Energy MLPs

Energy MLPs. Table of Contents. What is an MLP? Comparison to Income Trusts, REITs and Utilities Fundamental Risks to MLPs Energy MLPs Toll - Road Business Models Alerian MLP Index TM MLPs vs. Comparable Market Indices Alerian MLP Infrastructure Index TM

Energy MLPs

E N D

Presentation Transcript

Table of Contents What is an MLP? Comparison to Income Trusts, REITs and Utilities Fundamental Risks to MLPs Energy MLPs Toll - Road Business Models Alerian MLP IndexTM MLPs vs. Comparable Market Indices Alerian MLP Infrastructure IndexTM Investing in the Alerian MLP Infrastructure Index Alerian MLP Infrastructure Index - Historical Performance CIBC Contacts

What is an MLP? • Master Limited Partnerships (MLPs) • The current form of master limited partnerships (MLP) was created by US Congress in 1986. • A master limited partnership (MLP) is generally a limited partnership interest that is traded on a public exchange, and whose operations are managed by a general partner, the latter typically only has a 2% economic stake. • An interest in an MLP is referred to as a “unit” rather than a “share”. • MLPs typically pay out the bulk of their operating cash flow on a quarterly basis in the form of distributions (not dividends) to their limited and general partners. • As such, MLPs are relatively high-yielding securities whose primary objective is to grow cash distributions over time. • A MLP must derive most (~90%) of its cash flows from real estate, natural resources and commodities.

Comparison to Income Trusts, REITs and Utilities • MLPs vs. Income Trusts • Both are not taxed at the entity level and have historically had a high level of retail ownership. • The definition of an MLP in the U.S. tax code is very narrow whereas, the types of companies that were eligible for the Income Trust structure was quite broad, which encouraged abuse. • MLPs vs. REITS • Both yield-oriented equities that experienced rapid and substantial growth as retail investments. • The revenue of REITs is generally tied to the health of the overall economy and therein heavily exposed to downturns in the business cycle whereas the revenue of MLPs is generally tied to energy demand and federally mandated tariff increases, which reduces their exposure to downturns in the business cycle. • MLPs vs. Utilities • Both sectors benefit from inelastic demand and are closely regulated by the government. • Utilities are regulated at the local level, which tends to be more political with greater self-interest whereas interstate pipeline MLPs are regulated by the Federal Energy Regulatory Commission (FERC), which has historically shown a willingness to reassess the cost structure to support MLPs.

Fundamental Risks to MLPs • Regulatory Risk • The Federal Energy Regulatory Commission (regulates energy infrastructure assets) increasing the cost of capital, for example by lowering pipeline tariffs or create regulations which adversely affect a pipeline owned by an MLP. • Demand Destruction • Stagnation in energy demand (higher commodity prices, emission concern, alternative energy source, economic downturn, weather) • reduce volumes = lower cash generated • Supply side disruptions • Reduction in Middle Eastern supply, foreign embargos, terrorism • Weather, e.g. hurricanes. • Capacity issues – in instances where refinery source is less diversified. • Financial Risk • Interest rate – yield oriented nature of MLPs effectively creates duration risk. • Short term volatility as retail investors use only sentiment of equity and commodity markets without considering the impact on future cash flows to make decisions to hold/sell MLPs. • Environmental Accidents • Impact future cash flows as MLPs have low deductibles to cover any product spills. • Terrorism • Most MLPs do not carry any form of terrorism insurance (only carry business interruption insurance, typically effective after 30 days).

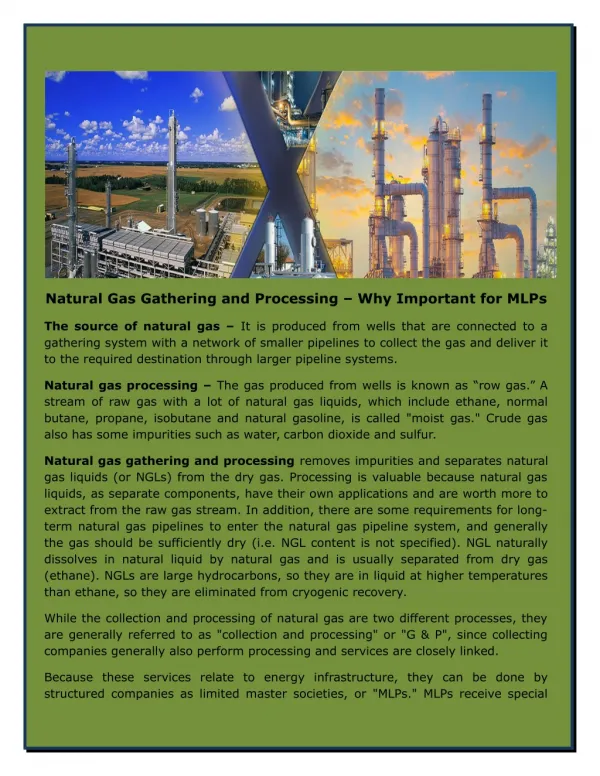

Energy MLPs • Based in the U.S., these limited partnerships are engaged in the transportation, storage, processing, exploration, and production of minerals and natural resources. • By confining their operations to these specific activities, they are able to trade on public securities exchanges without entity-level taxation. • Business models geared towards generating predictable cash flows based on: • long-lived, high-value physical assets. • Producer Price Index (PPI) revenue indexing, which provide predictable growth and a built-in inflation hedge. • substantial barriers to entry, which generate attractive organized investment opportunities. • strong operating leverage through hard assets that magnify inelastic demand. • 103 energy MLPs currently; • 3/4 of them trade on the NYSE. • The majority of the residual MLPs trades on the NASDAQ. • All listed MLPs are regulated by the Securities Exchange Commission and must comply with Sarbanes-Oxley Act. Data source: Alerian, Bloomberg as of 17 September 2013

Toll-Road Business Models • Typically toll-road business models • Receive a specified tariff for hauling a product over a certain distance. • Do not take title to the commodity. • Do not have balance sheet exposure. • Are largely agnostic to the level of commodity prices • underlying commodity prices do not enter the tariff calculation. • No significant credit risk as commodity prices increase.

Alerian MLP IndexTM • Alerian (www.alerian.com) is an independent company that provides MLP market intelligence, benchmarks, data sets and analytics that are used extensively by a range of stakeholders such as investment banks, stock exchanges, investment professionals, consultants, and MLPs. • Alerian MLP Index (NYSE:AMZ) measures the composite performance of the 50 most prominent energy MLPs. • Industry standard benchmark index for energy MLP sector. • Calculated using a float-adjusted, capitalisation-weighted methodology. • Total return index is available under ticker AMZX and is calculated on an end of day basis. Data source: Alerian website www.alerian.com

MLPs vs. Comparable Market Indices The S&P 500 is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy. The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry. Utilities are represented by the S&P 500 Utilities Index, a composite of utility stocks in the S&P 500. Real Estate Investment Trusts (REITs) are represented by the Real Estate 50 Index, a supplemental benchmark to the FTSE NAREIT US Real Estate Index Series to measure the performance of larger and more frequently traded equity REITs. Performance is provided on a total return basis. Data source: Bloomberg as of 28 June 2013

MLPs vs. Comparable Market Indices Master Limited Partnerships (MLPs) are represented by the Alerian MLP Infrastructure Index (AMZI). The S&P 500 is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy. The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 blue-chip stocks that are leaders in their industry. Utilities are represented by the S&P 500 Utilities Index, a composite of utility stocks in the S&P 500. Real Estate Investment Trusts (REITs) are represented by the Real Estate 50 Index, a supplemental benchmark to the FTSE NAREIT US Real Estate Index Series to measure the performance of more frequently traded equity REITs. Commodities are represented by the S&P Total Return World Commodity Index (SPWCITR). Non-US equities are represented by the MSCI Daily Total Return EAFE Index (NDDUEAFE). Small cap equities are represented by the Russell 2000 Index. Performance is provided on a total return basis. Annualized performance represents period from July 31, 2003 to July 31, 2013 Data source: Bloomberg as of 31 July 2013

Alerian MLP Infrastructure IndexTM • Alerian MLP Infrastructure IndexTM is liquid, midstream-focused subset of the AMZ. • Ticker NYSE:AMZI. • Launched March 2008. • Tracks the price return of 25 energy infrastructure assets. • Which earn the majority of their cash flow from the transportation, storage, and processing of energy commodities. • Calculated using a float-adjusted, capitalization-weighted methodology. • Total return index is available under ticker AMZIX and is calculated on an end of day basis. Data source: Alerian website www.alerian.com

Alerian MLP Infrastructure IndexTM Data source: Bloomberg as of 28 June 2013

Investing in the Infrastructure MLP Sector • Thematically, investment in this sector is an investment in the build out of the U.S. energy infrastructure over the next decade. • New infrastructure investment to keep pace with increasing population growth and shifting of North America’s traditional supply sources. • The United States requires over U.S.$200 billion of energy infrastructure investments over the next decade to match new supplies with growing demand, providing prolific investment opportunities. • Based on market capitalization, this sector represents about ~78% of the total MLP sector.

Alerian MLP Infrastructure Index – Historical Performance Data source: Bloomberg as of 28 June 2013

150 Cheapside London EC2V 6ET Dealing: +44 (0)20 7234 6955 Direct: +44 (0)20 7234 6009 Fax: +44 (0)20 7234 6254 150 Cheapside London EC2V 6ET Dealing: +44 (0)20 7234 6955 Direct: +44 (0)20 7234 6002 Fax: +44 (0)20 7234 6254 150 Cheapside London EC2V 6ET Dealing: +44 (0)20 7234 6955 Direct: +44 (0)20 7234 7168 Fax: +44 (0)20 7234 6254 150 Cheapside London EC2V 6ET Dealing: +44 (0)20 7234 6955 Direct: +44 (0)20 7234 7160 Fax: +44 (0)20 7234 6254 Martina Ben-Shaul Executive Director martina.ben-shaul@cibc.co.uk Vina Lad Executive Director vina.lad@cibc.co.uk Eduardo Montero Larraz Executive Director eduardo.montero@cibc.co.uk Vuk Kalezic Director vuk.kalezic@cibc.co.uk CIBC Contacts 150 Cheapside London EC2V 6ET Dealing: +44 (0)20 7234 7823 Direct: +44 (0)20 7234 7230 Fax: +44 (0)20 7234 6254 150 Cheapside London EC2V 6ET Dealing: +44 (0)20 7234 6955 Direct: +44 (0)20 7234 7230 Fax: +44 (0)20 7234 6254 Loli Spinola Director loli.spinola@cibc.co.uk Thomas Pellequer Executive Director Head of Continental European Sales thomas.pellequer@cibc.co.uk

Disclaimers This confidential presentation (the “Presentation”) has been prepared by CIBC World Markets plc and Canadian Imperial Bank of Commerce, London Branch solely for informational and discussion purposes and may not be divulged to any person or entity or reproduced, disseminated or disclosed, in whole or in part. By attending or accepting this Presentation, each recipient agrees that CIBC shall have no liability for any representations (express or implied) or warranties contained in, or for any omissions from, this Presentation. The information and any illustrative examples contained herein do not purport to be all-inclusive or to contain all of the information that may be material to any analogous situation and each recipient of the information and data contained herein should perform its own independent investigation and analysis in relation to such information and any subsequent transaction. The information and any data contained herein are not a substitute for the recipient’s independent evaluation and analysis and should not be considered as a recommendation to any recipient to participate in any transaction. Nothing in this Presentation is or should be construed as an offer or commitment of financing by CIBC and all and any financing structures remain subject to customary due diligence and documentation. This Presentation may include certain statements, estimates and projections. Any such statements, estimates and projections reflect various assumptions concerning anticipated results and have been included solely for illustrative purposes. No representations are made as to the accuracy of any such statements, estimates or projections or with respect to any other materials herein and none of the aforementioned should be relied upon as a warranty of future performance. Actual results may vary materially from the estimates and projected results contained herein. This communication is directed only at (i) "investment professionals" as defined in Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005; or (ii) high net worth bodies corporate, unincorporated associations and partnerships and trustees of high value trusts as described in Article 49. Any investment or investment activity to which this communication relates is only available to and will only be engaged in with such persons and persons who receive this communication who do not fall within (i) or (ii) above should not rely on or act upon this communication. CIBC World Markets plc is a wholly-owned subsidiary of Canadian Imperial Bank of Commerce and part of Canadian Imperial Bank of Commerce’s wholesale banking arm which also includes: CIBC World Markets Inc., CIBC World Markets Corp, CIBC World Markets Securities Ireland Limited, CIBC Australia Ltd, and CIBC World Markets (Japan) Inc, which are together referred herein as "CIBC".