Download

1 / 15

150 likes | 341 Views

Internal Controls IFTA Audit Manual Section A640 IRP Audit Procedures Manual(APM) Section 502. Michele Deering-Volz - CA Mark Howshar - WY Marc Walker - NB. Internal Controls Defined Why Evaluate Case Study. Definition of Internal Controls.

E N D

Internal ControlsIFTA Audit Manual Section A640IRP Audit Procedures Manual(APM) Section 502

Michele Deering-Volz - CA Mark Howshar - WY Marc Walker - NB

Internal Controls Defined Why Evaluate Case Study

Definition of Internal Controls a process for assuring achievement of an organization's objectives in operational effectiveness and efficiency, reliable financial reporting, and compliance with laws, regulations and policies.

APM Section 502/IFTA A640 The Auditor must test the effectiveness of internal controls. Based on the result of these tests, the auditor should make an assessment of the degree of reliance that can be placed on the internal controls

Strengths and weaknesses identified in the Registrant’s distance accounting system must be documented in the Audit file.

RECORDKEEPING SYSTEM The auditor should perform a Walk-through test .

Walk-Through • (i)…select one or more source documents to follow through the entire process • (ii) …ask to review each point where some action is taken

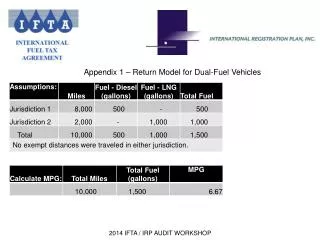

Case Study Introduction Distance Record Example Unit 8 – 1st ’11 1st ‘11 Summary – Unit 8

Purpose of Walk-Through • Better understanding of the detailed operations • What error types are possible • What controls would detect these errors • Does the registrant employ these controls

Evaluate… Are the controls effective and functioning as described? Can the system be audited?

IFTA A640.300Tests of Compliance If controls are inadequate to permit reliance, the auditor may make a more extensive review and perform tests of compliance.

If weaknesses identified in the preliminary evaluation preclude reliance, or if the auditor believes that more efficient or effective audit tests are possible without reliance, the auditor will plan audit procedures without any further study and evaluation of accounting control.

Case Study Files • Prepare/Maintain Records Agreement • ABC Co IFTA Workpaper Workbook • ABC Co Internal 2011 Calculation • ABC Co Summary Information • ABC Co Summary Subset - 37, 8, 55 • ABC Co Email conversations

Case Study / Questions • Case Study Resolution • Questions?