Download

1 / 28

280 likes | 469 Views

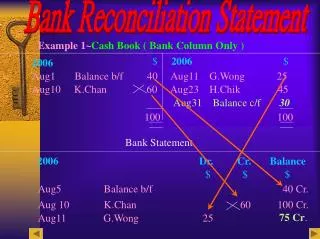

Bank Reconciliation Statement. 2006 Dr. Cr. Balance. $ $ $. Example 1~. Cash Book ( Bank Column Only ). $. 2006. $. 2006. Aug1. Balance b/f 40 Aug11 G.Wong 25.

E N D

Bank Reconciliation Statement 2006 Dr. Cr. Balance $ $ $ Example 1~ Cash Book ( Bank Column Only ) $ 2006 $ 2006 Aug1 Balance b/f 40 Aug11 G.Wong 25 Aug10 K.Chan 60 Aug23 H.Chik 45 Aug31 Balance c/f 30 100 100 Bank Statement Aug5 Balance b/f 40 Cr. Aug 10 K.Chan 60 100 Cr. 75 Cr. Aug11 G.Wong 25

Questions: 1. Should the ending balance of the Cash Book and Bank Statement be the same? 2. Why they should be the same? 3. Can you tell me why there is a difference between their ending balances?

Reasons for differences between ending balances of Cash Book and Bank Statement • Timing differences E.g. A receipt of $50 from A.Lee on Aug 28 were credited by the bank on Sept 3 • Omissions and Errors E.g. A payment of electricity fee by the bank of $300 was omitted in the Cash Book

Items that might explain timing differences omissions and errors ( 1 ) Unpresented Cheques • Cheques issued by the firm not presented • for payment by the bank. E.g Cash Book (Bank) 2005 $ Dec 31 Furniture 100 Bank Statement 2006 Dr. Cr. Balance $ $ $ Jan 10 Furniture 100 100 Dr

( 2 ) Uncredited Items ( Bank Lodgement not yet entered on Bank Statement) • Deposits entered into the Cash Book • but not yet appeared on Bank Statement E.g Cash Book (Bank) 2005 $ Dec 30 Sales 100 Bank Statement 2006 Dr. Cr. Balance $ $ $ Jan 2 Sales 100 100 Cr

( 3 ) Direct Debits • Payments made directly through the bank E.g Cash Book (Bank) 2006 $ Jan 3 Rates 700 Bank Statement 2005 Dr. Cr. Balance $ $ $ Dec 20 Rates 700 700 Dr

( 4 ) Bank Charges • Charges for banking services made by the bank for • the company E.g Cash Book (Bank) 2006 $ Jan 3 Bank Charges 20 Bank Statement 2005 Dr. Cr. Balance $ $ $ Dec 25 Bank Charges 20 20 Dr

( 5 ) Standing Orders • Standing instructions from the firm to • make regular payments by the bank E.g Cash Book (Bank) 2006 $ Jan 2 subscriptions 300 Bank Statement 2005 Dr. Cr. Balance $ $ $ Dec 10 subscription 300 300 Dr

( 6 ) Credit transfers/ direct credits • Collection from customers made direct to the bank • through the banking system E.g Cash Book (Bank) 2006 $ Jan 2 subscriptions 400 Bank Statement 2005 Dr. Cr. Balance $ $ $ Dec 17 subscription 400 400 Cr

( 7 ) Dishonoured Cheque • Cheque deposited into the bank but returned by the bank marked ‘refer to drawer’ ( i.e. the drawer fails to pay ) E.g Cash Book (Bank) 2005$ Dec 7 A.Chan 500 Bank Statement 2005 Dr. Cr. Balance $ $ $ Dec 9 A.Chan 500 500 Cr Dec 11 A.Chan 500 0 (Refer to drawer)

( 8 ) Interest allowed by the bank • Interest received from the bank for deposits or fixed • deposits into the bank E.g Cash Book (Bank) 2006 $ Jan 2 Interest received 10 Bank Statement 2005 Dr. Cr. Balance $ $ $ Dec 20 Interest received 10 10 Cr

Purposes of Bank Reconciliation Statement • Explain the reasons for differences • Identify errors and omissions in the • Cash Book and the Bank Statement • Make corrections

Drawing up a Bank Reconciliation Statement 2006 Dr. Cr. Balance $ $ $ Example 2 Cash Book ( Bank Column Only ) $ 2006 $ 2006 Aug1 Balance b/f 40 Aug11 G.Wong 25 Aug10 K.Chan 60 Aug23 H.Chik 45 Aug31 Balance c/f30 100 100 Bank Statement Aug 1 Balance b/f 40 Cr. Aug 10 K.Chan 60 100 Cr. Aug 11 G.Wong 25 75 Cr.

Preparing the Bank Reconciliation Statement $ $ Balance in hand as per Bank Statement 75 Bank Reconciliation Statement as at 31 August 2006 Balance in hand as per Cash Book 30 Add Unpresented cheque : H.Chik 45 Balance in hand as per bank statement 75 Bank Reconciliation Statement as at 31 August 2006 Less: Unpresented cheque :H.Chik 45 Balance in hand as per Cash Book 30

Exercise1 Cash Book 2008 Dr. Cr. Balance $ $ $ $ 2008 $ 2008 Dec26 Balance b/f 500 Dec27Y. Chan 100 Dec28 G.Poon 70 Dec29 C.Cheung 25 Dec 31 A.Tang 230 Dec31 Balance c/f 675 800 800 Bank Statement Dec 26 Balance b/f 500 Cr. Dec 29 Cheque 70 570 Cr. Dec 30 Y. Chan 100 470 Cr. Credit Transfer: L.Chung 60 530 Cr. Bank Charges 20 510 Cr.

Drawing up a Bank Reconciliation Statement 2006 Dr. Cr. Balance $ $ $ Example 3 Cash Book ( Bank Column Only ) 2006 $ 2006 $ Aug27 Balance b/f 400Aug28 W.Wong 55 Aug29 T.Pong 50 Aug30 A.Kong 20 Aug30 G.Lee 110 Aug31 Balance c/f 485 560 560 Bank Statement Aug 27 Balance b/f 400 Cr. Aug 29 Cheque 50450 Cr. Aug 30 W.Wong 55395 Cr. Aug 30 Credit transfer: G.Lau 60 455 Cr. Aug 30 Bank Charges 40415 Cr.

What is the amount difference between the Cash Book and the Bank Statement? Answer : $485-$415=$70

Updating Cash Book Credit Transfer Debit Cash Book (since not yet entered in Cash Book) Bank interest Standing Order/ Direct Debit Credit Cash Book (since not yet entered in Cash Book) Bank Charges Dishonoured Cheques

Cash Book 2006 $2006 $ Aug 31 Balance b/f 485 Aug 31 Bank charges 40 Aug 31 Credit transfer 60 Aug 31 Balance c/f 505 545545

Preparing the Bank Reconciliation Statement Bank Reconciliation Statement as at 31 August 2006 $ Balance in hand as per Cash Book 505 Add Unpresented cheque :A.Kong 20 525 Less Uncreditd items 110 Balance in hand as per bank statement 415

Bank Reconciliation Statement as at 31 August 2006 $ $ Balance in hand as per Cash Book 485 Add Unpresented cheque :A.Kong 20 Credit transfer : G.Lam 6080 565 Less Uncredited items : G.Lee 110 Bank charges 40 150 Balance in hand as per Bank Statement 415

Bank Reconciliation Statement as at 31 August 2006 $ $ Balance in hand as per Bank Statement 415 Add Uncredited items :G.Lee 110 Bank charges 40150 565 Less Unpresented cheque :A.Kong 20 Credit transfer :A.Lam 6080 Balance in hand as per Cash Book 485

Adjustment Table Effect onEffect onAdjustmentAdjustment Items Cash BookBank to Cashto Bank balanceStatementBookStatement balance balance Balance 1) 一 一 十 Unpresented cheque 2) 一 十 十 Uncredited items 3) 一 十 一 Direct debits

Effect onEffect onAdjustmentAdjustment Items Cash BookBank to Cashto Bank balanceBookStatement balancebalance 4) 一 一 十 Bank charges 5) 一 一 十 Standing orders 6) Credit 十 十 一 transfer/ direct credits

Effect onEffect onAdjustmentAdjustment Items Cash Book Bank to Cashto Bank balance balance balance 7) 一 一 十 Dishonoured cheque 8) Interest 十 十 一 allowed by the bank

Bank Overdrafts (Shown by a credit Balance in the Cash Book) Cash Book 2006 $ Nov1 Balance b/f 300 Bank overdraft Bank Statement 2006 Dr Cr Balance $ $ $ Nov1 Balance b/f 300 O/D

Example Cash Book 2007 $ 2007 $ Dec 4 A. Ko X 290 Dec 1 Balance b/f 522 Dec 24 N. Ng X 110 Dec 5 K.Wong 120 Dec 29 M.Ming 110 Dec 23 D.Fung 50 Dec 31 B.Tam 103 Dec 29 A.Co 70 Dec 31 Balance c/d 199 Dec 31 Bank Charges 50 812 812 Bank Statement 2007 Dr.Cr.Balance $ $ $ Dec 1 Balance b/f 522 O/D Dec 5 Cheque 290 X 232 O/D K.Wong 120 352 O/D Dec 24 Cheque 110 X 242 O/D Dec 29 M.Ming: Credit Transfer 110 132 O/D Dec 29 A.Co. 70 202 O/D Dec 31 Bank Charges 50 252 O/D

Answers Bank Reconciliation Statement as at 31 December 2007 $ Overdraft as per Cash Book 199 Less Bank Lodgement not yet entered on Bank Statement 103 302 Add Unpresented Cheque 50 252