Download

1 / 36

360 likes | 516 Views

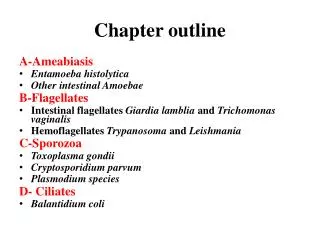

Chapter 21 explores critical strategies for repositioning funds, essential for optimizing working capital management. It discusses constraints on transferring funds, including political risks and tax implications. Key transfer methods are analyzed, such as dividends, royalties, and transfer pricing. The chapter also delves into the challenges posed by blocked funds and offers potential solutions, including fronting loans and negotiating with local governments. You'll gain insights into balancing accounts payable and short-term debt while understanding the advantages and disadvantages of centralized depositories in multinational operations.

E N D

OUTLINE FOR CHAPTER 21 • Understand Repositioning of Funds • Constraints on Moving of Funds • Ways to Transfer Funds • Unbundling • What to do if Funds are blocked • Aspects of Working Capital Management • Advantages and Disadvantages of a Centralized Depository • Netting (bilateral and multilateral) • Accounts Payable vs. Short-Term Debt

Chapter 21 – Working Capital Management • Managing current assets and current liabilities as well repositioning funds. • Repositioning funds - Moving Funds from one country to another or from one currency to another

Why Reposition Funds • For tax Reasons- locate profits in low-tax environments • To move funds to areas with greater profit potential • To move funds out of areas of economic or political problems • To move funds from countries that have exchange controls

Constraints on Positioning Funds • Usually assumed for a domestic firm there is no problem in moving funds from one affiliate to another • However for multinational firms there are often problems in moving funds

Constraints - Continued • 1) Political (examples - inconvertible currency, exchange controls and dividends and other remittances heavily taxed or limited in amount) • 2) Taxes (example withholding) • 3) Transaction costs (small / unit but add up over a year) • 4) Liquidity needs (banks want firms to keep a portion of their funds at their banks)

Unbundling • Many firms transfer funds in many ways (unbundle the package) as opposed to transferring funds in only one way (often through dividends) • It may be more acceptable politically to transfer funds in multiple ways (a firm would not want to make too large of a dividend payment)

Ways to Transfer Funds • 1) Dividends • 2) License fees, royalties, overhead and loans • 3) Transfer pricing • 4) Leads and lags (discussed earlier)

Dividends - Considerations • 1) Taxes - complicated • withholding taxes • in Germany, different tax rates on retained vs. distributed earnings (which are lower) • countries have different tax rates • countries often give tax credits for foreign income taxes

Dividend Considerations - Continued • 2) Political risk (for example, if a host country is very risky the parent may want more dividends declared by the subsidiary) • 3) Impending devaluation (would want subsidiary to speed up payables to the parent) • 4) Availability of funds (are the funds available to declare a dividend)

Dividend Considerations - Continued • 5) Joint venture partner (presence of a partner may dictate a defendable dividend policy - joint venture partner will want his/her proper share of the profits)

Royalties, Fees, Overhead and Loans - Considerations • A parent can charge its subsidiaries for the use of technology, patents, trade names etc. • Funds can effectively be transferred by over or undercharging from their true cost • Royalties, fees, etc. are usually locally tax deductible while dividends are not tax deductible

Transfer Pricing • Price one unit of a company charges another unit of the company for goods or services • The higher the price the more money the unit keeps and if the amount is above the “true” price this would amount to a transfer of funds • A major consideration for transfer pricing in addition to positioning of funds is the income tax effect

Example of Income Tax Effect on Transfer Pricing • Parent’s tax rate - 40% • Sub’s tax rate - 30% • Parent buys finished goods from the sub • Parent sells one good for $200 • Cost of goods sold for one unit is $100

Transfer Price Examples • Principle: All things being equal, want to show as much profit as possible in country with the lowest tax rates

Transfer Pricing - Tax Considerations • U.S. Section 482 “suggest” using an arm’s- length price (price one independent unit would charge another independent unit) • IRS - 3 methods to establish arm’s-length price (in order) • Comparable uncontrolled prices (market price) • Resale price method (final price - markup) • Cost-Plus method (full cost + markup)

Other Considerations on Transfer Pricing • 1) Tariffs (if a company pays a percentage of the transfer price would want, all things being equal, a low transfer price) • 2) Transfer pricing may make it difficult to judge performance of subsidiaries • 3) Transfer price should be fair to joint venture partner

Blocked Funds • Governments can limit transfers of foreign exchange of the country (examples - prior approval is needed to transfer and governments can make a currency inconvertible)

Moving Blocked Funds • 1) Use techniques discussed earlier for moving funds • 2) Fronting loans • 3) Creating unrelated exports • 4) Obtaining special dispensation (bargain for a special deal with the local government)

Fronting Loan loan • Instead of Parent Sub International Bank deposit loan Parent Sub

Fronting Loan - Continued • Bank “fronts” for the company (note bank has 100% collateral) • A government will more likely allow payment under the fronting loan than under the straight loan because its reputation will be hurt more if it does not allow a company to repay a major international bank • In many cases bank may be from a neutral country

Creating Unrelated Exports • Examples: • Locate a R&D facility in a country that blocks funds (in this case pay expenses in local currency) • Have a big party (again pay expenses in local currency)

Primary Purposes for Holding Cash Balances • 1) Transaction needs • 2) Precautionary reasons

Centralized Depository • Affiliates hold minimum cash for transactions and none for precautionary purposes • Excess cash for each affiliate is remitted to depository • Central depository invests excess funds for all subs and borrows if needed

Advantages of a Depository • Information advantage • the staff should know more about investment and borrowing opportunities worldwide than the financial manager at local subsidiary. • Also the more money they handle the better the information they should be able to obtain. • Also being located in a major financial center, it should have in general access to good and timely information.

Advantages - Continued • Total precautionary balance for company as a whole will be less than if each subsidiary holds its own balances (portfolio effect) • With a depository should not run into the situation that one sub is borrowing money (at a high rate) while another sub is investing money at a bank (at a low rate) • The depositories should locate in major money centers or other places that have major advantages.

Disadvantage to the Centralized Depository • It would require funds to set up and also to continually maintain

Netting • The table on the next slide represents the payment schedule for a month for a company with four subsidiaries or one parent and three subsidiaries • In this case sub C owes sub A $2 and sub A owes sub C $3

Paying Subsidiaries Receiving Subsidiaries

Netting - Continued • The worst system would be for each sub to pay the gross amount to all of the other subs (for example sub A pays $3 to sub C and sub C pays $2 to sub A) - this would result in a total of 12 transactions • Better to have bilateral netting - for example, sub A would pay sub C $1 (6 transactions)

Netting - Continued • If every sub paid or received from a central pool there would be only four transactions - for example, sub A would receive $1 from the pool • The best arrangement would be for the director of the pool to tell sub B to pay sub A $1 and sub D to pay sub C $2. This would involve only 2 transactions

Netting - Continued • Multilateral netting cuts down on the number of transactions as well as the $ amount of each transaction • Some countries don’t allow netting (want to help local banks)

Accounts Payable vs. Short-Term Debt • Many times a company (domestic or foreign) will get a discount if it pays early. • For example, credit terms of 5/10 net 50 means that if you pay in the first 10 days you only pay 95% of the bill or if you wait and pay in 50 days the entire amount of the bill is due.

Accounts Payable vs. Short-Term Debt - Continued • So if you don’t take the discount, you would in effect be borrowing $95 and agree to payback $100, an interest rate of 5.26% (5/95) for 40 days (50-10). Assuming 365 days in a year, the number of times 40 goes into 365 is 9.125 • The yearly interest rate would be (1.0526)9.125 -1 = 59.6 %

Accounts Payable - Continued • So take the discount even if short-term rates are lower than 59.6 % p.a.