Download

1 / 11

110 likes | 317 Views

The assumption of maximizing behavior lies at the heart of economic analysis. Firms are assumed to maximize economic profit. Economic profit is the difference between total revenue and total costs. Cost used in the calculation of economic profit are opportunity costs.

E N D

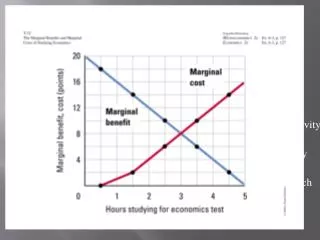

The assumption of maximizing behavior lies at the heart of economic analysis. Firms are assumed to maximize economic profit. Economic profit is the difference between total revenue and total costs. Cost used in the calculation of economic profit are opportunity costs. The Analysis of Maximizing Behavior Marginal benefit is the amount by which an additional unit of an activity increases its total benefit Marginal cost is the amount by which an additional unit of an activity increases its total cost Marginal decision rule: Net benefit is maximized at the point at which marginal benefit equals marginal cost. A constraint is a boundary that limits the range of choices that can be made

The marginal benefit curve for most activities slopes downwards. Total benefit equals the area under the marginal benefit curve up to the quantity of the activity

The marginal cost curve slopes upward. The area under the marginal cost curve gives total cost.

Deadweight loss is the amount of net benefit given up by a failure to operate where marginal benefit equals marginal cost.

Maximizing in the Marketplace When the net benefits of all economic activities are maximized, the allocation of resources is considered efficient. (Allocative Efficient) The concept of an efficient allocation of resources incorporates both the production and consumption of goods or services. Achieving Efficiency The role of property rights Property rights are a set of rules that specify the ways in which an owner can use a resource. A system of property rights forms the basis for all market exchange There are two required characteristics of property rights if the market- place is to be efficient Exclusivity. An exclusive property right is one that allows its owner to prevent others from using the resource Transferability. A transferable property right is one that allows the owner of a resource to sell or lease it to someone else.

A competitive market with well-defined and transferable property rights satisfies the efficiency condition. Producer and Consumer Surplus Consumer surplus is the amount by which the total benefit to consumers exceeds their total expenditure Producer surplus is the difference between the total revenue received by sellers and their total cost.

Efficiency and Equity In a market that satisfies the efficiency condition, an efficient allocation of resources will emerge from any particular distribution of income. Different income distributions will result in different, but still efficient, outcomes There is no test to apply to determine whether the distribution of income is or is not fair or equitable

Market Failure The failure of private decisions in the marketplace to achieve an efficient allocation of resources is called market failure Noncompetitive Markets 1. Market power is the ability to change the market price by an individual firm or group of firms 2. Market power results in distorted price, one that does not equal marginal cost Public Goods 1. A public good is one for which the cost of exclusion is prohibitive and for which the marginal cost of an additional user is zero. 2. A private good is one for which exclusion is possible and for which the marginal cost of another user is positive. 3. Free riders are people or firms that consume a public good without paying for it.

4. Public goods and the government a. Most public goods are provided directly by government b. Private firms under contract with government agencies produce some public goods c. Without government intervention in the market for public goods, the amount of public goods produced is not expected to be that which maximizes net benefit External Costs and Benefits 1. An external cost is a cost imposed on others outside of any market exchange 2. An external benefit is a benefit imposed on others in the absence of any market agreement 3. External costs and efficiency a. External costs are not included in a firm’s supply curve b. The level of output is higher than would be economically efficient

4. External costs and government intervention a. Government may intervene to mitigate external costs b. There are different ways for government to intervene. Government may find a way to force the internalization of external costs through fees and fines Government may use direct regulation by outlawing certain activities Common Property Resources 1. A common property resources is a resource for which no exclusive property rights exist 2. There is frequently no adequate incentive to preserve common property resources 3. When a species faces extinction, it is likely that no one has exclusive property rights to it