Download

1 / 38

380 likes | 487 Views

Understanding Life Insurance with LTC Riders and Advanced Marketing Opportunities. Some Things You Should Know.

E N D

Understanding Life Insurance with LTC Riders and Advanced Marketing Opportunities FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Some Things You Should Know • This presentation was not intended by the author to be used, by anybody for the purpose of avoiding any penalties that may be imposed on you pursuant to the Internal Revenue Code. The information contained herein was prepared to support the promotion, marketing and/or sale of life insurance contracts, annuity contracts and/or other products and services provided by Nationwide Life Insurance Company. • Federal tax laws are complex and subject to change. Neither the company nor its representatives give legal or tax advice. Please talk with your attorney or tax advisor for answers to your specific questions. • Investing involves risk, including possible loss of principal • Keep in mind that as an acceleration of the death benefit, the LTC rider payout will reduce both the death benefit and cash surrender values. Care should be taken to make sure that your clients' life insurance needs continue to be met even if the rider pays out in full. There is no guarantee that the rider will cover the entire cost for all of the insured's long-term care as these vary with the needs of each insured. FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Some Things You Should Know • When evaluating the purchase of a variable annuity, your clients should be aware that variable annuities are long-term investment vehicles designed for retirement purposes and will fluctuate in value; annuities have limitations; and investing involves market risk, including possible loss of principal. • This information assumes that the life insurance is not a modified endowment contract, or MEC. As long as the contract meets the non-MEC definitions of IRC Section 7702A, most distributions are taxed on a first-in/first-out basis. Surrender charges may apply to partial surrenders. Loans and partial surrenders from a MEC will generally be taxable, and if taken prior to age 59 ½, may be subject to a 10% tax penalty. Loans and partial surrenders will reduce the cash value and the death benefits payable to your beneficiaries, and withdrawals above the available free amount will incur surrender charges. If your contract were to lapse with a loan outstanding, the loan amount in excess of basis will be treated as a distribution and all or a portion will be subject to income tax. • The underlying investment options to a variable annuity or life insurance product are not publicly traded mutual funds and are not available directly for purchase by the general public. They are only available through variable annuity/variable life insurance policies issued by life insurance companies. FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Some Things You Should Know • As your clients’ personal situations change (i.e., marriage, birth of a child or job promotion), so will their life insurance needs. Care should be taken to ensure these strategies and products are suitable for long-term life insurance needs. You should weigh your clients’ objectives, time horizon and risk tolerance as well as any associated costs before investing. Also, be aware that market volatility can lead to the possibility of the need for additional premium in the policy. Variable life insurance has fees and charges associated with it that include costs of insurance that vary with such characteristics of the insured as gender, health and age, underlying fund charges and expenses, and additional charges for riders that customize a policy to fit your clients’ individual needs. • Not all Nationwide products and services are suitable for all clients or situations. There may be products, issued by other companies, which better suit your clients’ goals. Be sure to consider your clients’ objectives, their need for cash flow and liquidity, and overall risk tolerance when using any strategy. • This information was developed to promote and support products and services offered by Nationwide. It should not be taken as tax advice. It was not written or meant to be used by any taxpayer to avoid tax penalties, and it cannot be used by any taxpayer for that purpose. • Life insurance and annuities are issued by Nationwide Life Insurance Company or Nationwide Life and Annuity Insurance Company, Columbus, Ohio, member of Nationwide Financial®. The general distributor for variable insurance products is Nationwide Investment Services Corporation, member FINRA. In Michigan only: Nationwide Investment Svcs. Corporation. Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Agenda • The current LTC marketplace • A Brief Look at the Variety of LTC Solutions • The Explosion of Life Insurance Linked Solutions – Product Differentiators • Nationwide’s Indemnity-style LTC Rider • Advanced Market applications FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

The Current LTC Market Place FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Traditional LTC – Current Status Growth in traditional LTC sales disappointing1 • Sales down 2006-2009 • Sales down 23% in 2009 • Compound annual growth rate -5% between 2005-2010 1 LIMRA – U.S. Individual LTC Insurance Annual Review 2010 FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Traditional LTC – Current Status Concerns in traditional LTC market place1 • Significant premium increases on in-force polices • Companies leaving the marketplace • What is contributing to this dilemma? • Unexpectedly low lapse rates on LTCI polices • Claim payouts doubled between 2006 & 20092 • People living longer – boomers joining parents • Declining interest rates • 40% to 60% claims revenue depends on investment returns 1“Long Term Care Insurance May go the Way of the Dinosaur”, Investment News, March 18, 2012 2 “Long Term Care Headache” – Financial Advisor Magazine, January 2011 FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Consumer perceptions/objections • LTCI is expensive • It’s not necessary • Use it or lose it • Mistrust of industry • Affluent believe they can just self-insure • Unaware of alternative solutions “Why People Don’t Buy Long-Term Care Insurance”, Howard Gleckman, Forbes, Sept. 12, 2011 FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

A Variety of LTC Solutions • Traditional LTC • Most economical way to insure LTC • Most customizable • Single premium LTC/life asset based products • Return of premium and cost recovery • LTC focused solutions • Annuity/LTC linked product • Limited resources to work with • Insurability issues • Life Insurance/LTC linked products • Long term care concerns • A need for life insurance for financial protection FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Life Insurance Linked Solutions to Long-term Care and Chronic Illness Product Differentiators FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Life Insurance/LTC Combo • Classification of rider determines: • How product can be marketed • Requirements needed to sell a product • How rider is charged for • How claims are paid FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Product Differentiators • LTC Riders classified as 7702B • Can be marketed and referred to as Long-term Care • Tax free per IRS Sec. 7702B LTC rules • 2 impaired ADLs or Cognitive Impairment certified • Covers temporary and permanent claim conditions • Rider is available for an additional charge • Underwritten for LTC risk • LTC amount set at policy issue • Does not require separate LTC license • Many states require state specific LTC CE or other licenses • Must have licenses to sell the base life insurance product FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

What Differentiates 7702BLTC Riders? Indemnity vs. Reimbursement Benefits • Reimbursement • Reimburses only cost of care up to the benefit limit. • Require receipts to be submitted • Some will allow facility to bill insurance company direct • Not all charges on bill may qualify for reimbursement • Benefit not limited to HIPAA • Indemnity • Pays benefit directly to contract owner • No bills or receipts to submit for claims reimbursement • Some companies require monthly re-verification of billable services • Physician’s plan of care • Excess benefits can be used for other purposes • Benefit usually limited by some tie in to HIPAA FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Product Differentiators • Chronic Illness riders 101(g) classified • Some companies build riders under regulations that have the following provisions: • Cannot be marketed as a long-term care product • “Accelerated Death Benefit for Chronic Illness” • 2 impaired ADLs or Cognitive Impairment • Requires claim to be diagnosed as “likely to be for lifetime of insured”. (no temporary claims) • Benefits tax free when individually owned per Sec. 101(g) • May underwrite and charge for the rider, or include with the policy and discount • All pay by indemnity since claims reimbursement not possible • Does not require separate LTC license and currently does not have state CE requirements FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

What Differentiates 101(g) Chronic Illness Riders? • Charge for rider • Underwritten for chronic illness risk • Monthly deductions charged • Chronic Illness amount and benefit determined at policy issue • Included with the policy – death benefit discounted at time of claim • No underwriting, available to all • Not “free” – Charged for at time of claim • Death benefit discounted at claim by actuary factors • No charge if never used • Can’t determine benefit amount until time of claim • Younger the insured is, the less that is received FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Nationwide Life Insurance with the Long-term Care Rider FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Nationwide LTC Rider An alternative solution is Nationwide’s Long-term Care rider: • LTC benefit paid tax free as an accelerated death benefit • Death benefit provides pool of money • Someone receives money as LTC or death benefit • Cash value • Some contracts offer death benefit and premium guarantees for life of insured including LTC rider • LTC benefit reduces death benefit dollar for dollar • LTC rider amount may be dialed down to preserve some needed death benefit (not available in NY, KY or Virgin Islands) FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Nationwide LTC Rider • Cognitive impairment • Doctor certifies an impairment (includes Alzheimer’s and dementia) OR • Two ADLs impaired • Unable to perform 2 or more of activities of daily living: • Bathing, dressing, continence, eating, toileting, transferring • One-time 90-day elimination period before benefits are paid • May be met over a 730 day time period FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Nationwide LTC Rider • LTC benefit is lesser of: • 2% per month of death benefit/rider amount OR • Daily per diem rate established by HIPAA times days in the month • 2012 per diem rate = $310/day • Example: • 500K LTC rider x 2% = $10,000 per month OR • The HIPAA per diem of $310/day x 30 days in a month = $9,300 per month • In this case, client would receive $9,300/month • Benefit lasts at least 4 years & 2 months* Note: the 2012 per diem amount allowed by Health Insurance Portability and Accountability Act is $310 per day. Maximum annual amount for 2012 is $113,590 *Assuming no loans or withdrawals have been taken prior to collecting LTC benefit. FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Nationwide LTC Rider • Covered benefits include services such as: • Nursing home • Home health care • Assisted living • Adult day care • Hospice • Indemnity-style plan • Benefit paid to owner of contract • Direct payment – no receipts! • No monthly re-verification of billable services • Supplemental Family Care FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Nationwide LTC Rider • Issue ages 21-80 (SPUL is 35-80) • Lapse protection provision • Tax-free benefits (even on a MEC) • Guaranteed minimum death benefit (not available in NY, KY or Virgin Islands) • Benefits may be payable outside US • Available on most Nationwide permanent individual life insurance policies (not available in all states) • LTC Rider can be rated up to 5 tables FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Using an Indemnity-style Long-term Care Rider to Enhance a Life Insurance Need in Advanced Markets • Estate Planning Tool • Business Succession • Special Needs Trust • Charitable Giving • Executive Benefits FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

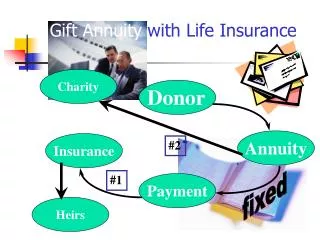

Estate Planning Tool • LTC riders can be used in ILIT if product pays an indemnity benefit. • Rider is paid to contract owner (the trustee) with no obligations to pay funds to grantor • Use of collateralized arms length loans removes money from trust without incidents of ownership • Collateral • Interest Rate • Loan is repaid in full • Interest taxable if repaid after death • Reimbursement plans will not work • Reimbursement is tied directly to grantor and creates incidents of ownership FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

What does self insuring LTC mean to an affluent client? Client sets aside $1,000,000 to cover any LTC Costs. Asset is liquid and in the estate. 50% chance of using some or all of asset for LTC costs1 Little or no amount from this asset would be estate taxed since it was liquidated to pay LTC costs 50% chance of not needing this asset for LTC costs $1,000,000 The untouched $1 million would be estate taxed. At 2012 rates, this could mean a tax rate of as much as 35% ($350,000) 1The Washington Post, Jan 23, 2012, Amy Pahl, Milliman, Inc. FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Example • Our client, Jane, has a $5 million tax liability • Assume product can dial down LTC rider • Add a $1 million LTC rider • When no dial down possible, use two policies • $4 million policy with no LTC rider • $1 million policy with a LTC rider • Assuming the following loan provisions • Collateral is the vacation home • Interest rate is 7% • Loan paid back just days before death FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

The Results Jane Needs Long-term Care Nationwide pays LTC benefit to Trust ($10,000 per month) Jane borrows funds from trust to pay LTC expenses Jane dies just as LTC benefits are exhausted Estate Principal Debt is - $1,000,000 Accrued Interest Debt is- $ 352,000 Total Debt to Trust - $1,352,000 At Client’s Death Death claim filed – remaining death benefit of $4,000,000 is paid to trust Estate repays Principal - $1,000,000 Estate repays Accrued Loan - $ 352,000 Total Amount Repaid - $1,352,000 Estate has been drained of $1,352,000 This amount not subject to estate tax now Result: $4,000,000 + $1,352,000 Trust now has $5,352,000 Loan interest assumed to be 7%, HIPAA rare assumed to be at $10,000 per month, benefit paid 100 months FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Business Succession • Buy-sell agreements • LTC rider provides funds for installment sale • Buy-sell agreement should reflect this possible type of sale • Purpose of LTC rider is to protect the business • LTC rider used in traditional manner when partners buy each other’s policies • Key person insurance • LTC rider provides installment compensation for lost services • Purpose of LTC rider is to protect the business • Business may offer key person their own plan (via Sec. 162 Plan, etc.) FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Business Succession Business Value - $900,000 50/50 Ownership SamDave $450,000 $450,000 Sam has 2 ADLs Claim is filed Benefit check ($9,000) is sent monthly to Dave Dave sends $9,000 a month to Sam as part of buyout Dave buys out Sam in 4 yrs and 2 months FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Buy Sell/Business Succession • Tax Treatment • 7702B LTC riders • Benefit paid tax free to business/policy owner or corporation • 7702B references Sec.104 • Insured as first rights to tax free amounts • Remaining tax free amount and tax on excess of formula paid by business • 101(g) chronic illness riders • If death occurs, tax free death benefit • If Chronic Illness benefit is paid to business owner, benefit is taxable in excess of cost basis. • No aggregate LTC tax rules on insured apply FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Special Needs Trust • Purpose of a Special Needs Trust • Enhance quality of life for special needs person • Maintain federal, state and local benefits for special needs person • How much death benefit will be needed? • What goals need to be met? • Can vary greatly • Contradiction of adding LTC Rider • Most companies require LTC rider and DB to be equal • LTC benefit depletes Death Benefit • May leave little or nothing for the trust • Nationwide allows LTC to be dialed down to preserve DB • Even if LTC can be dialed down, it may be wise to separately address life/LTC need with special needs FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Charitable Giving • Why does client usually want to add LTC rider to a policy intended for charitable giving? • Tax deduction • Leave money to charity – AND • Have access to LTC benefits! • Can’t have it all • Gift should be given with full intent of charity receiving • Why would an LTC rider make sense? • LTC benefit paid earlier than mortality • Provides cash with more spending power • Indemnifying the key contributor • Example - Life expectancy 83, LTC needed at 75 • DB flows to charity 8 years early- enhances spend-ability FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Executive Benefits- Employee Owned • LTC rider works in executive-owned plans • Insurance-based retirement plans • Executive bonus (Sec. 162 plans) • Collateral split dollar • Cost of LTC may be less expensive when over funded • May allow more potential income from plan • LTC is reduction of death benefit, not withdrawal or loan • If policy does not reduce current cash value • Cash value may continue to grow when LTC is collected • If policy takes a pro-rata deduction from cash value (NY, KY, V.I.) • Still makes valuable addition- low cost on max funded • LTC benefit could be eliminated after period of withdrawals and loans FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Executive Benefits- Employer Owned • Deferred Compensation • Ruled by 409A • Has specific triggering events • LTC is not one of them • Advantage is to Corporation • If insured’s disability includes LTC triggers: • LTC benefit paid to Corporation • Corporation only obligated to separation amount • Remaining accelerated DB stays with Corp. • Taxation? • Does reference to Sec. 104 apply? Let CPA decide! FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

In Summary • LTC alternative products seem to be wave of the future • It is important to understand differentiators between products • Indemnity LTC riders can be used in “outside the box” scenarios and advanced case design • Nationwide is “on your side” with true 7702B LTC Rider that pays an indemnity-style benefit and can be added to a variety of individual life products with a variety of premium payment options FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)

Questions? Independent Dealer: 1-800-321-6064 Financial Institutions: 1-800-893-5399 Wirehouse/Regionals: 1-800-720-1511 Nationwide Agents: 1-888-333-4202 Nationwide Financial Network: 1-877-223-0795 Brokerage General Agency: 1-888-767-7373 FOR BROKER/DEALER USE ONLY—NOT FOR USE WITH THE PUBLIC NFM-9907AO.1 (09/12)