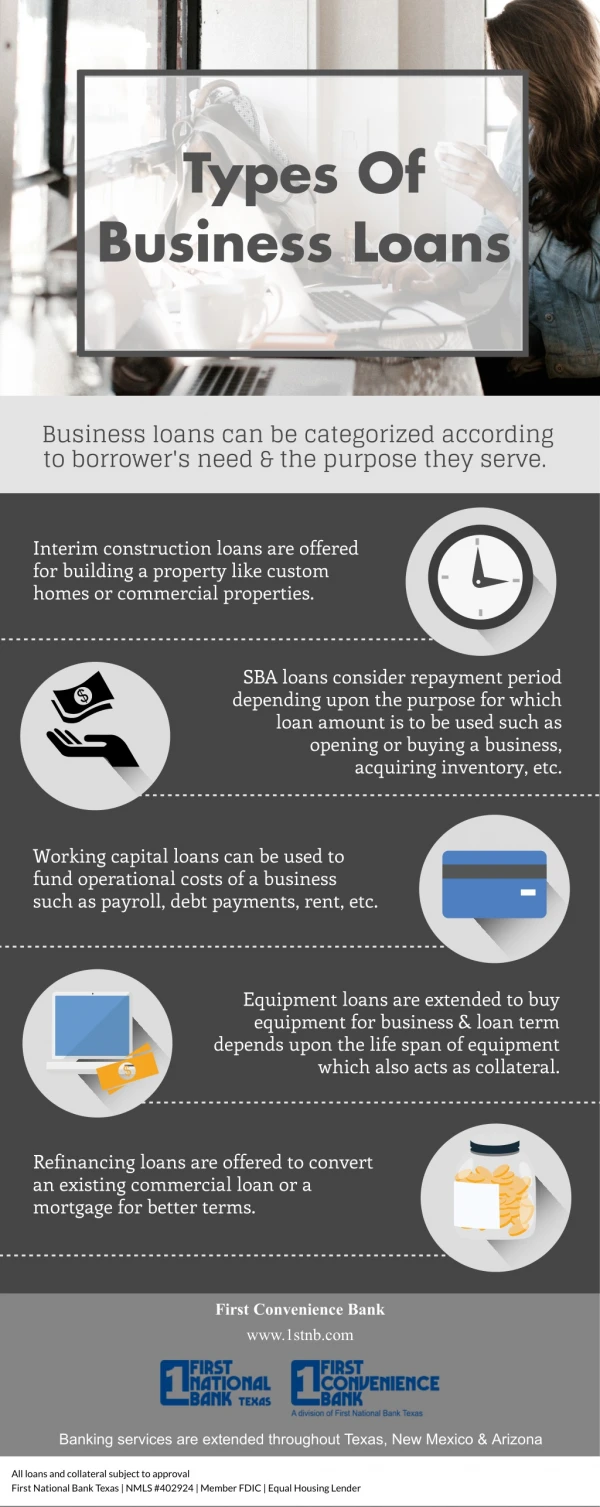

Types of Construction Business Loans • Despite the challenges of finding finance, there are plenty of options available, including: • A business line of credit • Invoice finance • Business credit cards • Equipment loans • Short-term unsecured loans.

Business Line of Credit • With this type of loan, you get a revolving line of credit up to a predetermined limit. You can draw from it repeatedly and only pay interest on what you are borrowing. It’s a helpful option to cover cash flow gaps and seasonal fluctuations. • As a flexible loan, you can draw as little or as much money as you need. Another positive about this type of loan is that approval is usually quick, with loans being approved within a few days. • Interest rates for business lines of credit will vary from around 5% to 13%, with lower interest rates for if the loan is secured. On the negative side, there’s usually an establishment fee of between 0.5% and 3% and an ongoing monthly line fee while the business line of credit is active.

Invoice Finance • Also called receivables finance, this form of lending is suitable if you invoice many customers and don’t want to wait to get paid. It enables you to unlock the value of your invoices and get paid early. The lender uses your outstanding invoices as collateral. You pay interest – usually between 2% and 5% – on the amount you borrow for the invoices are outstanding. • Since you are using your invoices as collateral, you can get finance fairly quickly. Once the lender has determined the creditworthiness of your creditors, you can receive the funds in a matter of days. • There are a few downsides with invoice finance. First, it’s only worthwhile for large construction companies that issue many invoices. Second, if calculate the interest on an annual basis, it can be very high – starting at 24%. Third, if your creditors don’t have a good credit history, their invoices won’t be accepted as collateral by the finance company.

Bank Term Loan • This is a traditional bank loan with a set term. It’s a suitable construction business loan if you know exactly how much you need to borrow and for how long. Bank term loans are secured, requiring collateral in the form of residential or commercial property. • On the positive side, the interest rate on a bank term loan will be on the lower end of the range. The main shortcomings are a large amount of paperwork required in completing the loan application and the time it can take to get approved. • This can be up to several months. So if you need the money quickly, it’s not the right option.

Equipment Finance • This type of construction business finance is used when purchasing large items of machinery or equipment, such as concreting and earthmoving equipment. One form of equipment finance is called a chattel mortgage. With this type of loan, the equipment purchased serves as collateral. Although you own your equipment, like you own a home, you can only sell it if you pay out the balance of the loan. • A hire purchase is a three-party agreement between the borrower, the equipment seller and the lender. The lender purchases the equipment from the seller and then you buy it by making payments over an agreed period of time. The usually includes paying an initial deposit and a balloon payment at the end of the term. After you make the final payment, you gain ownership of the equipment.

Unsecured Business Loans • No collateral is required with an unsecured business loan. The growth of online lenders has simplified the process of getting an unsecured business loan. You don’t have to complete large amounts of paperwork. • With Moula, for example, the online application can be completed in within 10 minutes. In addition, your finances are safely and securely analysed online to determine your eligibility for a business loan and how much you can borrow. • Unsecured business loans are short-term finance so you will need to determine if it matches your finance needs.

Making a Decision on a Construction Business Loan • Read the fine print before deciding to take on a construction business loan. • Check the loan terms and conditions and how they fit with your financial situation. • For example, some loans include a penalty if you repay early.

Check These Out! • Moula was founded to help hard-working business owners in Australia access the funding they need to grow. In the past, getting funding meant going through weeks of paperwork, hassle, and hurdles. We use data to assess your loan application, which means we can keep things painless and lightning-speedy. • With Moula, you can apply online with no paperwork and no hassle, and have the funds in your account the next day. • For more details about business loans Australia Check out: https://moula.com.au