Download

1 / 4

40 likes | 193 Views

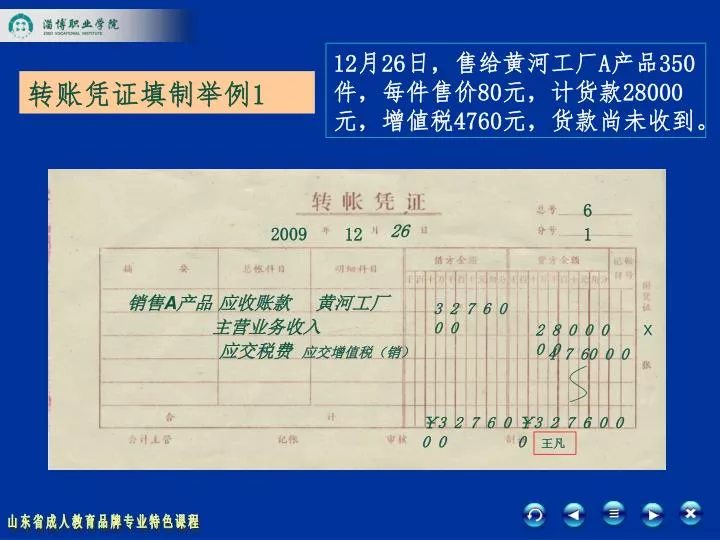

12 月 26 日,售给黄河工厂 A 产品 350 件,每件售价 80 元,计货款 28000 元,增値税 4760 元,货款尚未收到。. 转账凭证填制举例 1. 6. 26. 2009. 12. 1. 销售 A 产品. 应收账款 黄河工厂. 3 2 7 6 0 0 0. 主营业务收入. 2 8 0 0 0 0 0. X. 应交税费 应交增值税(销). 4 7 60 0 0. ¥ 3 2 7 6 0 0 0. ¥ 3 2 7 6 0 0 0. 王凡. 12 月 28 日,将本月发生的制造费用 6700 元,转入生产成本账户 。.

E N D

12月26日,售给黄河工厂A产品350件,每件售价80元,计货款28000元,增値税4760元,货款尚未收到。12月26日,售给黄河工厂A产品350件,每件售价80元,计货款28000元,增値税4760元,货款尚未收到。 转账凭证填制举例1 6 26 2009 12 1 销售A产品 应收账款 黄河工厂 3 2 7 6 0 0 0 主营业务收入 2 8 0 0 0 0 0 X 应交税费 应交增值税(销) 4 7 60 0 0 ¥3 2 7 6 0 0 0 ¥3 2 7 6 0 0 0 王凡

12月28日,将本月发生的制造费用6700元,转入生产成本账户。12月28日,将本月发生的制造费用6700元,转入生产成本账户。 转账凭证的填制举例2 7 28 2009 12 2 生产成本 结转制造费用 6 7 0 0 0 0 制造费用 6 7 0 0 0 0 X ¥6 7 0 0 0 0 ¥6 7 0 0 0 0 王凡

1 2 12月30日,采购员张山报销差旅费1450元,余款退回(原借款1500元)。 该笔业务即涉及收款业务又涉及转账业务,应编制2张记账凭证。 8 2009 12 30 库存现金 3 张山 其他应收款 报销差旅费交回现金 5 0 0 0 X 5 0 0 0 王凡

注意:一笔业务需编制两张或两张以上记账时,其凭证的总号用分数表示。注意:一笔业务需编制两张或两张以上记账时,其凭证的总号用分数表示。 2 2 8 3 2009 12 30 报销差旅费 管理费用 1 4 50 0 0 其他应收款 张山 1 4 5 0 0 0 X ¥ 1 4 5 0 0 0 ¥1 4 5 0 0 0 王凡