Download

1 / 6

60 likes | 136 Views

Dive into the intricate details of how GE Capital and Castle Harbour Leasing navigate the complexities of aircraft leasing, tax strategies, and financial structures. Explore the motivating factors and deal structures behind their operations, including tax savings, debt ratios, and cash flows. Learn about the legal implications and ongoing litigation with the IRS. Discover how under-the-table cash payments and tax-deductible interest play a role in this tangled web of aviation finance.

E N D

GE Capital and Castle Harbour A Tangled Web

Motivating Factors • Poor performance of airline industry • Weak secondary market • Credit rating/debt ratio • Retention of interest in aircraft • Tax savings

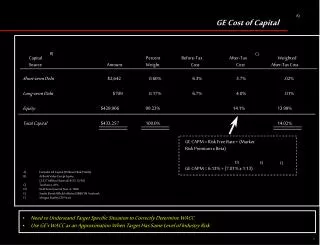

$530M in Aircraft, $258M in Debt, $22M in Rec., $296M in Cash, $0 in Stock Deal Structure GECC TIFD III - E TIFD III - M TIFD IV GE Capital AG ING Bank N.V. Rabo Merchant Bank N.V. Castle Harbour Leasing GE Capital Summer Street - 1 LLC Castle Harbour (Organized as Partnership) $50M + $67.5M Cash

Cash Flows GECC Cash to GECC Subs No taxes CHL buys GECC Commercial Paper Interest is tax deductible Under-the-table cash payments Castle Harbour Leasing GECC Subsidiaries Cash in/out No taxes Asset step up Cash to CHL No taxes Castle Harbour Dutch Banks Cash in/out No taxes Aircraft Lease Payments

End Results • GECC was able to re-depreciate its aircraft • The gain on the disposition of the aircraft was not taxed • GECC was able to save about $62M in taxes • Litigation is ongoing, as the IRS plans to appeal its recent loss on the case