Download

1 / 16

170 likes | 315 Views

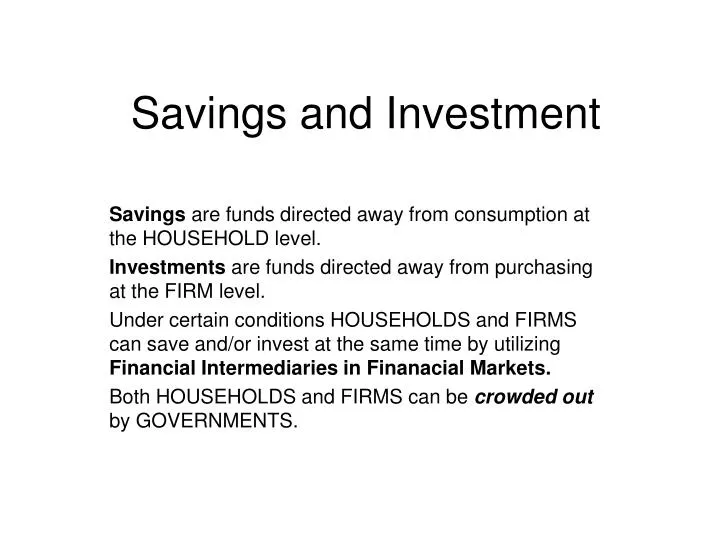

Savings and Investment. Savings are funds directed away from consumption at the HOUSEHOLD level. Investments are funds directed away from purchasing at the FIRM level.

E N D

Savings and Investment Savings are funds directed away from consumption at the HOUSEHOLD level. Investments are funds directed away from purchasing at the FIRM level. Under certain conditions HOUSEHOLDS and FIRMS can save and/or invest at the same time by utilizing Financial Intermediaries in Finanacial Markets. Both HOUSEHOLDS and FIRMS can be crowded out by GOVERNMENTS.

Financial Intermediaries • Financial Intermediaries arrange to bring lenders (those with funds available to lend) and borrowers (those who need funds) together. • Financial Intermediaries operate in regulated markets where there is assumed to be efficiency in transactions. (No single participant can manipulate the market and there is no insider trtading or “leaks” of confidential information that is not readily and freely available to everyone. • An efficient market means that transactions costs are standard and are minimal. • Examples of these markets are the bond market, the stock market and the futures market. • Examples of financial intermediaries are banks, trust companies, credit unions, insurance companies and certain professions that have fiduciary authority.

Bonds • Bonds are direct borrowing by GOVERNMENTS and FIRMS. • The Bond has a value that will be returned to the purchaser at a certain future point in time. The purchaser then bids to acquire the bond at the currentmarket price. The interest rate attached to the bond is unique but because there is efficiency in the market and there is standard currency, there will exist one and only one interest rate for each bond. There need not be any purchasing of a bond on any given day. • Individual bond interest rates called discount rates will differ from one corporation to the next based on: - term : how long the bond will take to pay back to the purchaser and - credit risk : level of debt carried by the issuer, how the issuer has performed recently, and the stability of revenue streams. Bond Rating Agencies publish evaluations of bond issuers.

Stocks • Stocks are an ownership share in the CORPORATION issuing the stock. • Stocks are offered to be sold to the public based on specific regulations and a formal publicly available document called a Prospectus. • Stocks are traded on an exchange. • Stocks are either common with no dividends payable or preferred with dividends payable. • Market Indices are published indicators of the value of ownership of CORPORATIONS in general. The DOW JONES and The TSX are examples. • In each market trading session there are bid prices from buyers and ask prices form sellers. For every price to be recorded there must be a transaction during that session.

Futures Markets • Primarily dealing with commodities such as oil, gold, wheat, pork bellies and currencies, these markets establish the price that a buyer is wiling to pay for delivery at a certain specified date for the commodity in question called a futures contract • The open price is set based on the street price when the market begins. There must be a purchaser matched with each seller for there to be a recorded price, but there are many buyers and many sellers so the open price from the previous session is carried over but is limited each day. When the futures contract is delivered the street price usually equals the futures price. • Gambling on how quickly prices will fall or rise is called speculation. • A producer of the product will try to guarantee a price by buying a future contract for the time when he will deliver the product at which time he will sell at that price. This is called hedging.

Economics of Financial Markets • Bond markets operate on average to identify and capture time value of money risk. This is reflected in the Net Present Value of the bond itself. • Stock markets operate to identify and capture current risk and the stability of the economic interplay between buyers and sellers thereby removing or standardizing transactions costs of ownership. • Futures markets operate at the margin to isolate any diseconomies that may affect overall stability by moving basic commodities through the production cycle. Futures markets are the bell weather of the domestic economy. • An economy that denies access to any one of these three financial market types is prone to capital collapse where funds cannot be borrowed, households cannot save, and speculation is a black market activity.

Financial Intermediaries • HOUSEHOLDS and FIRMS may not consume all of their income, but instead hold back a portion for a major purchase in the future, or against an unexpected need for funds. When they surrender these funds for safe keeping to another entity they are placing Fiduciary Trust in that entity on average . • This may be with a bank, trust company, credit union, insurance company, or a lawyer who accepts the Fiduciary Trust and is called a Financial Intermediary. • The entity will then anticipate how long it will have these funds in its possession less its payment of a fractional reserve to the GOVERNMENT and will Invest in FIRMS and HOUSEHOLDS through loans at the margin. The borrowers will pay back the loans with interest and the lenders will receive a portion of that interest less transactions costs credited to their account. The borrowers may also enter into a Fiduciary Trust with an intermediary and those funds will also be invested. • This is called a multiplier effect.

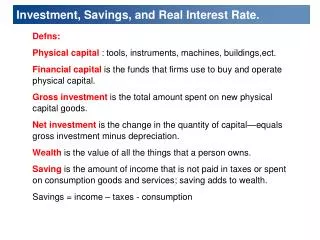

Economics of Financial Markets • For the Domestic Economy: • [Y=C+I+G] • [Y-C-G=I] • [Y-C-G=S where S = National Savings] • Now if we assume that GOVERNMENT pays for Government Spending G through Taxes T we have • [(Y-T-C) + (T-G)]=S where Y-T-C is private savings and T-G is public savings which is a budget surplus if positive and a deficit if negative. • Because S=I must hold at all times then there is a demand for and a supply of loanable funds [Y-T-C], with the price being equal to the interest rate .

Loanable Funds: Taxes • If CONSUMPTION does not change and GOVERNMNENT SPENDING does not change, then a change in Taxes will increase or decrease the supply of loanable funds . Supply :Taxes Unchanged Interest Rate Supply : Taxes Decreased Interest Rates Fall Demand Loanable Funds Increase Loanable Funds

Loanable Funds: Governmnet Spending • If CONSUMPTION does not change and Taxes dos not change, then a change in GOVERNMENT SPENDING will increase or decrease the demand for loanable funds. Interest Rate Demand for Loanable Funds Increased due to Government Spending Interest Rates Increase Demand for Loanable Funds Unchanged Loanable Funds Loanable Funds Increase

Loanable Funds: Budget • When GOVERNMENT runs a deficit … spends more than it takes in… it reduces the supply of loanable funds and drives up the interest rate by crowding out FIRMS and HOUSEHOLDS. Supply :Deficit Interest Rate Supply :Balanced Budget Interest Rates Increase Demand Loanable Funds Decrease Loanable Funds

The Basics of The Budget Budgeting has numerous impacts on the economy but the primary impact is on savings. The balance of the budget has direct and indirect effects. A surplus has the effect of reducing the pressure on citizens to save. A deficit increases the pressure on citizens to save. As citizens save more, the interest rate falls but as the citizens save less the interest rate rises as long as there is a constant need to invest by the business sector. If the interest rates are pushed down while there is a deficit this results in projects being initiated which have a return greater than the alternative financial return via the interest rate and this leads to pursuit of projects which may ultimately prove unprofitable. Similarly if interest rates rise during a surplus there is increased competition between the public sector financing through bonds and the needs for business investment financing and the private sector is pushed out or crowded out of the savings market. Surpluses and Deficits are used by governments to try to heat up (stimulate) or cool down (de-stimulate) economic activity and this is known as Fiscal Policy . If at the same time the government operates policies that effect the money supply (Monetary Policy), it may counter or reinforce its overall economic and political agenda. Fiscal and Monetary Policy are the major tools that are available to the government to manage the economy.

Investment - Savings (IS) and the Interest Rate (r) Note that as the interest rate falls savings are drawn down increasing the level of income (Y) but as the interest rate rises the level of income falls. r IS Y

Fiscal Policy Impacts • Fiscal policy is one of the major tools available to government and it operates through a number of distinct pathways: • * It creates the impression that the government is giving money to certain groups through tax deductions and credits, through direct subsidies and specialized treatment or through focusing attention on specialized groups. This is the goal of those who use lobbyists to advance their positions . Generally these actions are controlled through conflict of interest legislation and special investigative regulations which constitute statutory regulations. • * It creates direct competition in the marketplace for loanable funds wherein private projects and public projects compete for available funds and may result in one sector or the other being “shoved in” or “pushed out” of the funds pool. This is market regulated. • * It sets a pathway for future expectations which can influence the time discount rate by which citizens set their expectations for the future and in so doing may encourage long term investment decisions over shorter term decisions and visa versa such that foreign interests may become interested in moving capital into the country or out of it and that may result in exchange rate fluctuations. This regulation is international through the exchange rate.

The Fiscal Policy Triangle Exchange Rate Market Regulation

Fiscal Policy is Effective but not Efficient • Failure to account for the market, the exchange rate or the regulatory environment can lead to political and economic catastrophe unless there is an appropriate balance to the government influence of the economy. • The result can be inflation and sometimes even hyperinflation, stagnation and economic collapse, and resurrection and even revolution. • The other side of the equation is the monetary policy that will be discussed in a later lecture. • Fiscal policy is effective in that it can get the “job done” but it is not efficient in that there can be many and varied long term repercussions as a result.