Download

1 / 14

140 likes | 260 Views

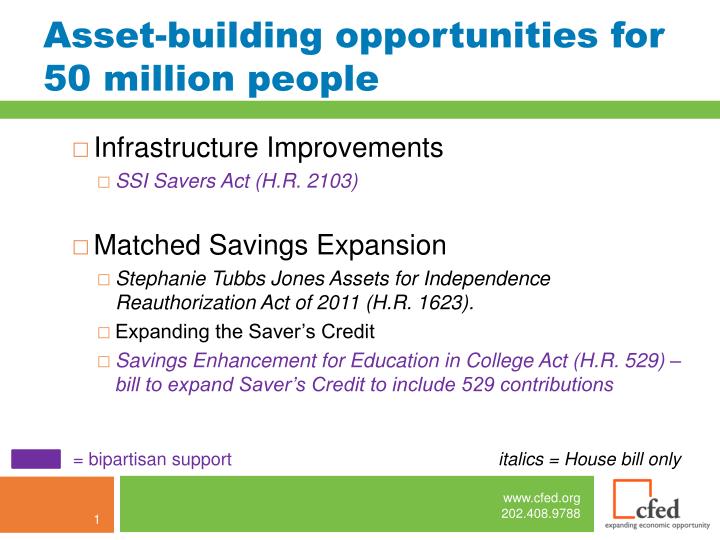

Asset-building opportunities for 50 million people. Infrastructure Improvements SSI Savers Act (H.R. 2103) Matched Savings Expansion Stephanie Tubbs Jones Assets for Independence Reauthorization Act of 2011 (H.R. 1623). Expanding the Saver’s Credit

E N D

Asset-building opportunities for 50 million people • Infrastructure Improvements • SSI Savers Act (H.R. 2103) • Matched Savings Expansion • Stephanie Tubbs Jones Assets for Independence Reauthorization Act of 2011 (H.R. 1623). • Expanding the Saver’s Credit • Savings Enhancement for Education in College Act (H.R. 529) – bill to expand Saver’s Credit to include 529 contributions = bipartisan support italics = House bill only

Asset Limits hurt Economic Self-Reliance • Forces many to stay unbanked or to spend down any savings to remain eligible for their benefits; • Prevents many recipients from saving for retirement or post-secondary education; • Limits opportunities for low-income people to save for homeownership; • If they have an emergency—a family member dies, a car breaks down, a roof needs repair—they are allowed little in savings to fall back on, leaving them vulnerable to predatory lenders and deeper poverty;

Asset Limit Reform: SSI Saver’s Act (H.R. 2103) • Sponsored by Congressman Petri (R-WI) and Congresswoman Tsongas (D-MA). • The bill would help people with disabilities save by: • Raising the asset limit to $5,000 for a single and $7,500 for joint filers and index these limits for inflation; • Excluding retirement savings up to $50,000 from inclusion in the asset test (<65 age) and up to $10,000 (>65 age); • Excluding IDAs and Education Savings Accounts for those under 65;

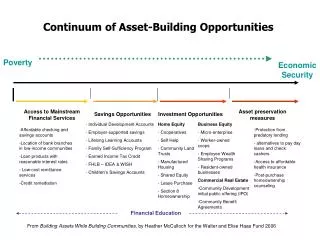

Savings through Incentives:Individual Development Accounts • Individual Development Accounts(IDAs) are special savings accounts that match the deposits of low- and moderate-income people. • IDAs are offered through partnerships between financial institutions (such as banks and credit unions) and local nonprofit organizations and requires savers to take financial education classes in order to receive match. • Matches are usually $1:$1 or $2:1. • Assets purchased using saver’s deposit + match are limited primarily to homeownership, higher education or business capitalization.

Assets for Independence (AFI) Program Facts • AFI is the primary source of federal funding for IDAs nationwide. • Many AFI projects offer services targeted to specific groups, including refugees/immigrants, victims of domestic violence, the homeless, and individuals with disabilities. • Tens of thousands of AFI savers have gone on to buy a home, attend college, or start a business. • IDA savers keep their homes and businesses and complete their college education

AFI Reauthorization • Stephanie Tubbs Jones Assets for Independence Reauthorization Act of 2011 (H.R. 1623) • Waivers included • Legislative Jurisdiction: • House: Ways and Means Committee • Senate: Health, Labor, Education and Pensions (HELP) Committee

AFI Reauthorization:Major Changes Simplification for Grantees • Lower the federal to non‐federal match rate from 1:1 to 2:1 to make it easier for grantees to raise local match. • Support training costs for grantees. Expand Participant Eligibility • Streamline income eligibility standards to include 80% of Adjusted Gross Income not to exceed $20,000 single, $30,000 head of household or $40,000 joint tax filer or 80% of Area Median Income, in addition to 200% federal poverty level. • Raise savings amount to $5,000/individuals and $10,000/families • Allow HHS the authority to waive any requirements found in the AFI legislation which would prohibit HHS from entering agreements with SSA.

AFI Reauthorization:Major Changes continued Definitions of Qualified Expenses • Expand qualified education expenses to include: • Include preparatory courses and professional licensing or certification examinations in education expenses • Room, board and transportation and 529 contributions • Expand the definition of qualified expenses for homeownership to include home repair and replacement of substandard homes including replacement of pre‐1976 mobile homes • Allow domestic violence survivors who jointly owned a home to qualify for homeownership

AFI Reauthorization:Proposed Changes continued Promote Research and Encourage Innovation: • Allow tribes and state or local governments to apply directly • Allow Indian Community Development Block Grant and the Native American Housing and Self‐Determination Act as match • Allow for automatic federal AFI funds for any statewide IDA program with an annual state appropriation of at least $250,000 • Demonstration projects targeting specific populations, whose circumstances have made their participation difficult, including foster youth, returning prisoners and working families • Raise the authorization limit from $25 million to $75 million

The Saver’s Credit • The Saver's Credit is a non-refundable tax credit available to eligible taxpayers who make salary-deferral contributions to their employer sponsored retirement plans (401(k), 403(b), SIMPLE, SEP or governmental 457 plan), and/or make contributions to their Traditional or Roth IRAs. • The current credit is between 10-50% of the individual's eligible contribution of up to $2,000, which means it cannot be more than $1,000. Double for couples.

The Saver’s Credit - current • Adjusted gross income must not exceed the following limits: • Lower the individual's AGI, the higher the saver's credit eligibility • Vastly underutilized – 50 million individuals eligible, but less than 6 million claim the credit

The Saver’s Credit – Proposed: (HR 1961/S. 3090 in 111th) • Indexes contribution limits for inflation and makes the credit refundable; • Expands the credit to additional middle‐income working families by raising the income eligibility for families from $55,500 in FY09 to $65,000; • Matches 50% of the first $1,000 of savings for families ($500 for individuals) earning <$65,000; • Automatically deposits matching funds into designated personal retirement accounts by using account information listed on IRS tax filings through IRS Form 8888 (HR 1961 only);

Saver’s Credit Expansion to 529 College Savings Accounts • Championed by Congresswoman Jenkins (R-KS) and Congressman Kind (D-WI). • The bill would: • Expand the existing Saver's Credit to contributions made to 529 college savings accounts • Allow the accounts to be used for computer purchases • Establish a modest new employer-matching program for college savings. • This bill does not make the credit refundable, thus it does not reach low-income and EITC-eligible households.

www.cfed.org www.cfed.org/go/advocacy Latest on legislation, track bills, send messages • Carol Wayman, Federal Policy Director, 202.207.0125, cwayman@cfed.org • Katherine Lucas, Policy Analyst, 202.408.9788, klucas-smith@cfed.org • Inemesit Imoh, Policy Associate, 202.207.0135, iimoh@cfed.org • Jessica Morales, Administrative Assistant, 202.207.0159, jmorales@cfed.org