Download

1 / 12

120 likes | 142 Views

The Commissioner ensures that employees of the Internal Revenue Service act in accordance with taxpayer rights, including the right to information, quality service, fair tax payment, challenge, appeal, finality, privacy, confidentiality, representation, and a just tax system.

E N D

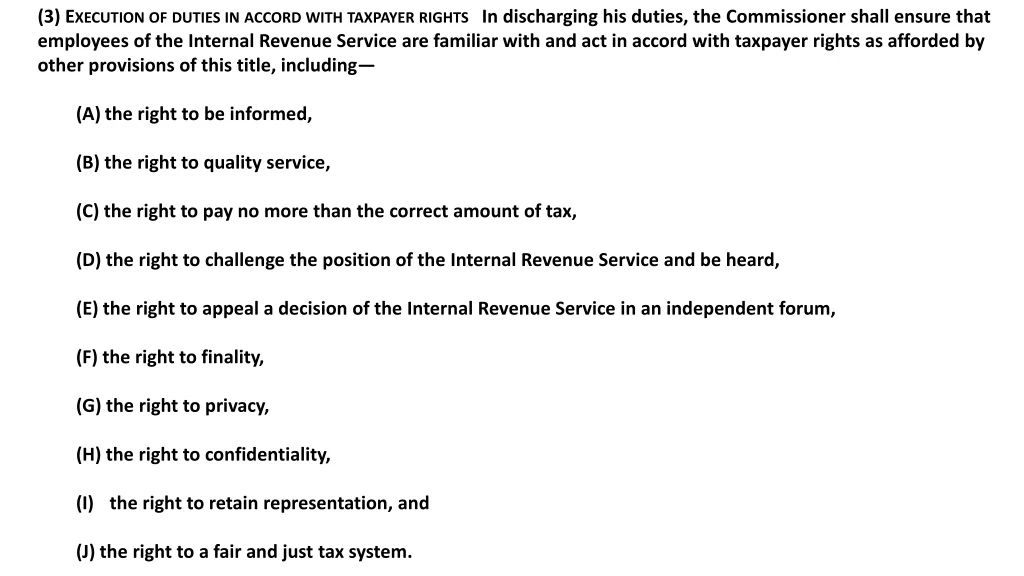

(3) Execution of duties in accord with taxpayer rights In discharging his duties, the Commissioner shall ensure that employees of the Internal Revenue Service are familiar with and act in accord with taxpayer rights as afforded by other provisions of this title, including— • the right to be informed, • (B) the right to quality service, • (C) the right to pay no more than the correct amount of tax, • (D) the right to challenge the position of the Internal Revenue Service and be heard, • (E) the right to appeal a decision of the Internal Revenue Service in an independent forum, • (F) the right to finality, • (G) the right to privacy, • (H) the right to confidentiality, • the right to retain representation, and • (J) the right to a fair and just tax system.

(3) Execution of duties in accord with taxpayer rights In discharging his duties, the Commissioner shall ensure that employees of the Internal Revenue Service are familiar with and act in accord with taxpayer rights as afforded by other provisions of this title, including— • the right to be informed, • (B) the right to quality service, • (C) the right to pay no more than the correct amount of tax, • (D) the right to challenge the position of the Internal Revenue Service and be heard, • (E) the right to appeal a decision of the Internal Revenue Service in an independent forum, • (F) the right to finality, • (G) the right to privacy, • (H) the right to confidentiality, • the right to retain representation, and • (J) the right to a fair and just tax system.

(3) Execution of duties in accord with taxpayer rights In discharging his duties, the Commissioner shall ensure that employees of the Internal Revenue Service are familiar with and act in accord with taxpayer rights as afforded by other provisions of this title., including— • the right to be informed, • (B) the right to quality service, • (C) the right to pay no more than the correct amount of tax, • (D) the right to challenge the position of the Internal Revenue Service and be heard, • (E) the right to appeal a decision of the Internal Revenue Service in an independent forum, • (F) the right to finality, • (G) the right to privacy, • (H) the right to confidentiality, • the right to retain representation, and • (J) the right to a fair and just tax system.

(3) Execution of duties in accord with taxpayer rights In discharging his duties, the Commissioner shall ensure that employees of the Internal Revenue Service are familiar with and act in accord with taxpayer rights as afforded by other provisions of this title, including— • the right to be informed, • (B) the right to quality service, • (C) the right to pay no more than the correct amount of tax, • (D) the right to challenge the position of the Internal Revenue Service and be heard, • (E) the right to appeal a decision of the Internal Revenue Service in an independent forum, • (F) the right to finality, • (G) the right to privacy, • (H) the right to confidentiality, • the right to retain representation, and • (J) the right to a fair and just tax system.

(3) Execution of duties in accord with taxpayer rights In discharging his duties, the Commissioner shall ensure that employees of the Internal Revenue Service are familiar with and act in accord with taxpayer rights as afforded by other provisions of this title, including— • the right to be informed, • (B) the right to quality service, • (C) the right to pay no more than the correct amount of tax, • (D) the right to challenge the position of the Internal Revenue Service and be heard, • (E) the right to appeal a decision of the Internal Revenue Service in an independent forum, • (F) the right to finality, • (G) the right to privacy, • (H) the right to confidentiality, • the right to retain representation, and • (J) the right to a fair and just tax system.

Cort v. Ash • “First, is the plaintiff ‘one of the class for whose especial benefit the statute was enacted’ . . .?” • “Second, is there any indication of legislative intent, explicit or implicit, either to create such a remedy or to deny one?” • “Third, is it consistent with the underlying purposes of the legislative scheme to imply such a remedy for the plaintiff?” • “[Fourth], is the cause of action one traditionally relegated to state law, in an area basically of concern of the the States, so that it would be inappropriate to infer a cause of action based solely on federal law?”

Cort v. Ash √ • “First, is the plaintiff ‘one of the class for whose especial benefit the statute was enacted’ . . .?” • “Second, is there any indication of legislative intent, explicit or implicit, either to create such a remedy or to deny one?” • “Third, is it consistent with the underlying purposes of the legislative scheme to imply such a remedy for the plaintiff?” • “[Fourth], is the cause of action one traditionally relegated to state law, in an area basically of concern of the the States, so that it would be inappropriate to infer a cause of action based solely on federal law?”

Cort v. Ash √ • “First, is the plaintiff ‘one of the class for whose especial benefit the statute was enacted’ . . .?” • “Second, is there any indication of legislative intent, explicit or implicit, either to create such a remedy or to deny one?” • “Third, is it consistent with the underlying purposes of the legislative scheme to imply such a remedy for the plaintiff?” • “[Fourth], is the cause of action one traditionally relegated to state law, in an area basically of concern of the the States, so that it would be inappropriate to infer a cause of action based solely on federal law?” √

Cort v. Ash √ • “First, is the plaintiff ‘one of the class for whose especial benefit the statute was enacted’ . . .?” • “Second, is there any indication of legislative intent, explicit or implicit, either to create such a remedy or to deny one?” • “Third, is it consistent with the underlying purposes of the legislative scheme to imply such a remedy for the plaintiff?” • “[Fourth], is the cause of action one traditionally relegated to state law, in an area basically of concern of the the States, so that it would be inappropriate to infer a cause of action based solely on federal law?” ? ? √

Words Matter • Congress explicitly used the language of rights • Congress used language that familiarly invokes rights anchored in procedural and substantive justice • Congress used the language of standards

Cort v. Ash √ • “First, is the plaintiff ‘one of the class for whose especial benefit the statute was enacted’ . . .?” • “Second, is there any indication of legislative intent, explicit or implicit, either to create such a remedy or to deny one?” • “Third, is it consistent with the underlying purposes of the legislative scheme to imply such a remedy for the plaintiff?” • “[Fourth], is the cause of action one traditionally relegated to state law, in an area basically of concern of the the States, so that it would be inappropriate to infer a cause of action based solely on federal law?” ? ? √

Cort v. Ash √ • “First, is the plaintiff ‘one of the class for whose especial benefit the statute was enacted’ . . .?” • “Second, is there any indication of legislative intent, explicit or implicit, either to create such a remedy or to deny one?” • “Third, is it consistent with the underlying purposes of the legislative scheme to imply such a remedy for the plaintiff?” • “[Fourth], is the cause of action one traditionally relegated to state law, in an area basically of concern of the the States, so that it would be inappropriate to infer a cause of action based solely on federal law?” √ √ √