Download

1 / 28

280 likes | 450 Views

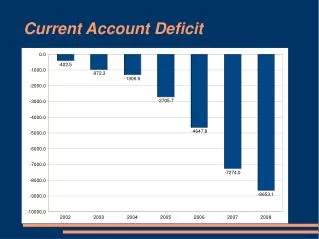

Indonesia’s current account challenge. Part 2 – Is there a current account problem?. Petar Vujanovic Head of Indonesia Desk OECD, Economic Department. Current Account. Current account in OECD and selected emerging economies. A big deterioration in Indonesia’s current account (% of GDP).

E N D

Indonesia’s current account challenge Part 2 – Is there a current account problem? Petar Vujanovic Head of Indonesia DeskOECD, Economic Department

Current account in OECD and selected emerging economies A big deterioration in Indonesia’s current account (% of GDP)

Current account in selected emerging economies Rapid deterioration in current account began in mid-2011

Exchange rate Depreciation of over 35% since beginning of 2012.

Current account components (USD) Higher oil deficit and lower non-oil & gas goods surplus

Current account components (USD) Goods imports stalled and big fall in goods exports (USD) since beginning of 2012.

Oil and gas – USD and Rupiah Denomination of trade (USD or rupiah) makes a difference.

Oil – net exports and price Oil price explains a big part of the growing oil deficit

Gas – net exports and price Gas price explains little of the (relatively modest) decline in gas exports (large trade surplus)

Trade – Non oil and gas goods exports Both manufactures and mineral commodity exports have declined

Trade – Manufactured exports Manufactured exports are quite diversified

Trade – Exports - Manufactures Percent reduction in value from Q2 2011 peak (% share)

Palm oil prices Palm oil prices have fallen over 30% since Q1 2011

Trade – Exports – Mining and other ~30% of all goods exports Percent reduction in value from ~Q4 2011 peak (% share)

Trade – metal prices (IMF) Metal prices have fallen over 30% since Q1 2011

Trade – thermal coal prices (IMF) Coal prices have fallen by around 30% since Q1 2011

Terms of trade …. In short – Indonesia has suffered a large decline in its terms of trade – and accelerated since beginning of 2011. Similar to other commodity-based economies, like Chile and Australia.

Trade – Goods and Service Imports (USD and local currency) Value of imports in local currency has been driven by depreciation. Volumes have been flat in recent quarters.

Trade – Goods and Service Imports (USD) Raw materials are the largest component

Trade – Raw material imports (USD) Processed industrial supplies are the largest component

Trade – Monthly trade balance The turn around in the trade balance continued in November.

National savings and investment Gross national savings and investment are now close to being equal

Capital account components Portfolio flows have been volatile; reserves accumulation has been important.

Reserves assets and the exchange rate Policy of rapid reserve accumulation fro 2008 while the rupiah strengthened helped to hold down the current account deficit.

Conclusion • There has been a big deterioration in the current account since the end of 2011. • This has contributed, at least in part, to a large depreciation in the Rupiah. • Decline in goods balance (non-oil and gas, and oil). • Commodity prices account for a large part of this – including crude oil, palm oil, coal, and many metals – end of the “super-cycle”. • A terms of trade shock – like other commodity exporters. • Imports of processed industrial supplies are a large component but flat (USD and volume) growth. • Savings excess over investment has disappeared. • Reserve asset transactions important in explaining capital account. • FDI flows have increased. Portfolio flows have been volatile.