Download

1 / 28

280 likes | 449 Views

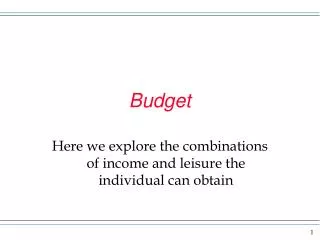

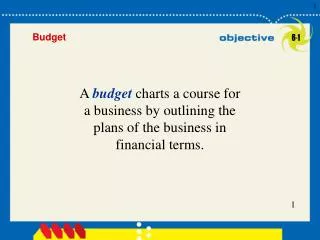

0. 6-1. Budget. A budget charts a course for a business by outlining the plans of the business in financial terms. . 0. Estimated Portion of Your Total Monthly Income That Should Be Budgeted for Various Living Expenses. 6-1. Savings. 8%. Entertainment. Housing. 6%. 30%.

E N D

0 6-1 Budget A budget charts a course for a business by outlining the plans of the business in financial terms.

0 Estimated Portion of Your Total Monthly Income That Should Be Budgeted for Various Living Expenses 6-1 Savings 8% Entertainment Housing 6% 30% Transportation 15% Clothing Utilities 7% 5% Other 4% Food Medical 6 5% 20%

Establishing specific goals 0 6-1 Objectives of Budgeting • Executing plans to achieve the goals • Periodically comparing actual results to the goals

Example Exercise 6-1 0 6-2 At the beginning of the period, the Assembly Department budgeted direct labor of $45,000 and supervisor salaries of $30,000 for 5,000 hours of production. The department actually completed 6,000 hours of production. Determine the budget for the department, assuming that it uses flexible budgeting? 32

Follow My Example 6-1 0 6-2 Variable cost: Direct labor (6,000 hours x $9.00* per hour) $54,000 Fixed cost: Supervisor 30,000 Total department cost $84,000 *45,000/5,000 hours 33 For Practice: PE6-1A, PE6-1B

Budgeted Income Statement Budgeted Balance Sheet Sales budget Cost of goods sold budget: Production budget Direct materials purchases budget Direct labor cost budget Factory overhead cost budget Selling and administrative expense budget Cash budget Capital expenditures budget 0 6-3 Budgets That Are Linked Together in a Master Budget

0 6-3 Income Statement Budgets 36

0 6-4 Sales Budget The sales budget normally indicates for each product— (1) the quantity of estimated sales and (2) the expected unit selling price.

0 6-4 Production Budget The number of units to be manufactured to meet budgeted sales and inventory needs for each product is set forth in the production budget.

Production Budget Expected units of sales + Desired units in ending inventory – Estimated units in beginning inventory Total units to be produced 0 6-4 Sales Budget 42

Example Exercise 6-2 0 6-4 Landon Awards Co. projected sales of 45,000 brass plaques for 2008. The estimated January 1, 2008 inventory is 3,000 units, and the desired December 31, 2008 inventory is 5,000 units. What is the budgeted production (in units) for 2008? 43

Follow My Example 6-2 0 6-4 Expected units to be sold 45,000 Plus: desired ending inventory, December 31, 2008 5,000 Total 50,000 Less estimated beginning inventory, January 1, 2008 3,000 Total units to be produced 47,000 44 For Practice: PE6-2A, PE6-2B

Production Budget Materials needed for production + Desired ending materials inventory – Estimated beginning materials inventory Direct materials to be purchased 0 6-4 Direct Materials Purchases Budget Sales Budget Direct Materials Purchases Budget 45

Example Exercise 6-3 0 6-4 Landon Awards Co. budgeted production of 47,000 brass plaques in 2008. Brass sheet is required to produce a brass plaque. Assume 96 square inches of brass sheet is required for each brass plaque. The estimated January 1, 2008 brass sheet inventory is 240,000 square inches. The desired December 31, 2008 brass sheet inventory is 200,000 square inches. If brass sheets costs $0.12 per square inch, determine the materials budget for 2008. 47

Follow My Example 6-3 0 6-4 Square inches required for production: Brass plaque (47,000 x 96 sq. in.) 4,512,000 Plus: desired ending inventory, December 31, 2008 200,000 Total 4,712,000 Less estimated beginning inventory, January 1, 2008 240,000 Total square inches to purchase 4,472,000 Unit price (per square inch) x $0.12 Total direct materials to be purchased $ 536,640 48 For Practice: PE6-3A, PE6-3B

Production Budget 0 6-4 Direct Labor Cost Budget Sales Budget Direct Materials Purchases Budget Direct Labor Cost Budget 50

Example Exercise 6-4 0 6-4 Landon Awards Co. budgeted production of 47,000 brass plaques in 2008. Assume that 12 minutes are required to engrave each plaque. If engraving labor costs $11.00 per hour, determine the direct labor budget for 2008. 51

Follow My Example 6-4 0 6-4 • Hours required for engraving: • Brass plaque (47,000 x 12 min.) 564,000 min. • Convert minutes to hour / 60 min. Engraving hours9,400 hrs. Hourly rate x $11.00 Total direct labor cost $103,400 52 For Practice: PE6-4A, PE6-4B

Production Budget 0 6-4 Factory Overhead Cost Budget Sales Budget Direct Materials Purchases Budget Direct Labor Cost Budget Factory Overhead Cost Budget 54

0 6-4 Cost of Goods Sold Budget Direct materials purchase budget Direct labor cost budget Factory overhead cost budget 55

Production Budget Cost of Goods Sold Budget 0 6-4 Factory Overhead Cost Budget Sales Budget Direct Materials Purchases Budget Direct Labor Cost Budget Factory Overhead Cost Budget 56

0 6-4 Selling and Administrative Expense Budget 60

Production Budget Cost of Goods Sold Budget 0 6-4 Selling and Administrative Expense Budget Sales Budget Direct Materials Purchases Budget Direct Labor Cost Budget Selling & Administrative Expenses Budget Factory Overhead Cost Budget 61

0 6-4 Budgeted Income Statement Sales budget Cost of goods sold budget Selling and administrative expenses budget 62

0 6-5 Cash Budget The cash budget is one of the most important elements of the budgeted balance sheet. The cash budget presents the expected receipts (inflows) and payments (outflows) of cash for a period of time.

Example Exercise 6-6 0 6-5 Landon Awards Co. collects 25% of its sales on account in the month of the sale and 75% in the month following the sale. If sales on account are budgeted to be $100,000 for March and $126,000 for April, what are the budgeted cash receipts from sales on account for April? 72

Follow My Example 6-6 April Collections from March sales (75% x $100,000) $ 75,000 Collections from April sales (25% x $126,000) 31,500 Total receipts from sales on account $106,500 0 6-5 73 For Practice: PE6-6A, PE6-6B

0 6-5 Capital Expenditure Budget The capital expenditure budget summarizes plans for acquiring fixed assets. 76