Download

1 / 34

340 likes | 517 Views

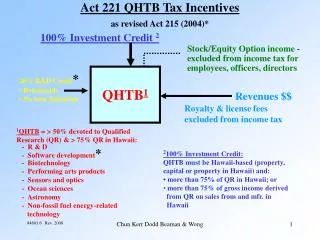

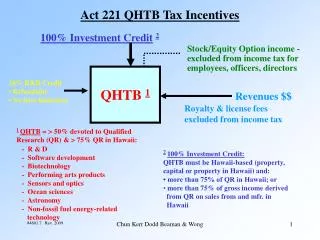

Act 221 QHTB Tax Incentives . 100% Investment Credit 2. Stock/Equity Option income - excluded from income tax for employees, officers, directors. QHTB 1. 20% R&D Credit • Refundable • No base limitation. Revenues $$. Royalty & license fees excluded from income tax.

E N D

Act 221 QHTB Tax Incentives 100% Investment Credit2 Stock/Equity Option income - excluded from income tax for employees, officers, directors QHTB 1 20% R&D Credit • Refundable • No base limitation Revenues $$ Royalty & license fees excluded from income tax 1QHTB = > 50% devoted to Qualified Research (QR) & > 75% QR in Hawaii: - R & D - Software development - Biotechnology - Performing arts products - Sensors and optics - Ocean sciences - Astronomy - Non-fossil fuel energy-related technology • 2100% Investment Credit: • QHTB must be Hawaii-based (property, • capital or property in Hawaii) and: • • more than 75% of QR in Hawaii; or • more than 75% of gross income derived • from QR on sales from and mfr. in • Hawaii Chun Kerr Dodd Beaman & Wong

Non-QHTB Tax Incentives • Enterprise Zones • Income tax holiday • GET holiday • Property tax holiday • UI holiday • General Excise Tax Exemptions • Exports • Scientific contracts • • Capital goods excise tax credit—4% taken off income tax • •Pyramiding relief phased in • Related Party Exemptions • 4% Hi-tech Renovation Credit (added 2001) • hi-speed telecom • security • environmental • electrical power Movie Production Credit Renewable Energy Tax Credit ForeignTrade Zone Chun Kerr Dodd Beaman & Wong

Hawaii High Technology Initiatives (Act 221) • In order to encourage the growth of high technology businesses in Hawaii, the legislature has provided a number of tax incentives for qualified high technology businesses (QHTBs): • 100% high technology investment tax credit for investors (ITCs) • Refundable 20% tax credit for research expenditures (R&D credit) [Act 215] • Income tax exclusion for (a) royalties and (b) stock-related transactions • Increase capital loss carryforward period Chun Kerr Dodd Beaman & Wong

Qualified High Technology Business (QHTB) • Definition: • A business, employing or owning capital or property, or maintaining an office, in Hawaii provided that: • > 50% of its total business is in qualified research and > 75% of its qualified research is performed in Hawaii (Activity test) or • > 75% of its gross income is derived from qualified research and the income is received from (1) products sold from, manufactured in, or produced in Hawaii or (2) services performed in Hawaii (Income test) Chun Kerr Dodd Beaman & Wong

QHTB • “Qualified research” • Research and development under Internal Revenue Code Section 41 • Computer software development for sale or license • Biotechnology • Performing arts products • Sensors and optics • Ocean sciences • Astronomy • Non-fossil fuel energy-related technology Chun Kerr Dodd Beaman & Wong

QHTB(con’t.) • Businesses should obtain a QHTB comfort ruling from the State of Hawaii Department of Taxation to ensure that they qualify as a QHTB • Form A-9 (Request for a High Tech Comfort Ruling) • See Hawaii Tax Department’s website (http://hawaii.gov/tax/) • Fee: $1,000 Chun Kerr Dodd Beaman & Wong

QHTB(con’t.) • Annual information return filing requirement • Form N-317 (Statement by a Qualified High Technology Business) • Tax year 2006 and prior years • Paper form due on April 20 following the tax year • Tax year 2007 and forward (Act 206) • Online form on the Hawaii Tax Department’s website • Due before June 30 following the tax year • $1,000 per month penalty for failure to file ($6,000 max) • Effective: July 1, 2007 (applies to investments received after June 30, 2007) Chun Kerr Dodd Beaman & Wong

High technology business investment tax credit (ITC) • Tax incentive for investors in a QHTB • Nonrefundable 100% income tax credit on investments made into a QHTB • Limited to $2 million per QHTB per year • Claimed over a five year period • First year - 35% (up to $700,000) • Second year - 25% (up to $500,000) • Third year - 20% (up to $400,000) • Fourth year - 10% (up to $200,000) • Fifth year - 10% (up to $200,000) • Effective 2001 - 2010 Chun Kerr Dodd Beaman & Wong

Investments made before May 1, 2009 - ability to allocate ITC to provide multiple credits Hawaii tax- averse partners Tax-indifferent partners* $1M Allocate full $2M ITC** $1M Special Purpose Partnership or LLC $2M *Usually obtains more equity interest in partnership or LLC to compensate for giving up credits HAWAII QHTB **Allocation allowed by statute: HRS Section 235-2.45(d) Chun Kerr Dodd Beaman & Wong

Limitation on allocating ITC to provide multiple credits[TIR 2007-02] • For each dollar invested, if the ITC allocation ratio to an investor IsThen <1.5 Hawaii tax department will not challenge because of safe harbor 1.5 - 2 Hawaii tax department may challenge for economic substance or business purpose - Safe harbor available if satisfies both tests: (1) no frontloading of credits test and (2) limited equity shifting test >2 Taxpayers are required to substantiate by proving economic substance and business purpose Chun Kerr Dodd Beaman & Wong

Investments made on or after May 1, 2009 [Act 178 (2009)] • Limitations • For tax years ending on or before December 31, 2010, not more than 80% of a taxpayer's tax liability may be offset by utilizing the ITC; • The ITC may not exceed an allocation ratio of 1:1 for each investor; and • Credits that are unused during tax years ending on or before December 31, 2009 or December 31, 2010 cannot be carried forward. • See Taxation Announcements 2009-23 (August 3, 2009) and 2009-27 (September 14, 2009) for more information. Chun Kerr Dodd Beaman & Wong

Filing requirements to claim ITC[Act 215] • Three step process: • Taxpayer files for certification • Form N-318A (Statement of Investment in a Qualified High Technology Business) • Due March 30 following the tax year • Fee: • Filed by investor ($100 early filing; $150 regular filing) • Filed by QHTB on investors’ behalf ($750 early filing; $1,000 regular filing) • Tax Department sends “approval” to taxpayer • Form N-318A page 2 • Taxpayer attaches “approval” to tax return (claim) with Form N-318 (High Technology Business Investment Tax Credit) • The claim for the ITC must be made within 12 months following the close of the tax year Chun Kerr Dodd Beaman & Wong

Tax credit for research activities (R&D credit) • Tax incentive available to QHTBs • Refundable 20% tax credit on qualified research expenditures • Standard to qualify is the same as federal R&D credit except: • No base amount limitation so credit applies to all qualified research expenditures, not just on the amount of increase • Research must be performed in Hawaii • Effective 2001 - 2010 Chun Kerr Dodd Beaman & Wong

R&D Credit • Qualified research expenses are limited to expenditures for: • Employee wages (Hawaii W-2) • Supplies (nondepreciable tangible personal property consumed in Hawaii) • Contract research (services performed in Hawaii by 3rd parties) Chun Kerr Dodd Beaman & Wong

Changes to R&D credit • With the enactment of Act 215, some changes were made: • Change in the definition of computer software development • Taxpayers must now intend to ultimately sell, license, or otherwise market the software for economic consideration • Taxpayers must have substantial rights to the intellectual property • Elimination of the liberal construction language • [Old language] It is the intention of the legislature that the amendments in this Act be liberally construed. • [New language] It is the intention of the legislature that the amendments in this Act be construed in a manner consistent with the intent of this Act. Chun Kerr Dodd Beaman & Wong

Filing requirements for claiming the R&D credit [Act 215] • Three step process: • Taxpayer files for certification • Form N-319A (Statement of Research and Development Costs) • Due March 30 following the tax year • Fee: ($400 early filing; $750 regular filing) • Tax Department sends “approval” to taxpayer • Form N-319A page 2 • Taxpayer attaches “approval” to tax return (claim) with Form N-319 (Credit for Research Activities) • The claim for the R&D credit must be made within 12 months following the close of the tax year Chun Kerr Dodd Beaman & Wong

QHTB stock rights income tax exclusion • Tax incentive for investors of QHTBs • Income tax exemption available for • Income earned and proceeds derived from QHTB stock options or stock; and • Income earned from stock of parent company of QHTB. The parent company must possess 80% of the total voting power of the stock or other interest in the QHTB, and 80% of its total value. Chun Kerr Dodd Beaman & Wong

QHTB royalty income tax exclusion • Tax incentive available to QHTBs • Income tax exclusion available for royalties earned on intellectual property developed and owned by the QHTB Chun Kerr Dodd Beaman & Wong

Other QHTB incentives • Capital loss carryovers • Instead of 5 years, QHTBs may carry forward capital losses for 15 years Chun Kerr Dodd Beaman & Wong

Summary of QHTB formation/operation • Initial steps • Form QHTB and related entities • Obtain QHTB comfort ruling from Hawaii Tax Department • Operations • Investor invests money into special purpose entity or QHTB to generate ITC • QHTB conducts operations to generate R&D credit, if applicable, and other tax credits Chun Kerr Dodd Beaman & Wong

Non-QHTB Incentives • Income tax (note: multiple credits may not be claimed on the same expenditures) • Renewable energy technologies income tax credit • Technology infrastructure renovation income tax credit • Capital goods excise tax credit • General excise tax • Exemption for related party transactions Chun Kerr Dodd Beaman & Wong

Renewable energy technologies income tax credit • Nonrefundable or alternatively, refundable, income tax credit for every renewable energy technology system installed and placed in service in Hawaii Chun Kerr Dodd Beaman & Wong

Renewable energy technologies income tax credit(con’t.) Property placed in service before July 1, 2009 • Credit amount • Solar thermal energy system • Single family residential property • 35% of actual cost or $2,250, whichever is less • Multi-family residential property • 35% of actual cost or $350 per unit, whichever is less • Commercial property • 35% of actual cost or $250,000, whichever is less Chun Kerr Dodd Beaman & Wong

Renewable energy technologies income tax credit(con’t.)Property placed in service before July 1, 2009 • Wind-powered energy systems • Single family residential property • 20% of actual cost or $1,500, whichever is less • Multi-family residential property • 20% of actual cost or $200 per unit, whichever is less • Commercial property • 20% of actual cost or $500,000, whichever is less • Photovoltaic energy systems • Single family residential property • 35% of actual cost or $5,000, whichever is less • Multi-family residential property • 35% of actual cost or $350 per unit, whichever is less • Commercial property • 35% of actual cost or $500,000, whichever is less Chun Kerr Dodd Beaman & Wong

Renewable energy technologies income tax credit (con’t.) [Act 204]Property placed in service before July 1, 2009 • No credit for single family residential solar thermal energy systems for homes with a building permit on or after January 1, 2010 • No credit for residential home developer who installs and places into service a system in 2009 Chun Kerr Dodd Beaman & Wong

Renewable energy technologies income tax credit(con’t.)Property placed in service on or after July 1, 2009 • Credit amount • Solar energy systems* • Single family residential property • 35% of actual cost or $2,250 per system, whichever is less, for systems used primarily for household use • 35% of actual cost or $5,000 per system, whichever is less, for systems not used primarily for household use[1] • Multi-family residential property • 35% of actual cost or $350 per unit per system, whichever is less * Act 154 (2009) removed the categories “solar thermal energy systems” and “photovoltaic energy systems” that existed under the earlier statute and created a single category called “solar energy systems.” [1] Subject to further reduction if used to satisfy the substitute renewable energy technology requirement for building permit purposes under HRS § 195-6.5(a). Chun Kerr Dodd Beaman & Wong

Renewable energy technologies income tax credit(con’t.)Property placed in service on or after July 1, 2009 • Commercial property • 35% of actual cost or $250,000 per system, whichever is less, for systems used primarily for household use • 35% of actual cost or $500,000 per system, whichever is less, for systems not used primarily for household use • Wind-powered energy systems • Single family residential property • 20% of actual cost or $1,500 per system, whichever is less[1] • Multi-family residential property • 20% of actual cost or $200 per unit per system, whichever is less • Commercial property • 20% of actual cost or $500,000 per system, whichever is less [1] Subject to further reduction if used to satisfy the substitute renewable energy technology requirement for building permit purposes under HRS § 195-6.5(a). Chun Kerr Dodd Beaman & Wong

Renewable energy technologies income tax credit (con’t.)Property placed in serviceon or after July 1, 2009 • No credit for single family residential renewable energy technology systems for homes with a building permit on or after January 1, 2010. • Residential home developers may now claim the credit. Chun Kerr Dodd Beaman & Wong

Renewable energy technologies income tax credit (con’t.)Property placed in serviceon or after July 1, 2009 • For tax years beginning on or after January 1, 2009, a taxpayer can claim a refundable credit under the following circumstances: (1) the taxpayer reduces his or her solar energy credit claim by 30% and elects to claim the credit as a refundable credit or (2) the taxpayer (a) receives solely pension income or (b) has an AGI of $20,000 ($40,000 for married filing jointly) or less and elects to claim the credit (either solor energy or wind) as a refundable credit. Chun Kerr Dodd Beaman & Wong

Technology renovation infrastructure income tax credit • Nonrefundable 4% income tax credit for renovation costs of commercial buildings in Hawaii to enable • high speed telecommunication, • physical security systems, • environmental systems, and • backup and emergency electrical systems. Chun Kerr Dodd Beaman & Wong

Technology renovation infrastructure income tax credit(con’t.) • Act 178 (2009) update • For renovation costs incurred on or after May 1, 2009 and on or before December 31, 2010, the credit may only offset up to 80% of a taxpayer's tax liability. Also, if these credits are not used during tax years ending on or before December 31, 2009 or December 31, 2010, they cannot be carried forward. Chun Kerr Dodd Beaman & Wong

Capital goods excise tax credit • 4% refundable income tax credit for eligible depreciable tangible personal property placed in service and used by the taxpayer in a trade or business • The claim for the credit must be made within 12 months following the close of the tax year Chun Kerr Dodd Beaman & Wong

Capital goods excise tax credit(con’t.) • Act 178 (2009) update • The credit is suspended for property placed in service on or after May 1, 2009 and on or before December 31, 2009. • Note: proposed legislative changes in 2010 to further suspend or revoke of this credit should be closely monitored. Chun Kerr Dodd Beaman & Wong

Exemption for related party transactions • General excise tax exemption for related party transactions such as: • interest on intercompany loans, • legal and accounting services, • use of computer software or hardware, • information technology services, • database management, and • managerial and administrative services. Chun Kerr Dodd Beaman & Wong