Electronic Payment Systems

Electronic Payment Systems. Most of the electronic payment systems on internet use cryptography in one way or the other to ensure confidentiality and security of the payment information.

Electronic Payment Systems

E N D

Presentation Transcript

Electronic Payment Systems Most of the electronic payment systems on internet use cryptography in one way or the other to ensure confidentiality and security of the payment information. Some of the popular payment systems on internet include the credit-card based payment systems, electronic checks, electronic cash, micro-payment systems (milicent, payword etc.)

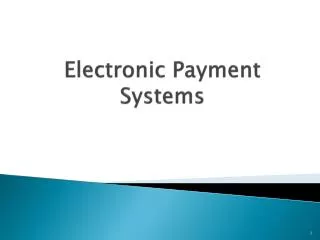

Card Holder Merchant 2. Show Credit Card 3. Authorization 4. Capture Card Brand 1. Issuer Credit Card 5. Payment Request 6. Payment Transfer Acquirer Bank Issuer Bank Card Holder Account Merchant Account

The Process of Using Credit Cards 1. A potential cardholder requests an issuing bank in which the cardholder may have an account, the issuance of a card brand (like Visa or MasterCard). The issuing bank approves (or denies) the application. If approved, a plastic card is physically delivered to the customer’s address by mail. The card is activated as soon as the cardholder calls the bank for initiation and signs the back of the card. 2. The cardholder shows the card to a merchant whenever he or she needs to pay for a product or service. 3. The merchant then asks for approval from the brand company (Visa etc.) and the transaction is paid by credit. The merchant keeps a sales slip

4. The merchant sends the slip to the acquirer bank and pays a fee for the service. This is called a capturing process. 5. The acquirer bank requests the brand to clear for the credit amount and gets paid. 6. Then the brand asks for clearance to the issuer bank. The amount is transferred from issuer to brand. The same amount is deducted from the cardholder’s account in the issuing bank.

Virtual PIN Payment System A buyer browses the web server where FV registered merchant is selling goods. The buyer is asked to enter his/her Virtual PIN by the merchant site . Merchant queries the FV Internet Payment System Server (FVIPSS) to confirm Virtual PIN If Virtual PIN is not blacklisted Merchant may acknowledge this fact to the buyer by email and sends the goods, and also sends transaction details to FV

FVIPSS or simply FV server sends email to the buyer if the goods were satisfactory There are three possible answers to that If the answer is “accept” then the payment proceeds, in case the answer is “reject” it means that either the goods have not been received or the buyer is not satisfied with the quality of goods. Then the payment is not made to the merchant. If the answer indicates “fraud” it means that the goods were never ordered. In such an eventuality the FVIPSS immediately blacklists Virtual PIN so that it cannot be used in the future.

Centralized Account Payment Model In this both the payer (buyer) and the payee (merchant) hold accounts at the same centralized on-line financial institution. PayPal, E-gold, Billpoint, Cybergold, Yahoo! Pay Direct, Centralized bank using credit/debit card or prepaid cards. To make payment an account holder is authenticated using an account identifier and a password, account identifier of the payee and the payment amount.

All communication between the user and the bank is protected using SSL (Secure Socket Layer), which is an encryption based protocol. Normally, the unique email addresses of the users are chosen as account identifiers.

Electronic Checks An electronic check contains an instruction to the payer’s bank to make a specified payment to a payee. The payer and the payee are issued digital certificates All individuals capable of issuing electronic checks will have an electronic check book device. An electronic check book device is a combination of secure hardware such as a smart card and appropriate software. A smart card is usually the size of a credit card having special software loaded on it. Information regarding secret/private key, certificate information and register of what checks have been signed/endorsed is normally stored in the smart card.